The

Little Book of Valuation

The

Little Book of Valuation

Discount Rates

Cash

flows that are riskier should be assessed a lower value than more stable cashflows,

but how do we measure risk and reflect it in value? In conventional discounted

cash flow valuation models, the discount rate becomes the vehicle for conveying

our concerns about risk. We use higher discount rates on riskier cash flows and

lower discount rates on safer cash flows. In this section, we will begin be

contrasting how the risk in equity can vary from the risk in a business, and

then consider the mechanics of estimating the cost of equity and capital.

Business Risk

versus Equity Risk

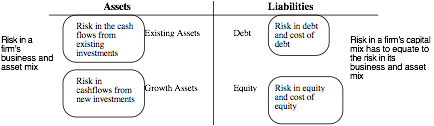

Before

we delve into the details of risk measurement and discount rates, we should

draw a contrast between two different ways of thinking about risk that relate

back to the financial balance sheet that we presented in chapter 1. In the

first, we think about the risk in a firm’s operations or assets, i.e., the risk

in the business. In the second, we look at the risk in the equity investment in

this business. Figure 2.5 captures the differences between the two measures:

Figure 2.5: Risk in Business versus Risk in Equity

As

with any other aspect of the balance sheet, this one has to balance has well,

with the weighted risk in the assets being equal to the weighted risk in the

ingredients to capital – debt and equity. Note that the risk in the

equity investment in a business is partly determined by the risk of the

business the firm is in and partly by its choice on how much debt to use to

fund that business. The equity in a safe business can be rendered risky, if the

firm uses enough debt to fund that business.

In

discount rate terms, the risk in the equity in a business is measured with the

cost of equity, whereas the risk in the business is captured in the cost of

capital. The latter will be a weighted average of the cost of equity and the

cost of debt, with the weights reflecting the proportional use of each source

of funding.

Measuring Equity

Risk and the Cost of Equity

Measuring

the risk in equity investments and converting that risk measure into a cost of

equity is rendered difficult by two factors. The first is that equity has an

implicit cost, which is unobservable, unlike debt, which comes with an explicit

cost in the form of an interest rate. The second is that risk in the eyes of

the beholder and different equity investors in the same business can have very

different perceptions of risk in that business and demand different expected

returns as a consequence.

The Diversified Marginal Investor

If

there were only one equity investor in a company, estimating equity risk and

the cost of equity would be a far simpler exercise. We would measure the risk

of investing in equity in that company to the investor and assess a reasonable

rate of return, given that risk. In a publicly traded company, we run into the

practical problem that the equity investors number in the hundreds, if not the

thousands, and that they not only vary in size, from small to large investors,

but also in risk aversion. So, whose perspective should we take when measuring

risk and cost of equity? In corporate finance and valuation, we develop the

notion of the marginal investor,

i.e., the investor most likely to influence the market price of publicly traded

equity. The marginal investor in a publicly traded stock has to own enough

stock in the company to make a difference and be willing to trade on that

stock. The common theme shared by risk and return models in finance is that the

marginal investor is diversified, and we measure the risk in an investment as

the risk added to a diversified portfolio.

Put another way, it is only that portion of the risk in an investment

that is attributable to the broader market or economy, and hence not

diversifiable, that should be built into expected returns.

Models for Expected Return (Cost of Equity)

It

is on the issue of how best to measure this non-diversifiable risk that the

different risk and return models in finance part ways. Let use consider the

alternatives:

·

In the capital

asset pricing model (CAPM), this risk is captured in the beta that we assign an asset/business,

with that number carrying the burden of measuring exposure to all of the

components of market risk. The expected return on an investment can then be

specified as a function of three variables – the riskfree rate, the beta

of the investment and the equity risk premium (the premium demanded for

investing in the average risk investment):

Expected

Return = Riskfree Rate + BetaInvestment

(Equity Risk Premium)

The riskfree rate and equity risk

premium are the same for all investments in a market but the beta will capture

the market risk exposure of the investment; a beta of one represents an average

risk investment, and betas above (below) one indicate investments that are

riskier (safer) than the average risk investment in the market.

·

In the arbitrage pricing and multi-factor

models, we allow for multiple sources of non-diversifiable (or market) risk and

estimate betas against each one. The expected return on an investment can be

written as a function of the multiple betas (relative to each market risk

factor) and the risk premium for that factor. If there are k factors in the

model with bji

and Risk Premiumj representing the beta

and risk premium of factor j, the expected return on the investment can be

written as:

Expected

Return = ![]()

Note

that the capital asset pricing model can be written as a special case of these

multi-factor models, with a single factor (the market) replacing the multiple

factors.

·

The final class of models can be categorized as

proxy models. In these models, we essentially give up on measuring risk

directly and instead look at historical data for clues on what types of

investments (stocks) have earned high returns in the past, and then use the

common characteristic(s) that they share as a measure of risk. For instance,

researchers have found that market capitalization and price to book ratios are

correlated with returns; stocks with small market capitalization and low price

to book ratios have historically earned higher returns than large market stocks

with higher price to book ratios. Using the historical data, we can then

estimate the expected return for a company, based on its market capitalization

and price to book ratio.

Expected

Return = a + b(Market Capitalization) + c (Price to

Book Ratio)

Since

we are no longer working within the confines of an economic model, it is not

surprising that researchers keep finding new variables (trading volume, price

momentum) that improve the predictive power of these models. The open question,

though, is whether these variables are truly proxies for risk or indicators of

market inefficiency. In effect, we may be explaining away the misvaluatiion of classes of stock by the market by using

proxy models for risk.

Estimation Issues

With

the CAPM and multi-factor models, the inputs that we need for the expected

return are straightforward. We need to come up with a risk free rate and an

equity risk premium (or premiums in the multi-factor models) to use across all

investments. Once we have these market-wide estimates, we then have to measure

the risk (beta or betas) in individual investments. In this section, we will lay out the broad principles that will govern these

estimates but we will return in future chapters to the details of how best to

make these estimates for different types of businesses:

·

The riskfree rate is the expected return on an

investment with guaranteed returns; in effect, you expected return is also your

actual return. Since the return is guaranteed, there are two conditions that an

investment has to meet to be riskfree. The first is that the entity making the

guarantee has to have no default risk; this is why we use government securities

to derive riskfree rates, a necessary though not always a sufficient condition.

As we will see in chapter 6, there is default risk in many government

securities that is priced into the expected return. The second is that the time

horizon matters. A six-month treasury bill is not riskfree, if you are looking

at a five-year time horizon, since we are exposed to reinvestment risk. In

fact, even a 5-year treasury bond may not be riskless, since the coupons

received every six months have to be reinvested. Clearly, getting a riskfree

rate is not as simple as it looks at the outset.

·

The equity risk premium is the premium that

investors demand for investing in risky assets (or equities) as a class,

relative to the riskfree rate. It will be a function not only of how much risk

investors perceive in equities, as a class, but the risk aversion that they

bring to the market. It also follows that the equity risk premium can change

over time, as market risk and risk aversion both change. The conventional

practice for estimating equity risk premiums is to use the historical risk

premium, i.e., the premium investors have earned over long periods (say 75

years) investing in equities instead of riskfree (or close to riskfree) investments.

In chapter 7, we will question the efficacy of this process and offer

alternatives.

·

To estimate the beta in the CAPM and betas in

multi-factor models, we draw on statistical techniques and historical data. The

standard approach for estimating the CAPM beta is to run a regression of

returns on a stock against returns on a broad equity market index, with the

slope capturing how much the stock moves, for any given market move. To

estimate betas in the arbitrage pricing model, we use

historical return data on stocks and factor analysis to extract both the number

of factors in the models, as well as factor betas for individual companies. As

a consequence, the beta estimates that we obtain will always be backward

looking (since they are derived from past data) and noisy (they are statistical

estimates, with standard errors). In addition, these approaches clearly will

not work for investments that do not have a trading history (young companies,

divisions of publicly traded companies). One solution is to replace the

regression beta with a bottom-up beta,

i.e., a beta that is based upon industry averages for the businesses that the

firm is in, adjusted for differences in financial leverage.[1]

Since industry averages are more precise than individual regression betas, and

the weights on the businesses can reflect the current mix of a firm, bottom up

betas generally offer better estimates for the future.

The Cost of Debt

While

equity investors receive residual cash flows and bear the bulk of the operating

risk in most firms, lenders to the firm also face the risk that they will not

receive their promised payments – interest expenses and principal

repayments. It is to cover this default risk that lenders add a “default spread”

to the riskless rate when they lend money to firms; the greater the perceived

risk of default, the greater the default spread and the cost of debt. The other

dimension on which debt and equity can vary is in their treatment for tax

purposes, with cashflows to equity investors (dividends and stock buybacks)

coming from after-tax cash flows, whereas interest payments are tax

deductible. In effect, the tax law

provides a benefit to debt and lowers the cost of borrowing to businesses.

To

estimate the cost of debt for a firm, we need three components. The first is

the riskfree rate, an input to the cost of equity as well. As a general rule,

the riskfree rate used to estimate the cost of equity should be used to compute

the cost of debt as well; if the cost of equity is based upon a long-term

riskfree rate, as it often is, the cost of debt should be based upon the same

rate. The second is the default spread and there are three approaches that are

used, depending upon the firm being analyzed.

·

If the firm has traded bonds outstanding, the

current market interest rate on the bond (yield to maturity) is used as the

cost of debt. This is appropriate only if the bond is liquid and is

representative of the overall debt of the firm; even risky firms can issue safe

bonds, backed up by the most secure assets of the firms.

·

If the firm has a bond rating from an

established ratings agency such as S&P or Moody’s, we can estimate a

default spread based upon the rating. In September 2008, for instance, the

default spread for BBB rated bonds was 2% and would have been used as the

spread for any BBB rated company.

·

If the firm is unrated and has debt outstanding

(bank loans), we can estimate a “synthetic” rating for the firm, based upon its

financial ratios. A simple, albeit effective approach for estimating the

synthetic ratio is to base it entirely on the interest coverage ratio (EBIT/

Interest expense) of a firm; higher interest coverage ratios will yield higher

ratings and lower interest coverage ratios.

The

final input needed to estimate the cost of debt is the tax rate. Since interest

expenses save you taxes at the margin, the tax rate that is relevant for this

calculation is not the effective tax rate but the marginal tax rate. In the

United States, where the federal corporate tax rate is 35% and state and local

taxes add to this, the marginal tax rate for corporations in 2008 was close to

40%, much higher than the average effective tax rate, across companies, of 28%.

The after-tax cost of debt for a firm is therefore:

After-tax

cost of debt = (Riskfree Rate + Default Spread) (1- Marginal tax rate)

The

after-tax cost of debt for most firms will be significantly lower than the cost

of equity for two reasons. First, debt in a firm is generally less risky than

its equity, leading to lower expected returns. Second, there is a tax saving

associated with debt that does not exist with equity.

Debt Ratios and

the Cost of Capital

Once

we have estimated the costs of debt and equity, we still have to assign weights

for the two ingredients. To come up with this value, we could start with the

mix of debt and equity that the firm uses right now. In making this estimate,

the values that we should use are market values, rather than book values. For

publicly traded firms, estimating the market value of equity is usually a

trivial exercise, where we multiply the share price by the number of shares

outstanding. Estimating the market value of debt is usually a more difficult

exercise, since most firms have some debt that is not traded. Though many

practitioners fall back on book value of debt as a proxy of market value,

estimating the market value of debt is still a better practice.

Once we have the current market value weights for debt and equity for use in the cost of capital, we have a follow up judgment to make in terms of whether these weights will change or remain stable. If we assume that they will change, we have to specify both what the right or target mix for the firm will be and how soon the change will occur. In an acquisition, for instance, we can assume that the acquirer can replace the existing mix with the target mix instantaneously. As passive investors in publicly traded firms, we have to be more cautious, since we do not control how a firm funds its operations. In this case, we may adjust the debt ratio from the current mix to the target over time, with concurrent changes in the costs of debt, equity and capital. In fact, the last point about debt ratios and costs of capital changing over time is worth reemphasizing. As companies change over time, we should expect the cost of capital to change as well.