Buybacks Aid Europe's Stocks

Tool Turns Popular As Companies, Holders See It in a New Light

By SARA CALIAN

Staff Reporter of THE WALL STREET JOURNAL

August 23, 2004; Page C16

LONDON -- European companies increasingly are buying their shares back, pumping

up stock prices and winning over investors for their conservative use of cash

in a lackluster market.

In Europe, share buybacks, which were unpopular and not permitted under national

regulations in some countries six years ago, have increased in recent months.

European corporations have increased their cash flow in the past several years,

helping fuel the buyback trend. There also is a change in perception. Years

ago, a buyback was seen by many investors as a sign that the company didn't

have an acquisition strategy.

"Right now, the market would rather see companies use cash for buybacks

than put the cash in an investment that may or may not return something to

you," says Teun Draaisma, a market strategist at Morgan Stanley in London. "In

the late 1990s, investors took buybacks as a sign of defeat. The thinking was,

'If you need to buy back shares, you don't have anything else to do with the

money and it must be bad news.' But now share buybacks are seen as a healthy

sign."

"Right now, the market would rather see companies use cash for buybacks

than put the cash in an investment that may or may not return something to

you," says Teun Draaisma, a market strategist at Morgan Stanley in London. "In

the late 1990s, investors took buybacks as a sign of defeat. The thinking was,

'If you need to buy back shares, you don't have anything else to do with the

money and it must be bad news.' But now share buybacks are seen as a healthy

sign."

Indeed, Martin White, a Barclays Global Investors active equity strategist

in London, says his firm includes share buybacks in its criteria of stock selection,

and when the number of buybacks increases, it is sometimes used as a buy signal

for fund managers. "A company buying its own shares can be a positive

sign that management regards their stock price as representing good value," he

says. "It can also indicate an economy and discipline about how corporate

cash flows should be spent."

Stock repurchases are more common in the U.S., where for many years they served

as tax-efficient alternatives for corporations to paying higher dividends,

Mr. White says.

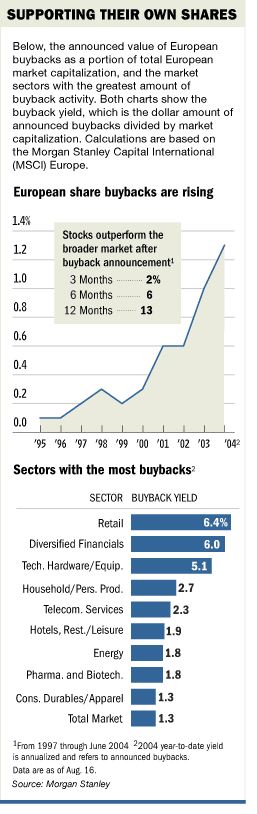

The U.S. buyback yield -- the dollar amount of announced buybacks divided

by companies' market capitalizations -- has increased in recent months, rising

to 2.3% for annualized 2004 data as of Aug. 16, which is a jump from 1.8% in

2003, according to Morgan Stanley. The yield has been above 1% for the past

decade.

The European buyback yield, using the same dollar calculations as the U.S.,

has more than doubled to 1.3% for 2004 as of annualized data for Aug. 16, compared

with 0.6% in 2002, according to research by Morgan Stanley. On average, if

an investor buys a European stock on the day it announces a buyback, there

is a 67% probability of outperforming the market 12 months after the announcement

and a 64% probability of outperforming the sector in 12 months, according to

the study.

Those are good odds considering the Dow Jones Stoxx 50 Index has fallen 3.47%

this year.

Still, some shareholders worry that companies aren't spending enough on growth

and development. "We are positive about share buybacks, but the market

shouldn't forget the need to look for growth," says Rolf Drees, a spokesman

for Union Investment in Frankfurt. "The number of share buybacks reflects

the market attitude toward chance and risk. Five years ago, everybody saw the

chance for an investment for growth, and now people overstate the risk of any

investment. Companies still need to look for opportunities to grow."

Many industries are taking part in the buyback boom, with some of the heaviest

activity in the retail, financial and energy sectors. For example, just this

month, the United Kingdom arm of Royal Dutch/Shell Group, Shell Petroleum Co.,

repurchased 1.9 million ordinary shares and Spain's Santander Central Hispano

SA repurchased more than 3.3 million shares. UBS AG conducted one of the biggest

share-buyback programs in Europe, buying some $14 billion (€11.4 billion)

of its shares since 1997 and it plans to buy more this year, according to Morgan

Stanley.

The telecommunications sector, which has been trying to pay down debt in the

past few years, is now freer to use its strong cash flow to offer an increasing

number of share buybacks, analysts say. Vodafone Group PLC is in the middle

of a program to buy back $14.2 billion of shares, which it announced in November

2003.

Andrew Milligan, global strategist at Standard Life Investments in Edinburgh,

Scotland, says share buybacks are one of the most important themes in the market. "Investors

like companies when they can give cash back," he says. "A lot of

investors are saying 'unless you have a very good idea, then why not give the

cash back to us.' "

Peter Oppenheimer, head of portfolio strategy at Goldman Sachs in London,

says corporations flush with cash have just a few options when it comes to

giving some money back to shareholders: increase the dividend, give a special

dividend or do a share buyback. "Most companies want to keep the dividend

steady. They don't want to raise it now and then have to meet higher expectations

every year," he says. "A share buyback makes more sense."

Write to Sara Calian at sara.calian@wsj.com