The

Little Book of Valuation

The

Little Book of Valuation

Looking for Relationships in the Data

When

there are two series of data, there are a number of statistical measures that

can be used to capture how the series move together over time.

Correlations and Covariances

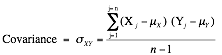

The two most

widely used measures of how two variables move together (or do not) are the

correlation and the covariance. For two data series, X (X1, X2,)

and Y(Y, Y. . .), the covariance provides a measure of

the degree to which they move together and is estimated by taking the product

of the deviations from the mean for each variable in each period.

The sign on the covariance indicates the type of relationship the two

variables have. A positive sign indicates that they move together and a

negative sign that they move in opposite directions. Although the covariance

increases with the strength of the relationship, it is still relatively

difficult to draw judgments on the strength of the relationship between two

variables by looking at the covariance, because it is not standardized.

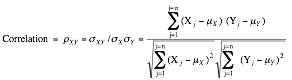

The

correlation is the standardized measure of the relationship between two

variables. It can be computed from the covariance :

The correlation can never be

greater than one or less than negative one. A correlation close to zero

indicates that the two variables are unrelated. A positive correlation

indicates that the two variables move together, and the relationship is

stronger as the correlation gets closer to one. A negative correlation

indicates the two variables move in opposite directions, and that relationship

gets stronger the as the correlation gets closer to negative one. Two variables

that are perfectly positively correlated (rXY = 1) essentially move in

perfect proportion in the same direction, whereas two variables that are

perfectly negatively correlated move in perfect proportion in opposite

directions.

Regressions

A

simple regression is an extension of

the correlation/covariance concept. It attempts to explain one variable, the

dependent variable, using the other variable, the independent variable.

Scatter Plots and Regression Lines

Keeping with statistical tradition, let Y be the dependent variable and X be the independent variable. If the

two variables are plotted against each other with each pair of observations

representing a point on the graph, you have a scatterplot, with Y on the vertical axis and X on the horizontal axis. Figure A1.3 illustrates a scatter plot.

Figure

A1.3: Scatter Plot of Y versus X

In a regression,

we attempt to fit a straight line through the points that best fits the data.

In its simplest form, this is accomplished by finding a line that minimizes the

sum of the squared deviations of the points from the line. Consequently, it is

called an ordinary least squares

(OLS) regression. When such a line is fit, two parameters emerge—one is

the point at which the line cuts through the Y-axis, called the intercept of the regression, and the other is

the slope of the regression line:

Y = a

+ bX

The slope (b) of the regression measures both the direction and the magnitude

of the relationship between the dependent variable (Y) and the independent variable (X). When the two variables are positively correlated, the slope

will also be positive, whereas when the two variables are negatively correlated,

the slope will be negative. The magnitude of the slope of the regression can be

read as follows: For every unit increase in the dependent variable (X), the independent variable will change

by b (slope).

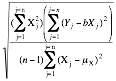

Estimating Regression Parameters

Although there are

statistical packages that allow us to input data and get the regression

parameters as output, it is worth looking at how they are estimated in the

first place. The slope of the regression line is a logical extension of the

covariance concept introduced in the last section. In fact, the slope is

estimated using the covariance:

![]()

The intercept (a) of the regression can be read in a number of ways. One

interpretation is that it is the value that Y

will have when X is zero. Another is

more straightforward and is based on how it is calculated. It is the difference

between the average value of Y, and

the slope-adjusted value of X.

![]()

Regression parameters are always

estimated with some error or statistical noise, partly because the relationship

between the variables is not perfect and partly because we estimate them from

samples of data. This noise is captured in a couple of statistics. One is the R2 of the regression, which

measures the proportion of the variability in the dependent variable (Y) that is explained by the independent

variable (X). It is also a direct

function of the correlation between the variables:

![]()

An R2 value close to one indicates a strong relationship

between the two variables, though the relationship may be either positive or

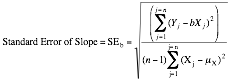

negative. Another measure of noise in a regression is the standard error, which

measures the “spread” around each of the two parameters estimated—the

intercept and the slope. Each parameter has an associated standard error, which

is calculated from the data:

Standard Error of Intercept = SEa =

If we make the additional

assumption that the intercept and slope estimates are normally distributed, the

parameter estimate and the standard error can be combined to get a t-statistic that measures whether the

relationship is statistically significant.

t-Statistic

for Intercept = a/SEa

t-Statistic

from Slope = b/SEb

For samples with more than 120

observations, a t-statistic greater

than 1.95 indicates that the variable is significantly different from zero with

95% certainty, whereas a statistic greater than 2.33 indicates the same with

99% certainty. For smaller samples, the t-statistic

has to be larger to have statistical significance.[1]

Using Regressions

Although

regressions mirror correlation coefficients and covariances in showing the

strength of the relationship between two variables, they also serve another

useful purpose. The regression equation described in the last section can be

used to estimate predicted values for the dependent variable, based on assumed

or actual values for the independent variable. In other words, for any given Y, we can estimate what X should be:

X = a

+ b(Y)

How good are these predictions? That

will depend entirely on the strength of the relationship measured in the

regression. When the independent variable explains a high proportion of the

variation in the dependent variable (R2 is high), the predictions

will be precise. When the R2 is low, the predictions will have a

much wider range.

From Simple to Multiple Regressions

The

regression that measures the relationship between two variables becomes a

multiple regression when it is extended to include more than

one independent variables (X1, X2, X3,

X4 . . .) in trying to explain the

dependent variable Y. Although

the graphical presentation becomes more difficult, the multiple regression yields output that is an extension of the simple

regression.

Y = a

+ bX1 + cX2 + dX3 + eX4

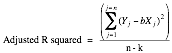

The R2 still measures the strength of the relationship, but

an additional R2 statistic

called the adjusted R2 is

computed to counter the bias that will induce the R2 to keep increasing as more independent variables are

added to the regression. If there are k independent variables in the

regression, the adjusted R2

is computed as follows:

Multiple regressions are powerful

tools that allow us to examine the determinants of any variable.

Regression Assumptions and Constraints

Both the simple

and multiple regressions described in this section also assume linear

relationships between the dependent and independent variables. If the

relationship is not linear, we have two choices. One is to transform the

variables by taking the square, square root, or natural log (for example) of

the values and hope that the relationship between the transformed variables is

more linear. The other is to run nonlinear regressions that attempt to fit a

curve (rather than a straight line) through the data.

There are implicit

statistical assumptions behind every multiple regression that we ignore at our

own peril. For the coefficients on the individual independent variables to make

sense, the independent variable needs to be uncorrelated with each other, a condition

that is often difficult to meet. When independent variables are correlated with

each other, the statistical hazard that is created is called multicollinearity. In its presence, the

coefficients on independent variables can take on unexpected signs (positive

instead of negative, for instance) and unpredictable values. There are simple

diagnostic statistics that allow us to measure how far the data may be

deviating from our ideal.