What is Valuation?

Knowing what an asset is worth and what determines that value is a pre-requisite for intelligent decision making -- in choosing investments for a portfolio, in deciding on the appropriate price to pay or receive in a takeover and in making investment, financing and dividend choices when running a business. The premise of valuation is that we can make reasonable estimates of value for most assets, and that the same fundamental principles determine the values of all types of assets, real as well as financial. Some assets are easier to value than others, the details of valuation vary from asset to asset, and the uncertainty associated with value estimates is different for different assets, but the core principles remain the same. This introduction lays out some general insights about the valuation process and outlines the role that valuation plays in portfolio management, acquisition analysis and in corporate finance. It also examines the three basic approaches that can be used to value an asset.

A philosophical basis for valuation

A postulate of sound investing is that an investor does not pay more for an asset than it is worth. This statement may seem logical and obvious, but it is forgotten and rediscovered at some time in every generation and in every market. There are those who are disingenuous enough to argue that value is in the eyes of the beholder, and that any price can be justified if there are other investors willing to pay that price. That is patently absurd. Perceptions may be all that matter when the asset is a painting or a sculpture, but we do not and should not buy most assets for aesthetic or emotional reasons; we buy financial assets for the cashflows we expect to receive from them. Consequently, perceptions of value have to be backed up by reality, which implies that the price we pay for any asset should reflect the cashflows it is expected to generate. Valuation models attempt to relate value to the level of, uncertainty about and expected growth in these cashflows.

There are many aspects of valuation where we can agree to disagree, including estimates of true value and how long it will take for prices to adjust to that true value. But there is one point on which there can be no disagreement. Asset prices cannot be justified by merely using the argument that there will be other investors around who will pay a higher price in the future. That is the equivalent of playing a very expensive game of musical chairs, where every investor has to answer the question, "Where will I be when the music stops?” before playing. The problem with investing with the expectation that there will be a bigger fool around to sell an asset to, when the time comes, is that you might end up being the biggest fool of all.

Inside the Valuation Process

There are two extreme views of the valuation process. At one end are those who believe that valuation, done right, is a hard science, where there is little room for analyst views or human error. At the other are those who feel that valuation is more of an art, where savvy analysts can manipulate the numbers to generate whatever result they want. The truth does lies somewhere in the middle and we will use this section to consider three components of the valuation process that do not get the attention they deserve – the bias that analysts bring to the process, the uncertainty that they have to grapple with and the complexity that modern technology and easy access to information have introduced into valuation.

Value first, Valuation to follow: Bias in Valuation

We almost never start valuing a company with a blank slate. All too often, our views on a company are formed before we start inputting the numbers into the models that we use and not surprisingly, our conclusions tend to reflect our biases. We will begin by considering the sources of bias in valuation and then move on to evaluate how bias manifests itself in most valuations. We will close with a discussion of how best to minimize or at least deal with bias in valuations.

Sources of Bias

The bias in valuation starts with the companies we choose to value. These choices are almost never random, and how we make them can start laying the foundation for bias. It may be that we have read something in the press (good or bad) about the company or heard from an expert that it was under or over valued. Thus, we already begin with a perception about the company that we are about to value. We add to the bias when we collect the information we need to value the firm. The annual report and other financial statements include not only the accounting numbers but also management discussions of performance, often putting the best possible spin on the numbers. With many larger companies, it is easy to access what other analysts following the stock think about these companies. Zacks, I/B/E/S and First Call, to name three services among many, provide summaries of how many analysts are bullish and bearish about the stock, and we can often access their complete valuations. Finally, we have the market’s own estimate of the value of the company- the market price – adding to the mix. Valuations that stray too far from this number make analysts uncomfortable, since they may reflect large valuation errors (rather than market mistakes).

In many valuations, there are institutional factors that add to this already substantial bias. For instance, it is an acknowledged fact that equity research analysts are more likely to issue buy rather than sell recommendations, i.e., that they are more likely to find firms to be undervalued than overvalued.[1] This can be traced partly to the difficulties analysts face in obtaining access and collecting information on firms that they have issued sell recommendations on, and partly to pressure that they face from portfolio managers, some of whom might have large positions in the stock, and from their own firm’s investment banking arms which have other profitable relationships with the firms in question.

The reward and punishment structure associated with finding companies to be under and over valued is also a contributor to bias. An analyst whose compensation is dependent upon whether she finds a firm is under or over valued will be biased in her conclusions. This should explain why acquisition valuations are so often biased upwards. The analysis of the deal, which is usually done by the acquiring firm’s investment banker, who also happens to be responsible for carrying the deal to its successful conclusion, can come to one of two conclusions. One is to find that the deal is seriously over priced and recommend rejection, in which case the analyst receives the eternal gratitude of the stockholders of the acquiring firm but little else. The other is to find that the deal makes sense (no matter what the price) and to reap the ample financial windfall from getting the deal done.

Manifestations of Bias

There are three ways in which our views on a company (and the biases we have) can manifest themselves in value. The first is in the inputs that we use in the valuation. When we value companies, we constantly come to forks in the road where we have to make assumptions to move on. These assumptions can be optimistic or pessimistic. For a company with high operating margins now, we can either assume that competition will drive the margins down to industry averages very quickly (pessimistic) or that the company will be able to maintain its margins for an extended period (optimistic). The path we choose will reflect our prior biases. It should come as no surprise then that the end value that we arrive at is reflective of the optimistic or pessimistic choices we made along the way.

The second is in what we will call post-valuation tinkering, where analysts revisit assumptions after a valuation in an attempt to get a value closer to what they had expected to obtain starting off. Thus, an analyst who values a company at $ 15 per share, when the market price is $ 25, may revise his growth rates upwards and his risk downwards to come up a higher value, if she believed that the company was under valued to begin with.

The third is to leave the value as is but attribute the difference between the value we estimate and the value we think is the right one to a qualitative factor such as synergy or strategic considerations. This is a common device in acquisition valuation where analysts are often called upon to justify the unjustifiable. In fact, the use of premiums and discounts, where we augment or reduce estimated value, provides a window on the bias in the process. The use of premiums – control and synergy are good examples – is commonplace in acquisition valuations, where the bias is towards pushing value upwards (to justify high acquisition prices). The use of discounts – illiquidity and minority discounts, for instance – are more typical in private company valuations for tax and divorce court, where the objective is often to report as low a value as possible for a company.

What to do about bias

Bias cannot be regulated or legislated out of existence. Analysts are human and bring their biases to the table. However, there are ways in which we can mitigate the effects of bias on valuation:

1. Reduce institutional pressures: As we noted earlier, a significant portion of bias can be attributed to institutional factors. Equity research analysts in the 1990s, for instance, in addition to dealing with all of the standard sources of bias had to grapple with the demand from their employers that they bring in investment banking business. Institutions that want honest sell-side equity research should protect their equity research analysts who issue sell recommendations on companies, not only from irate companies but also from their own sales people and portfolio managers.

2. De-link valuations from reward/punishment: Any valuation process where the reward or punishment is conditioned on the outcome of the valuation will result in biased valuations. In other words, if we want acquisition valuations to be unbiased, we have to separate the deal analysis from the deal making to reduce bias.

3. No pre-commitments: Decision makers should avoid taking strong public positions on the value of a firm before the valuation is complete. An acquiring firm that comes up with a price prior to the valuation of a target firm has put analysts in an untenable position, where they are called upon to justify this price. In far too many cases, the decision on whether a firm is under or over valued precedes the actual valuation, leading to seriously biased analyses.

4. Self-Awareness: The best antidote to bias is awareness. An analyst who is aware of the biases he or she brings to the valuation process can either actively try to confront these biases when making input choices or open the process up to more objective points of view about a company’s future.

5. Honest reporting: In Bayesian statistics, analysts are required to reveal their priors (biases) before they present their results from an analysis. Thus, an environmentalist will have to reveal that he or she strongly believes that there is a hole in the ozone layer before presenting empirical evidence to that effect. The person reviewing the study can then factor that bias in while looking at the conclusions. Valuations would be much more useful if analysts revealed their biases up front.

While we cannot eliminate bias in valuations, we can try to minimize its impact by designing valuation processes that are more protected from overt outside influences and by report our biases with our estimated values.

It is only an estimate: Imprecision and Uncertainty in Valuation

Starting early in life, we are taught that if we do things right, we will get the right answers. In other words, the precision of the answer is used as a measure of the quality of the process that yielded the answer. While this may be appropriate in mathematics or physics, it is a poor measure of quality in valuation. Barring a very small subset of assets, there will always be uncertainty associated with valuations, and even the best valuations come with a substantial margin for error. In this section, we examine the sources of uncertainty and the consequences for valuation.

Sources of Uncertainty

Uncertainty is part and parcel of the valuation process, both at the point in time that we value a business and in how that value evolves over time as we get new information that impacts the valuation. That information can be specific to the firm being valued, more generally about the sector in which the firm operates or even be general market information (about interest rates and the economy).

When valuing an asset at any point in time, we make forecasts for the future. Since none of us possess crystal balls, we have to make our best estimates, given the information that we have at the time of the valuation. Our estimates of value can be wrong for a number of reasons, and we can categorize these reasons into three groups.

a. Estimation Uncertainty: Even if our information sources are impeccable, we have to convert raw information into inputs and use these inputs in models. Any mistakes or mis-assessments that we make at either stage of this process will cause estimation error.

b. Firm-specific Uncertainty: The path that we envision for a firm can prove to be hopelessly wrong. The firm may do much better or much worse than we expected it to perform, and the resulting earnings and cash flows will be very different from our estimates.

c. Macroeconomic Uncertainty: Even if a firm evolves exactly the way we expected it to, the macro economic environment can change in unpredictable ways. Interest rates can go up or down and the economy can do much better or worse than expected. These macro economic changes will affect value.

The contribution of each type of uncertainty to the overall uncertainty associated with a valuation can vary across companies. When valuing a mature cyclical or commodity company, it may be macroeconomic uncertainty that is the biggest factor causing actual numbers to deviate from expectations. Valuing a young technology company can expose analysts to far more estimation and firm-specific uncertainty. Note that the only source of uncertainty that can be clearly laid at the feet of the analyst is estimation uncertainty.

Even if we feel comfortable with our estimates of an asset’s values at any point in time, that value itself will change over time, as a consequence of new information that comes out both about the firm and about the overall market.. Given the constant flow of information into financial markets, a valuation done on a firm ages quickly, and has to be updated to reflect current information. Thus, technology companies that were valued highly in late 1999, on the assumption that the high growth from the nineties would continue into the future, would have been valued much less in early 2001, as the prospects of future growth dimmed. With the benefit of hindsight, the valuations of these companies (and the analyst recommendations) made in 1999 can be criticized, but they may well have been reasonable, given the information available at that time.

Responses of Uncertainty

Analysts who value companies confront uncertainty at every turn in a valuation and they respond to it in both healthy and unhealthy ways. Among the healthy responses are the following:

1. Better Valuation Models: Building better valuation models that use more of the information that is available at the time of the valuation is one way of attacking the uncertainty problem. It should be noted, though, that even the best-constructed models may reduce estimation uncertainty but they cannot reduce or eliminate the very real uncertainties associated with the future

2. Valuation Ranges: A few analysts recognize that the value that they obtain for a business is an estimate and try to quantify a range on the estimate. Some use simulations and others derive expected, best-case and worst-case estimates of value. The output that they provide therefore yields both their estimates of value and their uncertainty about that value.

3. Probabilistic Statements: Some analysts couch their valuations in probabilistic terms to reflect the uncertainty that they feel. Thus, an analyst who estimates a value of $ 30 for a stock which is trading at $ 25 will state that there is a 60 or 70% probability that the stock is under valued rather than make the categorical statement that it is under valued. Here again, the probabilities that accompany the statements provide insight into the uncertainty that the analyst perceives in the valuation.

In general, healthy responses to uncertainty are open about its existence and provide information on its magnitude to those using the valuation. These users can then decide how much caution they should exhibit while acting on the valuation.

Unfortunately, not all analysts deal with uncertainty in ways that lead to better decisions. The unhealthy responses to uncertainty include:

1. Passing the buck: Some analysts try to pass on responsibility for the estimates by using other people’s numbers in the valuation. For instance, analysts will often use the growth rate estimated by other analysts valuing a company as their estimate of growth. If the valuation turns out to be right, they can claim credit for it, and if it turns out wrong, they can blame other analysts for leading them down the garden path.

2. Giving up on fundamentals: A significant number of analysts give up, especially on full-fledged valuation models, unable to confront uncertainty and deal with it. All too often, they fall back on more simplistic ways of valuing companies (multiples and comparables, for example) that do not require explicit assumptions about the future. A few decide that valuation itself is pointless and resort to reading charts and gauging market perception.

In closing, it is natural to feel uncomfortable when valuing equity in a company. We are after all trying to make our best judgments about an uncertain future. The discomfort will increase as we move from valuing stable companies to growth companies, from valuing mature companies to young companies and from valuing developed market companies to emerging market companies.

What to do about uncertainty

The advantage of breaking uncertainty down into estimation uncertainty, firm-specific and macroeconomic uncertainty is that it gives us a window on what we can manage, what we can control and what we should just let pass through into the valuation. Building better models and accessing superior information will reduce estimation uncertainty but will do little to reduce exposure to firm-specific or macro-economic risk. Even the best-constructed model will be susceptible to these uncertainties.

In general, analysts should try to focus on making their best estimates of firm-specific information – how long will the firm be able to maintain high growth? How fast will earnings grow during that period? What type of excess returns will the firm earn?– and steer away from bringing in their views on macro economic variables. To see why, assume that you believe that interest rates today are too low and that they will go up by about 1.5% over the next year. If you build in the expected rise in interest rates into your discounted cash flow valuations, they will all yield low values for the companies that you are analyzing. A person using these valuations will be faced with a conundrum because she will have no way of knowing how much of this over valuation is attributable to your macroeconomic views and how much to your views of the company.

In summary, analysts should concentrate on building the best models they can with as much information as they can legally access, trying to make their best estimates of firm-specific components and being as neutral as they can on macro economic variables. As new information comes in, they should update their valuations to reflect the new information. There is no place for false pride in this process. Valuations can change dramatically over time and they should if the information warrants such a change.

The Payoff to Valuation

Even at the end of the most careful and detailed valuation, there will be uncertainty about the final numbers, colored as they are by assumptions that we make about the future of the company and the economy in which it operates. It is unrealistic to expect or demand absolute certainty in valuation, since the inputs are estimated with error. This also means that analysts have to give themselves reasonable margins for error in making recommendations on the basis of valuations.

The corollary to this statement is that a valuation cannot be judged by its precision. Some companies can be valued more precisely than others simply because there is less uncertainty about the future. We can value a mature company with relatively few assumptions and be reasonably comfortable with the estimated value. Valuing a technology firm will require far more assumptions, as will valuing an emerging market company. A scientist looking at the valuations of these companies (and the associated estimation errors) may very well consider the mature company valuation the better one, since it is the most precise, and the technology firms and emerging market company valuations to be inferior because there is most uncertainty associated with the estimated values. The irony is that the payoff to valuation will actually be highest when you are most uncertain about the numbers. After all, it is not how precise a valuation is that determines its usefulness but how precise the value is relative to the estimates of other investors trying to value the same company. Any one can value a zero-coupon default-free bond with absolute precision. Valuing a young technology firm or an emerging market firm requires a blend of forecasting skills, tolerance for ambiguity and willingness to make mistakes that many analysts do not have. Since most analysts tend to give up in the face of such uncertainty, the analyst who perseveres and makes her best estimates (error-prone though they might be) will have a differential edge.

We do not want to leave the impression that we are completely helpless in the face of uncertainty. Simulations, decision trees and sensitivity analyses are tools that help us deal with uncertainty but not eliminate it.

Are bigger models better? Valuation Complexity

Valuation models have become more and more complex over the last two decades, as a consequence of two developments. On the one side, computers and calculators have become far more powerful and accessible in the last few decades. With technology as our ally, tasks that would have taken us days in the pre-computer days can be accomplished in minutes. On the other side, information is both more plentiful, and easier to access and use. We can download detailed historical data on thousands of companies and use them as we see fit. The complexity, though, has come at a cost. In this section, we will consider the trade off on complexity and how analysts can decide how much to build into models.

More detail or less detail

A fundamental question that we all face when doing valuations is how much detail we should break a valuation down into. There are some who believe that more detail is always better than less detail and that the resulting valuations are more precise. We disagree. The trade off on adding detail is a simple one. On the one hand, more detail gives analysts a chance to use specific information to make better forecasts on each individual item. On the other hand, more detail creates the need for more inputs, with the potential for error on each one, and generates more complicated models. Thus, breaking working capital down into its individual components – accounts receivable, inventory, accounts payable, supplier credit etc. – gives an analyst the discretion to make different assumptions about each item, but this discretion has value only if the analyst has the capacity to differentiate between the items.

The Cost of Complexity

A parallel and related question to how much detail there should be in a valuation is the one of how complex a valuation model should be. There are clear costs that we pay as models become more complex and require more information.

1. Information Overload: More information does not always lead to better valuations. In fact, analysts can become overwhelmed when faced with vast amounts of conflicting information and this can lead to poor input choices. The problem is exacerbated by the fact that analysts often operate under time pressure when valuing companies. Models that require dozens of inputs to value a single company often get short shrift from users. A model’s output is only as good as the inputs that go into it; it is garbage in, garbage out.

2. Black Box Syndrome: The models become so complicated that the analysts using them no longer understand their inner workings. They feed inputs into the model’s black box and the box spits out a value. In effect, the refrain from analysts becomes “The model valued the company at $ 30 a share” rather than “We valued the company at $ 30 a share”. Of particular concern should be models where portions of the models are proprietary and cannot be accessed (or modified) by analysts. This is often the case with commercial valuation models, where vendors have to keep a part of the model out of bounds to make their services indispensable.

3. Big versus Small Assumptions: Complex models often generate voluminous and detailed output and it becomes very difficult to separate the big assumptions from the small assumptions. In other words, the assumption that pre-tax operating margins will stay at 20% (a big assumption that doubles the value of the company) has to compete with the assumption that accounts receivable will decline from 5% of revenues to 4% of revenues over the next 10 years (a small assumption that has almost no impact on value).

The Principle of Parsimony

In the physical sciences, the principle of parsimony dictates that we try the simplest possible explanation for a phenomenon before we move on to more complicated ones. We would be well served adopting a similar principle in valuation. When valuing an asset, we want to use the simplest model we can get away with. In other words, if we can value an asset with three inputs, we should not be using five. If we can value a company with 3 years of cashflow forecasts, forecasting ten years of cash flows is asking for trouble.

The problem with all-in-one models that are designed to value all companies is that they have to be set up to value the most complicated companies that we will face and not the least complicated. Thus, we are forced to enter inputs and forecast values for simpler companies that we really do not need to estimate. In the process, we can mangle the values of assets that should be easy to value. Consider, for instance, the cash and marketable securities held by firms as part of their assets. The simplest way to value this cash is to take it at face value. Analysts who try to build discounted cash flow or relative valuation models to value cash often mis-value it, either by using the wrong discount rate for the cash income or by using the wrong multiple for cash earnings.[2]

Approaches to Valuation

Analysts use a wide spectrum of models, ranging from the simple to the sophisticated. These models often make very different assumptions about the fundamentals that determine value, but they do share some common characteristics and can be classified in broader terms. There are several advantages to such a classification -- it makes it is easier to understand where individual models fit in to the big picture, why they provide different results and when they have fundamental errors in logic.

In general terms, there are three approaches to valuation. The first, discounted cashflow valuation, relates the value of an asset to the present value of expected future cashflows on that asset. The second, relative valuation, estimates the value of an asset by looking at the pricing of 'comparable' assets relative to a common variable like earnings, cashflows, book value or sales. The third, contingent claim valuation, uses option pricing models to measure the value of assets that share option characteristics. While they can yield different estimates of value, one of the objectives of discussing valuation models is to explain the reasons for such differences, and to help in picking the right model to use for a specific task.

Discounted Cashflow Valuation

In discounted cashflows valuation, the value of an asset is the present value of the expected cashflows on the asset, discounted back at a rate that reflects the riskiness of these cashflows. This approach gets the most play in classrooms and comes with the best theoretical credentials. In this section, we will look at the foundations of the approach and some of the preliminary details on how we estimate its inputs.

Basis for Approach

We buy most assets because we expect them to generate cash flows for us in the future. In discounted cash flow valuation, we begin with a simple proposition. The value of an asset is not what someone perceives it to be worth but it is a function of the expected cash flows on that asset. Put simply, assets with high and predictable cash flows should have higher values than assets with low and volatile cash flows. In discounted cash flow valuation, we estimate the value of an asset as the present value of the expected cash flows on it.

![]()

where,

n = Life of the asset

E(CFt) = Expected cashflow in period t

r = Discount rate reflecting the riskiness of the estimated cashflows

The cashflows will vary from asset to asset -- dividends for stocks, coupons (interest) and the face value for bonds and after-tax cashflows for a business. The discount rate will be a function of the riskiness of the estimated cashflows, with higher rates for riskier assets and lower rates for safer ones.

Using discounted cash flow models is in some sense an act of faith. We believe that every asset has an intrinsic value and we try to estimate that intrinsic value by looking at an asset’s fundamentals. What is intrinsic value? Consider it the value that would be attached to an asset by an all-knowing analyst with access to all information available right now and a perfect valuation model. No such analyst exists, of course, but we all aspire to be as close as we can to this perfect analyst. The problem lies in the fact that none of us ever gets to see what the true intrinsic value of an asset is and we therefore have no way of knowing whether our discounted cash flow valuations are close to the mark or not.

Classifying Discounted Cash Flow Models

There are three distinct ways in which we can categorize discounted cash flow models. In the first, we differentiate between valuing a business as a going concern as opposed to a collection of assets. In the second, we draw a distinction between valuing the equity in a business and valuing the business itself. In the third, we lay out three different and equivalent ways of doing discounted cash flow valuation – the expected cash flow approach, a value based upon excess returns and adjusted present value.

a. Going Concern versus Asset Valuation

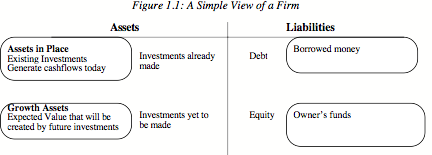

The value of an asset in the discounted cash flow framework is the present value of the expected cash flows on that asset. Extending this proposition to valuing a business, it can be argued that the value of a business is the sum of the values of the individual assets owned by the business. While this may be technically right, there is a key difference between valuing a collection of assets and a business. A business or a company is an on-going entity with assets that it already owns and assets it expects to invest in the future. This can be best seen when we look at the financial balance sheet (as opposed to an accounting balance sheet) for an ongoing company in figure 1.1:

Note that investments that have already been made are categorized as assets in place, but investments that we expect the business to make in the future are growth assets.

A financial balance sheet provides a good framework to draw out the differences between valuing a business as a going concern and valuing it as a collection of assets. In a going concern valuation, we have to make our best judgments not only on existing investments but also on expected future investments and their profitability. While this may seem to be foolhardy, a large proportion of the market value of growth companies comes from their growth assets. In an asset-based valuation, we focus primarily on the assets in place and estimate the value of each asset separately. Adding the asset values together yields the value of the business. For companies with lucrative growth opportunities, asset-based valuations will yield lower values than going concern valuations.

One special case of asset-based valuation is liquidation valuation, where we value assets based upon the presumption that they have to be sold now. In theory, this should be equal to the value obtained from discounted cash flow valuations of individual assets but the urgency associated with liquidating assets quickly may result in a discount on the value. How large the discount will be will depend upon the number of potential buyers for the assets, the asset characteristics and the state of the economy.

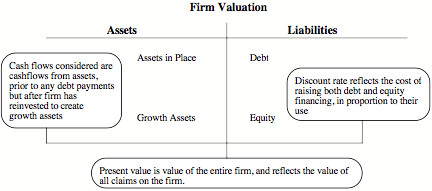

b. Equity Valuation versus Firm Valuation

There are two ways in which we can approach discounted cash flow valuation. The first is to value the entire business, with both assets-in-place and growth assets; this is often termed firm or enterprise valuation.

The cash flows before debt payments and after reinvestment needs are called free

cash flows to the firm, and the discount rate that reflects the composite

cost of financing from all sources of capital is called the cost of capital.

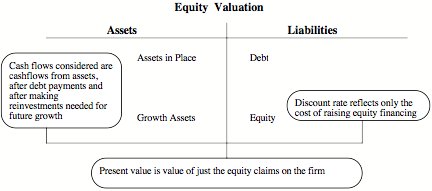

The second way is to just value the equity stake in the business, and this is called equity valuation.

The cash flows after debt payments and reinvestment needs are called free cash flows

to equity, and the discount rate that reflects just the cost of equity

financing is the cost of equity.

Note also that we can always get from the former (firm value) to the latter (equity value) by netting out the value of all non-equity claims from firm value. Done right, the value of equity should be the same whether it is valued directly (by discounting cash flows to equity a the cost of equity) or indirectly (by valuing the firm and subtracting out the value of all non-equity claims).

c. Variations on DCF Models

The model that we have presented in this section, where expected cash flows are discounted back at a risk-adjusted discount rate, is the most commonly used discounted cash flow approach but there are two widely used variants. In the first, we separate the cash flows into excess return cash flows and normal return cash flows. Earning the risk-adjusted required return (cost of capital or equity) is considered a normal return cash flow but any cash flows above or below this number are categorized as excess returns; excess returns can therefore be either positive or negative. With the excess return valuation framework, the value of a business can be written as the sum of two components:

Value of business = Capital Invested in firm today + Present value of excess return cash flows from both existing and future projects

If we make the assumption that the accounting measure of capital invested (book value of capital) is a good measure of capital invested in assets today, this approach implies that firms that earn positive excess return cash flows will trade at market values higher than their book values and that the reverse will be true for firms that earn negative excess return cash flows.

In the second variation, called the adjusted present value (APV) approach, we separate the effects on value of debt financing from the value of the assets of a business. In general, using debt to fund a firm’s operations creates tax benefits (because interest expenses are tax deductible) on the plus side and increases bankruptcy risk (and expected bankruptcy costs) on the minus side. In the APV approach, the value of a firm can be written as follows:

Value of business = Value of business with 100% equity financing + Present value of Expected Tax Benefits of Debt – Expected Bankruptcy Costs

In contrast to the conventional approach, where the effects of debt financing are captured in the discount rate, the APV approach attempts to estimate the expected dollar value of debt benefits and costs separately from the value of the operating assets.

While proponents of each approach like to claim that their approach is the best and most precise, we will argue that the three approaches yield the same estimates of value, if we make consistent assumptions.

Inputs to Discounted Cash Flow Models

There are three inputs that are required to value any asset in this model - the expected cash flow, the timing of the cash flow and the discount rate that is appropriate given the riskiness of these cash flows.

a. Discount Rates

In valuation, we begin with the fundamental notion that the discount rate used on a cash flow should reflect its riskiness, with higher risk cash flows having higher discount rates. There are two ways of viewing risk. The first is purely in terms of the likelihood that an entity will default on a commitment to make a payment, such as interest or principal due, and this is called default risk. When looking at debt, the cost of debt is the rate that reflects this default risk.

The second way of viewing risk is in terms of the variation of actual returns around expected returns. The actual returns on a risky investment can be very different from expected returns; the greater the variation, the greater the risk. When looking at equity, we tend to use measures of risk based upon return variance. While the discussion of risk and return models elsewhere in this site will look at the different models that attempt to do this in far more detail, there are some basic points on which these models agree. The first is that risk in an investment has to perceived through the eyes of the marginal investor in that investment, and this marginal investor is assumed to be well diversified across multiple investments. Therefore, the risk in an investment that should determine discount rates is the non-diversifiable or market risk of that investment. The second is that the expected return on any investment can be obtained starting with the expected return on a riskless investment, and adding to it a premium to reflect the amount of market risk in that investment. This expected return yields the cost of equity.

The cost of capital can be obtained by taking an average of the cost of equity, estimated as above, and the after-tax cost of borrowing, based upon default risk, and weighting by the proportions used by each. We will argue that the weights used, when valuing an on-going business, should be based upon the market values of debt and equity. While there are some analysts who use book value weights, doing so violates a basic principle of valuation, which is that at a fair value[3] , one should be indifferent between buying and selling an asset.

b. Expected Cash Flows

In the strictest sense, the only cash flow an equity investor gets out of a publicly traded firm is the dividend; models that use the dividends as cash flows are called dividend discount models. A broader definition of cash flows to equity would be the cash flows left over after the cash flow claims of non-equity investors in the firm have been met (interest and principal payments to debt holders and preferred dividends) and after enough of these cash flows has been reinvested into the firm to sustain the projected growth in cash flows. This is the free cash flow to equity (FCFE), and models that use these cash flows are called FCFE discount models.

The cashflow to the firm is the cumulated cash flow to all claimholders in the firm. One way to obtain this cashflow is to add the free cash flows to equity to the cash flows to lenders (debt) and preferred stockholders. A far simpler way of obtaining the same number is to estimate the cash flows prior to debt and preferred dividend payments, by subtracting from the after-tax operating income the net investment needs to sustain growth. This cash flow is called the free cash flow to the firm (FCFF) and the models that use these cash flows are called FCFF models.

c. Expected Growth

It is while estimating the expected growth in cash flows in the future that analysts confront uncertainty most directly. There are three generic ways of estimating growth. One is to look at a company’s past and use the historical growth rate posted by that company. The peril is that past growth may provide little indication of future growth. The second is to obtain estimates of growth from more informed sources. For some analysts, this translates into using the estimates provided by a company’s management whereas for others it takes the form of using consensus estimates of growth made by others who follow the firm. The bias associated with both these sources should raise questions about the resulting valuations.

We will promote a third way, where the expected growth rate is tied to two variables that are determined by the firm being valued - how much of the earnings are reinvested back into the firm and how well those earnings are reinvested. In the equity valuation model, this expected growth rate is a product of the retention ratio, i.e. the proportion of net income not paid out to stockholders, and the return on equity on the projects taken with that money. In the firm valuation model, the expected growth rate is a product of the reinvestment rate, which is the proportion of after-tax operating income that goes into net new investments and the return on capital earned on these investments. The advantages of using these fundamental growth rates are two fold. The first is that the resulting valuations will be internally consistent and companies that are assumed to have high growth are required to pay for the growth with more reinvestment. The second is that it lays the foundation for considering how firms can make themselves more valuable to their investors.

DCF Valuation: Pluses and Minuses

To true believers, discounted cash flow valuation is the only way to approach valuation, but the benefits may be more nuanced that they are willing to admit. On the plus side, discounted cash flow valuation, done right, requires analysts to understand the businesses that they are valuing and ask searching questions about the sustainability of cash flows and risk. Discounted cash flow valuation is tailor made for those who buy into the Warren Buffett adage that what we are buying are not stocks but the underlying businesses. In addition, discounted cash flow valuations is inherently contrarian in the sense that it forces analysts to look for the fundamentals that drive value rather than what market perceptions are. Consequently, if stock prices rise (fall) disproportionately relative to the underlying earnings and cash flows, discounted cash flows models are likely to find stocks to be over valued (under valued).

There are, however, limitations with discounted cash flow valuation. In the hands of sloppy analysts, discounted cash flow valuations can be manipulated to generate estimates of value that have no relationship to intrinsic value. We also need substantially more information to value a company with discounted cash flow models, since we have to estimate cashflows, growth rates and discount rates. Finally, discounted cash flow models may very well find every stock in a sector or even a market to be over valued, if market perceptions have run ahead of fundamentals. For portfolio managers and equity research analysts, who are required to find equities to buy even in the most over valued markets, this creates a conundrum. They can go with their discounted cash flow valuations and conclude that everything is overvalued, which may put them out of business, or they can find an alternate approach that is more sensitive to market moods. It should come as no surprise that many choose the latter.

Relative Valuation

While the focus in classrooms and academic discussions remains on discounted cash flow valuation, the reality is that most assets are valued on a relative basis. In relative valuation, we value an asset by looking at how the market prices similar assets. Thus, when determining what to pay for a house, we look at what similar houses in the neighborhood sold for rather than doing an intrinsic valuation. Extending this analogy to stocks, investors often decide whether a stock is cheap or expensive by comparing its pricing to that of similar stocks (usually in its peer group). In this section, we will consider the basis for relative valuation, ways in which it can be used and its advantages and disadvantages.

Basis for approach

In relative valuation, the value of an asset is derived from the pricing of 'comparable' assets, standardized using a common variable. Included in this description are two key components of relative valuation. The first is the notion of comparable or similar assets. From a valuation standpoint, this would imply assets with similar cash flows, risk and growth potential. In practice, it is usually taken to mean other companies that are in the same business as the company being valued. The other is a standardized price. After all, the price per share of a company is in some sense arbitrary since it is a function of the number of shares outstanding; a two for one stock split would halve the price. Dividing the price or market value by some measure that is related to that value will yield a standardized price. When valuing stocks, this essentially translates into using multiples where we divide the market value by earnings, book value or revenues to arrive at an estimate of standardized value. We can then compare these numbers across companies.

The simplest and most direct applications of relative valuations are with real assets where it is easy to find similar assets or even identical ones. The asking price for a Mickey Mantle rookie baseball card or a 1965 Ford Mustang is relatively easy to estimate given that there are other Mickey Mantle cards and 1965 Ford Mustangs out there and that the prices at which they have been bought and sold can be obtained. With equity valuation, relative valuation becomes more complicated by two realities. The first is the absence of similar assets, requiring us to stretch the definition of comparable to include companies that are different from the one that we are valuing. After all, what company in the world is remotely similar to Microsoft or GE? The other is that different ways of standardizing prices (different multiples) can yield different values for the same company.

Harking back to our earlier discussion of discounted cash flow valuation, we argued that discounted cash flow valuation was a search (albeit unfulfilled) for intrinsic value. In relative valuation, we have given up on estimating intrinsic value and essentially put our trust in markets getting it right, at least on average.

Variations on Relative Valuation

In relative valuation, the value of an asset is based upon how similar assets are priced. In practice, there are three variations on relative valuation, with the differences primarily in how we define comparable firms and control for differences across firms:

a. Direct comparison: In this approach, analysts try to find one or two companies that look almost exactly like the company they are trying to value and estimate the value based upon how these “similar” companies are priced. The key part in this analysis is identifying these similar companies and getting their market values.

b. Peer Group Average: In the second, analysts compare how their company is priced (using a multiple) with how the peer group is priced (using the average for that multiple). Thus, a stock is considered cheap if it trade at 12 times earnings and the average price earnings ratio for the sector is 15. Implicit in this approach is the assumption that while companies may vary widely across a sector, the average for the sector is representative for a typical company.

c. Peer group average adjusted for differences: Recognizing that there can be wide differences between the company being valued and other companies in the comparable firm group, analysts sometimes try to control for differences between companies. In many cases, the control is subjective: a company with higher expected growth than the industry will trade at a higher multiple of earnings than the industry average but how much higher is left unspecified. In a few cases, analysts explicitly try to control for differences between companies by either adjusting the multiple being used or by using statistical techniques. As an example of the former, consider PEG ratios. These ratios are computed by dividing PE ratios by expected growth rates, thus controlling (at least in theory) for differences in growth and allowing analysts to compare companies with different growth rates. For statistical controls, we can use a multiple regression where we can regress the multiple that we are using against the fundamentals that we believe cause that multiple to vary across companies. The resulting regression can be used to estimate the value of an individual company. In fact, we will argue that statistical techniques are powerful enough to allow us to expand the comparable firm sample to include the entire market.

Applicability of multiples and limitations

The allure of multiples is that they are simple and easy to relate to. They can be used to obtain estimates of value quickly for firms and assets, and are particularly useful when there are a large number of comparable firms being traded on financial markets, and the market is, on average, pricing these firms correctly. In fact, relative valuation is tailor made for analysts and portfolio managers who not only have to find under valued equities in any market, no matter how overvalued, but also get judged on a relative basis. An analyst who picks stocks based upon their PE ratios, relative to the sectors they operate in, will always find under valued stocks in any market; if entire sectors are over valued and his stocks decline, he will still look good on a relative basis since his stocks will decline less than comparable stocks (assuming the relative valuation is right).

By the same token, they are also easy to misuse and manipulate, especially when comparable firms are used. Given that no two firms are exactly similar in terms of risk and growth, the definition of 'comparable' firms is a subjective one. Consequently, a biased analyst can choose a group of comparable firms to confirm his or her biases about a firm's value. While this potential for bias exists with discounted cashflow valuation as well, the analyst in DCF valuation is forced to be much more explicit about the assumptions which determine the final value. With multiples, these assumptions are often left unstated.

The other problem with using multiples based upon comparable firms is that it builds in errors (over valuation or under valuation) that the market might be making in valuing these firms. If, for instance, we find a company to be under valued because it trades at 15 times earnings and comparable companies trade at 25 times earnings, we may still lose on the investment if the entire sector is over valued. In relative valuation, all that we can claim is that a stock looks cheap or expensive relative to the group we compared it to, rather than make an absolute judgment about value. Ultimately, relative valuation judgments depend upon how well we have picked the comparable companies and how how good a job the market has done in pricing them.

Contingent Claim Valuation

There is little in either discounted cashflow or relative valuation that can be considered new and revolutionary. In recent years, though, analysts have increasingly used option-pricing models, developed to value listed options, to value assets, businesses and equity stakes in businesses. These applications are often categorized loosely as real options, but they have to be used with caution.

Basis for Approach

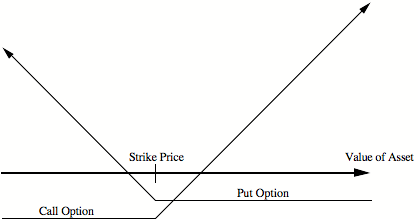

A contingent claim or option is an asset which pays off only under certain contingencies - if the value of the underlying asset exceeds a pre-specified value for a call option, or is less than a pre-specified value for a put option. Much work has been done in the last few decades in developing models that value options, and these option-pricing models can be used to value any assets that have option-like features.

Figure 1.2 illustrates the payoffs on call and put options as a function of the value of the underlying asset:

Figure 1.2: Payoffs on Options as a Function of the Underlying Asset's Value

An option can be valued as a function of the following variables - the current value and the variance in value of the underlying asset, the strike price and the time to expiration of the option and the riskless interest rate. This was first established by Black and Scholes (1972) and has been extended and refined subsequently in numerous variants.[4] While the Black-Scholes option-pricing model ignored dividends and assumed that options would not be exercised early, it can be modified to allow for both. A discrete-time variant, the Binomial option-pricing model, has also been developed to price options.

An asset can be valued as a call option if the payoffs on it are a function of the value of an underlying asset; if that value exceeds a pre-specified level, the asset is worth the difference; if not, it is worth nothing. It can be valued as a put option if it gains value as the value of the underlying asset drops below a pre- specified level, and if it is worth nothing when the underlying asset's value exceeds that specified level. There are many assets that generally are not viewed as options but still share several option characteristics. A patent can be analyzed as a call option on a product, with the investment outlay needed to get the project going considered the strike price and the patent life becoming the life of the option. An undeveloped oil reserve or gold mine provides its owner with a call option to develop the reserve or mine, if oil or gold prices increase.

The essence of the real options argument is that discounted cash flow models understate the value of assets with option characteristics. The understatement occurs because DCF models value assets based upon a set of expected cash flows and do not fully consider the possibility that firms can learn from real time developments and respond to that learning. For example, an oil company can observe what the oil price is each year and adjust its development of new reserves and production in existing reserves accordingly rather than be locked into a fixed production schedule. As a result, there should be an option premium added on to the discounted cash flow value of the oil reserves. It is this premium on value that makes real options so alluring and so potentially dangerous.

Applicability and Limitations

Using option-pricing models in valuation does have its advantages. First, there are some assets that cannot be valued with conventional valuation models because their value derives almost entirely from their option characteristics. For example, a biotechnology firm with a single promising patent for a blockbuster cancer drug wending its way through the FDA approval process cannot be easily valued using discounted cash flow or relative valuation models. It can, however, be valued as an option. The same can be said about equity in a money losing company with substantial debt; most investors buying this stock are buying it for the same reasons they buy deep out-of-the-money options. Second, option-pricing models do yield more realistic estimates of value for assets where there is a significant benefit obtained from learning and flexibility. Discounted cash flow models will understate the values of natural resource companies, where the observed price of the natural resource is a key factor in decision making. Third, option-pricing models do highlight a very important aspect of risk. While risk is considered almost always in negative terms in discounted cash flow and relative valuation (with higher risk reducing value), the value of options increases as volatility increases. For some assets, at least, risk can be an ally and can be exploited to generate additional value.

This

is not to suggest that using real options models is an unalloyed good. Using

real options arguments to justify paying premiums on discounted cash flow

valuations, when the options argument does not hold, can result in overpayment.

While we do not disagree with the notion that firms can learn by observing what

happens over time, this learning has value only if it has some degree of exclusivity.

We will argue that it is usually inappropriate to attach an option premium to

value if the learning is not exclusive and competitors can adapt their behavior

as well. There are also

limitations in using option pricing models to value long-term options on

non-traded assets. The assumptions made about constant variance and dividend

yields, which are not seriously contested for short term options, are much more

difficult to defend when options have long lifetimes. When the underlying asset

is not traded, the inputs for the value of the underlying asset and the

variance in that value cannot be extracted from financial markets and have to

be estimated. Thus the final values obtained from these applications of option

pricing models have much more estimation error associated with them than the

values obtained in their more standard applications (to value short term traded

options).

The Role of Valuation

Valuation is useful in a wide range of tasks. The

role it plays, however, is different in different arenas. The following section

lays out the relevance of valuation in portfolio management, in acquisition

analysis and in corporate finance.

1. Portfolio Management

The role that valuation plays in portfolio management is determined in large part by the investment philosophy of the investor. Valuation plays a minimal role in portfolio management for a passive investor, whereas it plays a larger role for an active investor. Even among active investors, the nature and the role of valuation is different for different types of active investment. Market timers use valuation much less than investors who pick stocks, and the focus is on market valuation rather than on firm-specific valuation. Among security selectors, valuation plays a central role in portfolio management for fundamental analysts, and a peripheral role for technical analysts.

The following sub-section describes, in broad terms, different investment philosophies and the roles played by valuation in each one.

1. Fundamental Analysts: The underlying theme in fundamental analysis is that the true value of the firm can be related to its financial characteristics -- its growth prospects, risk profile and cashflows. Any deviation from this true value is a sign that a stock is under or overvalued. It is a long-term investment strategy, and the assumptions underlying it are that:

(a) The relationship between value and the underlying financial factors can be measured.

(b) The relationship is stable over time.

(c) Deviations from the relationship are corrected in a reasonable time period.

Fundamental analysts include both value and growth investors. The key difference between the two is in where the valuation focus lies. Reverting back to our break down of assets in figure 1.1, value investors are primarily interested in assets in place and acquiring them at less than their true value. Growth investors, on the other hand, are far more focused on valuing growth assets and buying those assets at a discount. While valuation is the central focus in fundamental analysis, some analysts use discounted cashflow models to value firms, while others use multiples and comparable firms. Since investors using this approach hold a large number of 'undervalued' stocks in their portfolios, their hope is that, on average, these portfolios will do better than the market.

2. Activist Investors: Activist investors take positions in firms that have a reputation for poor management and then use their equity holdings to push for change in the way the company is run. Their focus is not so much on what the company is worth today but what its value would be if it were managed well. Investors like Carl Icahn, Michael Price and Kirk Kerkorian have prided themselves on their capacity to not only pinpoint badly managed firms but to also create enough pressure to get management to change its ways. How can valuation skills help in this pursuit? To begin with, these investors have to ensure that there is additional value that can be generated by changing management. In other words, they have to separate how much of a firm’s poor stock price performance has to do with bad management and how much of it is a function of external factors; the former are fixable but the latter are not. They then have to consider the effects of changing management on value; this will require an understanding of how value will change as a firm changes its investment, financing and dividend policies. As a consequence, they have to not only know the businesses that the firm operates in but also have an understanding of the interplay between corporate finance decisions and value. Activist investors generally concentrate on a few businesses they understand well, and attempt to acquire undervalued firms. Often, they wield influence on the management of these firms and can change financial and investment policy.

3. Chartists: Chartists believe that prices are driven as much by investor psychology as by any underlying financial variables. The information available from trading measures -- price movements, trading volume and short sales -- gives an indication of investor psychology and future price movements. The assumptions here are that prices move in predictable patterns, that there are not enough marginal investors taking advantage of these patterns to eliminate them, and that the average investor in the market is driven more by emotion than by rational analysis. While valuation does not play much of a role in charting, there are ways in which an enterprising chartist can incorporate it into analysis. For instance, valuation can be used to determine support and resistance lines[5] on price charts.

4. Information Traders: Prices move on information about the firm. Information traders attempt to trade in advance of new information or shortly after it is revealed to financial markets. The underlying assumption is that these traders can anticipate information announcements and gauge the market reaction to them better than the average investor in the market. For an information trader, the focus is on the relationship between information and changes in value, rather than on value, per se. Thus an information trader may buy an 'overvalued' firm if he believes that the next information announcement is going to cause the price to go up, because it contains better than expected news. If there is a relationship between how undervalued or overvalued a company is, and how its stock price reacts to new information, then valuation could play a role in investing for an information trader.

5. Market Timers: Market timers note, with some legitimacy, that the payoff to calling turns in markets is much greater than the returns from stock picking. They argue that it is easier to predict market movements than to select stocks and that these predictions can be based upon factors that are observable. While valuation of individual stocks may not be of much direct use to a market timer, market timing strategies can use valuation in one of at least two ways:

(a) The overall market itself can be valued and compared to the current level.

(b) Valuation models can be used to value a large number of stocks, and the results from the cross-section can be used to determine whether the market is over or under valued. For example, as the number of stocks that are overvalued, using the valuation model, increases relative to the number that are undervalued, there may be reason to believe that the market is overvalued.

6. Efficient Marketers: Efficient marketers believe that the market price at any point in time represents the best estimate of the true value of the firm, and that any attempt to exploit perceived market efficiencies will cost more than it will make in excess profits. They assume that markets aggregate information quickly and accurately, that marginal investors promptly exploit any inefficiencies and that any inefficiencies in the market are caused by friction, such as transactions costs, and cannot exploited. For efficient marketers, valuation is a useful exercise to determine why a stock sells for the price that it does. Since the underlying assumption is that the market price is the best estimate of the true value of the company, the objective becomes determining what assumptions about growth and risk are implied in this market price, rather than on finding under or over valued firms.

2. Valuation in Acquisition Analysis

Valuation should play a central part of acquisition analysis. The bidding firm or individual has to decide on a fair value for the target firm before making a bid, and the target firm has to determine a reasonable value for itself before deciding to accept or reject the offer.

There are special factors to consider in takeover valuation. First, there is synergy, the increase in value that many managers foresee as occurring after mergers because the combined firm is able to accomplish things that the individual firms could not. The effects of synergy on the combined value of the two firms (target plus bidding firm) have to be considered before a decision is made on the bid. Second, the value of control, which measures the effects on value of changing management and restructuring the target firm, will have to be taken into account in deciding on a fair price. This is of particular concern in hostile takeovers.

As we noted earlier, there is a significant problem with bias in takeover valuations. Target firms may be over-optimistic in estimating value, especially when the takeover is hostile, and they are trying to convince their stockholders that the offer price is too low. Similarly, if the bidding firm has decided, for strategic reasons, to do an acquisition, there may be strong pressure on the analyst to come up with an estimate of value that backs up the acquisition.

3. Valuation in Corporate Finance

There is a role for valuation at every stage of a firm’s life cycle. For small private businesses thinking about expanding, valuation plays a key role when they approach venture capital and private equity investors for more capital. The share of a firm that a venture capitalist will demand in exchange for a capital infusion will depend upon the value she estimates for the firm. As the companies get larger and decide to go public, valuations determine the prices at which they are offered to the market in the public offering. Once established, decisions on where to invest, how much to borrow and how much to return to the owners will be all decisions that are affected by valuation. If the objective in corporate finance is to maximize firm value[6] , the relationship between financial decisions, corporate strategy and firm value has to be delineated.

As a final note, value enhancement has become the mantra of management consultants and CEOs who want to keep stockholders happy, and doing it right requires an understanding of the levers of value. In fact, many consulting firms have come up with their own measures of value (EVA and CFROI, for instance) that they contend facilitate value enhancement.

4. Valuation for Legal and Tax Purposes

Mundane though it may seem, most valuations, especially of private companies, are done for legal or tax reasons. A partnership has to be valued, whenever a new partner is taken on or an old one retires, and businesses that are jointly owned have to be valued when the owners decide to break up. Businesses have to be valued for estate tax purposes when the owner dies, and for divorce proceedings when couples break up. While the principles of valuation may not be different when valuing a business for legal proceedings, the objective often becomes providing a valuation that the court will accept rather than the “right” valuation.

Conclusion

Valuation plays a key role in many areas of finance -- in corporate finance, in mergers and acquisitions and in portfolio management. The models presented will provide a range of tools that analysts in each of these areas will find of use, but the cautionary note sounded in this introduction bears repeating. Valuation is not an objective exercise, and any preconceptions and biases that an analyst brings to the process will find their way into the value.