Now what?

Now that the seminar is over, you are probably wondering what you should

do next to get ready for the "exam". Here are some questions you probably

have:

a. Where did the numbers in the valuations come from?

b. What equations/models do I need to know?

c. What will the exam look like?

What will be covered on the exam?

As promised in class, I will cover only what I did in class. In terms

of material, this will include all of the inputs into DCF valuation

and the loose ends. There will be nothing omn relative valuation.

Where did the numbers in the valuations come from?

We valued three companies in class - Amgen, Hyundai Heavy and Amazon. While

there were a lot of numbers that went into each valuation, the best way to

see the interplay of the numbers is to download the excel spreadsheets containing

each of the valuatons. Here are the links to the downloads:

Valuation

of Amgen

Valuation

of Hyundai Heavy Industries

Valuation

of Amazon - 2000

What equations/models do I need to know?

The equations that govern valuation are, for the most part, simple

and many are borrowed from other disciplines. In the table below, I have listed

almost every equation or variant that we used through the session, with illustrations

from Amgen and Hyundai Heavy backing them up. If you prefer his entire table

as a pdf file, please click

here.

Input |

Equation |

Examples from notes |

Riskfree Rate |

Long term, default free, currency-matched

rate. |

For Amgen, |

Equity Risk Premium (ERP) (Mature market) |

Can be estimated from

|

Geometric average ERP for US = 3.88%

(see page 23) |

Country Risk premium (CRP) (and total risk premium) |

Step 1: Get default spread for

country, based upon its sovereign rating.

|

For Korea |

Beta |

Can be estimated from

where wj = Weight of business j |

Amgen: Single business company (Pg

22) |

Lambda |

Measures company exposure to country

risk. Easiest way to estimate it is to use revenue exposure: |

Hyundai Heavy (Page 30) |

Expected Return (Cost of equity) |

If enough information provided

for estimating lambda |

For Amgen |

Pre-tax Cost of Debt |

If mature market company |

For Amgen in 2007 |

Debt |

For computing the cost of capital, debt should include:

|

For Amgen in 2007 (See page 14) |

Cost of capital |

Cost of equity (E/(D+E)) + Cost of Debt (1- marginal tax rate) (D/(D+E)) |

For Amgen, |

EBIT |

Start with the stated operating income, but adjust for:

|

For Amgen, (Pge 14-15) |

Capital Expenditures & Net Cap Ex |

Should include:

Net Cap ex = Cap Ex – Depreciation |

For Amgen, |

Non-cash Working Capital |

Non-cash Current Assets – Non-debt Current liabilities. |

For Amgen in 2007 |

FCFF |

EBIT (1- tax rate) – (Cap Ex – Depreciation) – Change in non-cash Working Capital |

For Amgen in 2007 |

Return on Capital |

|

For Amgen in 2007 |

Reinvestment Rate |

|

For Amgen in 2007 |

Expected Growth |

Reinvestment Rate * Return on Capital |

For Amgen |

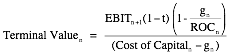

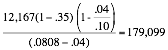

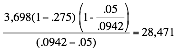

Terminal value |

|

For Amgen |

Value of Operating Assets today |

|

For Amgen: |

Value of firm today |

Value of Operating Assets |

For Amgen |

Value of equity today |

Value of firm today

|

For Amgen |

Value of equity per share |

Value of Equity today

/ Number of shares outstanding |

For Amgen |

What will the exam look like?

It will be a multiple choice exam. While I cannot give away

the game, suffice to say that it will be (a) straight forward and (b) require

only the most basic mathematics skills.