Handout for Chapter 3. International Indicators

Trade Balance, Current Account and Capital Flows

Current Account Transactions:

1. Merchandise Balance = Exports - Imports of Goods

2. Net Exports (Trade Balance, NX) = Merchandise Balance plus Net Exports of Services Figure 1

3. Current Account Balance (CA) = Trade Balance + Net Factor Income from Abroad ( = NX + i NFA).

A country running a CA deficit must finance this deficit through net borrowing from the rest of the world (i.e. either by by increasing its net debt or by reducing its net foreign assets).

The cash flows measured by the current account are mirrored by equal and offsetting financial cash flows, which we refer to as the capital account. Issue analogous to the statement of cash flows for a firm (as seen in Table 1). A firm with a negative (positive) net cash flow from operations must balance this with an equal and opposite source (use) of cash from financial transactions.

If NFA is the net stock of foreign assets held by people in the United States (US ownership of foreign assets, net of foreign ownership of US assets), then (excepting changes in asset valuation) changes in NFA are equal to the current account:

NFAt+1 = NFAt + CAt .

NFAt+1= NFAt + GDPt + it x NFAt - Ct - Gt - It = NFAt + CAt

Another way of seeing the relation between the CA and the NFA of the country: link between the current account of the BP (that records current transactions, i.e. trade in goods and services and the interest payments on net foreign assets) and the capital account of the BP (that records capital transactions, i.e. the purchase and sale of foreign assets). Note that:

NFA = Foreign Assets (FA) - Foreign Liabilities (FL) =

= US Assets Abroad - Foreign Assets in the US

Define capital outflows and capital inflows as:

Change in Foreign Assets = Capital Outflows = FAt+1 - FAt = Change in assets we buy/hold abroad (including the change in loans we make to foreigners)

Change in Foreign Liabilities = Capital Inflows = FLt+1 - FLt = Change in liabilites we owe to foreigners (including the loans/borrowings that foreigners make to us)

Capital Account of BP = Capital Outflows - Capital Inflows

CAt = NFAt+1 - NFAt = [(FAt+1 - FLt+1)- (FAt - FLt+1)]

= - [(FLt+1 - FLt) - (FAt+1- FAt)] = - KAt

i.e. the capital account is:

KAt = Capital inflows - Capital outflows

This implies that the overall balance of payments is always equal to zero:

CAt + KAt = 0 = BPt

When the current account is in a surplus (CA>0), we are on net accumulating foreign assets and therefore the capital account is in a deficit (KA < 0): capital outflows are greater than capital inflows. When the current account is in a deficit (CA<0), we are on net decumulating foreign assets (or increasing our net foreign liabilities) and therefore the capital account is in a surplus (KA>0): capital inflows are greater than capital outflows. The overall balance of payments must, by accounting definition, be always equal to zero because any current account transaction has and equal and corresponding transaction in the capital account.

Example: US in 1988 (see the table in the Economic Report of the President)

CAt = NFAt+1 - NFAt = - KAt

-122 = -145 - (-23) = - (-122)

or:

CAt = - [(FLt+1- FLt) - (FAt+1- FAt)] = - KAt

-122 = - [(1918-1648) - (1773-1625)] = - 122

-122 = - [270 - 148] = -122

Current Account Balance = -122 (Actual 1988 figure: -127 giving a statistical discrepancy of $5 b))

Capital Account = +122 of which:

Capital Inflows: 270; Capital Outflows: 148

Note: Foreign Assets (Liabilities) are the sum of Official and Private Foreign Assets (Liabilities) (see Table 1).

Nominal and Real Exchange Rates and the PPP

Exchange rates. We use the convention that prices of foreign currency are expressed in dollars. This leads to the confusing result that increases in the exchange rate are decreases in the value of the dollar. Note: the financial sector convention is to define the exchange rate of the US $ as units of foreign currency per units domestic currency (daily data shown here), i.e. Yen per US dollars, that is the opposite of the convention we follow here ($ per Yen). (If confused, use an on-line Currency Convertor).

Our Definition:

The Exchange Rate is the Dollar Price of Foreign Currency

S$/YEN = Dollars needed to buy one Yen (say 8.6 US cents)

S$/DM = Dollars needed to buy one DM (say $ 0.67)

If S increases the Dollar is Depreciating (it takes more $ to buy one unit of foreign currency).

If S decreases the Dollar is Appreciating (it takes less $ to buy one unit of foreign currency).

Alternative Definition (used in financial markets):

The Exchange Rate is the Foreign Currency Price of a US $

SYEN/$ = Yen needed to buy one US$ (say 116 Yen=1/0.008). See Figure2

SDM/$ = DM needed to buy one US $ (say 1.49 DM= 1/0.67). See Figure 3

Exchange rates are very variable (see the Minneapolis Fed home page for updated Charts of U.S. exchange rates relative to a basket of currencies).

Exchange rates are related to prices of foreign and domestic goods. Example:

P = price in $ of a unit of a domestic good (one gallon of gas, say $1.20)

Pf = price in units of foreign currency of the same good in a foreign country (say DM 2.0)

Which good is more expensive ? The price in dollars (P$f) of a unit of the foreign good is equal to its price in foreign currency (Pf = DM 2) times the exchange rate of the dollar relative to the foreign currency (S = 0.67):

P$f = S Pf = 0.67 x 2 = 1.34

The relative price of the foreign good to the domestic good (defined as RER):

RER = S Pf / P = 1.34 / 1.20 = 1.166

where S is the (spot) exchange rate. The good in Germany is 16.6% more expensive (when expressed in same currency) than the same good in the U.S.

Often we use price indexes, like CPI or GDP deflators, representing baskets of goods. In this case the ratio RER is referred to as the real exchange rate. It indicates how expensive foreign goods are relative to domestic goods.

If domestic and foreign goods were very similar, and there were few barriers to trade, then when expressed in the same currency their price should be equal. In this case the RER would be equal to one and show no change.

In fact, if the price ratio differed from one, buyers in Germany would only buy in the cheap country (US), driving up prices there until foreign and domestic prices were equal. Thus prices of foreign and domestic goods, expressed in a common currency, should be the same, leading the RER to stay around one.

This theory, applied to the baskets of goods underlying aggregate price indexes, is referred to as purchasing power parity, (or PPP) since the purchasing power of a dollar is predicted to be the same in both countries:

P = S Pf

In the example above instead:

P =1.20 < S Pf =1.34 (divergence from PPP)

So how, can we reach a PPP equilibrium when the relative price differs from unity ? There are three alternative ways the equlibrium can be restored:

1. German prices could fall from DM 2 to DM 1.79 so that: P=1.20=SPf=0.67x1.79

2. US prices may go up from $1.20 to $ 1.34 so that: P=1.34=SPf=0.67x2.00

3. The $/DM exchange rate could appreciate from 0.67 to 0.60 so that: P=1.20= S Pf = 0.60 x 2.00

In practice, all of the three effects will be at work in reality.

What is the evidence on the PPP ? If the PPP holds, the real exchange rate (RER) should be equal to one and constant over time. In fact,

RER = S Pf / P = P / P = 1 (if the PPP holds).

However, we find, when we compute RER using consumer price indexes, that it varies a lot: prices of (say) Mercedes in particular, and goods in general, are often much different in Germany and the US, and between any two other countries, as well. At least in the short-run, the PPP is a poor approximation.

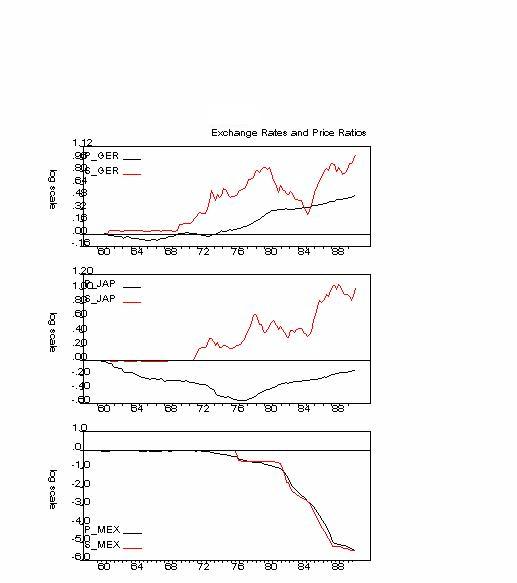

Moreover, most of the variation in the RER is related to movements in the spot rate: see Figure 4 . In Figure5 the real exchange rate is divided into two components: the ratio P/Pf is the solid line and the spot rate S is the dashed line. If PPP were true, the two lines would be the same (as PPP implies S = P/Pf). In fact they're much different.

Why the PPP dpes npt hold in the short-run ? We assumed that the domestic and foreign goods were identical (a gallon of gasoline). However, the RER represents basket of domestic and foreign goods that can be very different. Also, for homogenous goods, firms may price discriminate across markets.

While the PPP may not hold in the short-run, it should tend to hold in the long-run: if German prices are systematically higher than U.S. ones, at some point they will have to fall or US prices will have to go up, or the US $ will have to appreciate (or all of the above).

To understand the role of the exchange rate as an adjustment mechanism for relative prices and the trade balance, note the following points:

1. A depreciation (appreciation) of the domestic exchange rate makes foreign imported goods more expensive (cheaper) when priced in domestic currency. So a currency depreciation (appreciation) will lead to a reduction (increase) in the demand for imported goods as these goods become more expensive (cheaper). This reduction (increase) in the demand for imports should improve (worsen) the US trade balance.

2. A depreciation (appreciation) of the domestic exchange rate makes domestic goods exported abroad cheaper (more expensive) when priced in a foreign currency. So a currency depreciation (appreciation) will lead to a increase (decrease) in the foreign demand for US goods, i.e. an increase (decrease) in US exports as these goods become cheaper (more expensive) in foreign markets. This increase (decrease) in the US exports will improve (worsen) the US trade balance.

In particular:

1. A US$ appreciation decreases the price in US $ of imported goods (P$f) as: P$f =S Pf . So, a $ appreciation (an decrease in S) will decrease P$f . Example:

P$f = S Pf = 0.67 x 2 = 1.34

P$f = S Pf = 0.60 x 2 = 1.20

1. A US Dollar appreciation increases the price in foreign currency (DM) of US goods exported abroad (PDM ) since:

PDM = P / S. So, a $ appreciation (an decrease in S) will increase PDM. Example:

PDM = P / S = 1.20 / 0.67 = 1.79

PDM = P / S = 1.20 / 0.60 = 2.00

So, a depreciation of the nominal exchange rate (S) will lead to an increase in the relative price of foreign to domestic goods, i.e. it will lead to a depreciation of the real exchange rate (RER). In fact:

RER = S Pf / P = P$f / P

If the price in own currency of domestic and foreign goods (P and Pf) is given, a nominal depreciaton of the exchange rate will also be a real depreciation.

Note: if the PPP was holding both in the short-run and the long-run, a nominal depreciation of the domestic currency would not lead to a depreciation of the real exchange rate. For given foreign prices of foreign goods, a nominal depreciation would increase proportionally by the same amount the price of imported goods and of domestic goods leaving the RER unaffected.

So, the PPP can be interpreted both as a theory of the determinant of the exchange rate and as a theory of the determinant of the domestic price level (or inflation rate). As theory of the exchange rate, the PPP can be written as:

S = P / Pf (1)

or, if we write the expression above in percentage rates of change:

dS/S = dP/P - dPf/Pf (2)

where dx/x is the percentage rate of change of variable x.

The expression (1) says that the exchange rate will be more depreciated if the domestic price level is higher than the foreign one (absolute PPP).

In rate of change form (relative PPP), expression (2) says that the exchange rate will depreciate at a % rate equal to the difference between domestic and foreign inflation. Example: if domestic inflation is 10% while foreign inflation is 4%, the domestic currency should depreciate on average by 6%.

The PPP, as a theory of the determinants of the exchange rate, considers the causality between P and S as going from domestic inflation to exchange rate depreciation: high inflation causes high depreciation rates.

As a theory of the determinants of the domestic inflation instead, the PPP considers the causality as going from the exchange rate to domestic inflation:

dP/P = dS/S + dPf/Pf (3)

(3) implies that, for given foreign inflation, the domestic inflation rate will be equal to the foreign inflation rate plus the 'exogenous' rate of depreciation of the domestic currency. For example, if foreign inflation is 4% and the domestic currency is depreciated by 20%, domestic inflation will be equal to 24%.

Of course, if the PPP does not strictly holds (at least in the short-run), the RER will not be always equal to one and constant and a depreciation of the nominal exchange rate will also depreciate the real exchange rate.

By how much will the real exchange rate depreciate if the nominal exchange rate depreciates by x% ?

1. If the domestic price level was completely independent of the nominal exchange rate, the domestic inflation rate would be totally unaffected by a nominal depreciation. In this case, the real exchange rate would depreciate by x% as well. This is an extreme case where the increase in the price of imported goods caused by the nominal depreciation does not affect at all the price of domestic goods.

2. If an x% nominal depreciation leads to an increase in domestic inflation (but by less than the x% implied by the PPP), the real exchange rate will depreciate but, by less than x%. In fact, by definition:

dRER/RER = dS/S + dPf/Pf - dP/P

Example: Mexico in 1995. Foreign (US) inflation was 3% while the Mexican Peso depreciated during the year by about 107%. If the Mexican inflation in 1995 has remained at the 1994 level (about 8%), the 107% nominal depreciation would have corresponded to a real depreciation of 102% (107 + 3 - 8). The large devaluation of 1995 led to an increase in the inflation rate that surged to 48% in 1995. So, the nominal depreciation of the Peso of 107% corresponded to a smaller real depreciation of 52% (107 + 3 - 48). Major improvement of the Mexican trade balance in 1995.

Implication. A currency devaluation is a double-sided sword:

1. On one side, it leads to a real depreciation that makes imported goods more expensive, domestic exports cheaper abroad and leads to an improvement of the trade balance via a fall in imports and an increase in exports.

2. On the other side, a nominal depreciation leads to an increase in domestic inflation that dampens the effect of the nominal devaluation on the real exchange rate.

The faster domestic inflation adjusts to the change in the exchange rate (i.e. the closer we are to the PPP in the short-run), the smaller will be the real depreciation following a nominal depreciation, the smaller will be the improvement in the trade balance and the bigger the increase in domestic inflation.

Interest Rates and Exchange Rates

There are substantial differences in interest rates across countries.

Covered interest parity: interest rates denominated in different currencies are the same once you "cover'' yourself against possible currency changes. The argument follows the standard logic of arbitrage in finance.

Compare two equivalent strategies for investing one US dollar.

First strategy: invest one dollar in a 3-month eurodollar deposit. After three months that leaves you with (1+i) dollars, where i is the dollar rate of interest expressed as a quarterly rate (the annualized rate of 4.19% divided by 4).

Second investment strategy has a number of steps:

1.Convert the dollar to DMs, leaving us with 1/S DMs if S is the spot exchange rate in $/DM.

2. Invest this money in a 3-month DM deposit, earning the quarterly rate of return if (f for foreign). Here if is the annualized rate of return 9.52% divided by 4. That leaves us with (1+if)/S DMs after three months. We could convert at the spot rate prevailing three months from now, but that exposes us to the risk that the DM will fall. So, an alternative is:

3. To sell DMs forward. In January 1992 we know we will have (1+if)/S DMs that we want to convert back to dollars. With a three-month forward contract, we arrange now to convert them at the forward rate F expressed, like S, as $/DM. This strategy leaves us with (1+if)F/S dollars after three months.

Thus we have two relatively riskless strategies, one yielding (1+i), the other yielding (1+if)F/S. Which is better? Well, if either strategy had a higher payoff, you could short one and go long the other, earning huge profits with no risk. Since banks are not in the business of letting you make money this way, so they make sure that these prices are set so that the returns are equal:

(1 + i) = ( 1 + if) F/S

We call this equation the covered interest parity condition (CIPC).

Example with January 1992 numbers. i= (4.19 % divided by 4), if = (9.52% divided by 4), S=0.6225 (62 cents per DM), F=0.6114 (so it's cheaper to buy DMs forward than spot).

The covered interest parity can be also written in a simpler form:

(1+i) = (1 + if) F/S = (1 + if) [1 + (F-S)/S] = (1 + if)(1 + fp) =

= (1+if+ fp + if fp)

where fp (the forward premium) is the percentage difference of the forward rate from the spot rate. Since the term (if fp) is close to zero, this parity condition becomes approximately:

i = if + fp

Or: i - if = fp

i.e. the domestic interest rate is equal to to the foreign rate plus the forward premium.

This gives you a simple rule: if the domestic interest rate is above the foreign rate by x%, the forward exchange rate (for the maturity equivalent ot the interest rate) will be above (i.e. depreciated relative to) the spot rate by x%.

If you cover your foreign positions with a forward contract, that sense there's no point worrying about whether to invest in dollars or DMs. But what if, in strategy two, you converted at the spot rate in a quarter (three months form now) and took your chances on the exchange rate? Your return would then be

(1+itf) St+1 / St ,

where by St+1 is the spot rate a quarter (3 months) from now.

Suppose now that agents are risk-neutral, i.e they care only about expected returns. Then, expected return on investing in a domestic asset for a period (a quarter) is (1 + i) while the expected return (as of today time t) of investing in a foreign asset is:

(1+itf) E(St+1)/St

where is the expectation I have today (time t) of what the spot exchange rate will be a quarter (3 months) from now.

If agents are risk-neutral and care only about expected returns, the expected return to investing in a domestic asset must be equal to the (uncertainan as of today) expected return on investing in the foreign asset. This is what is called the uncovered interest parity condition(UIPC):

(1+it ) = (1+itf) E(St+1) / St ,

where E(xt+1) again means the expectation today (t) of the value at time t+1 of the variable x.

Note: this is not a riskless arbitrage opportunity as the ex-post future spot rate may be different from what we expected it to be. Rearranging the expression above, we can rewrite the uncovered interest parity condition as:

i = if + dSe/S = if + (E(St+1) - St)/St

or : i - if = dSe/S

where dSe/S is the expected percentage depreciation of the domestic currency.

Simple rule: if the UIPC holds, a x% difference between the interest rate at home and abroad must imply that investors expect that the domestic currency will depreciate by x%.

Given that covered interest parity works, uncovered interest parity amounts to saying that the forward rate today (delivery of currency at time t+1) is the market's expectation of what the spot rate will be a period from now:

ft = E(St+1).

More generally, since forward contracts can be signed for any maturity:

Ftt+k = E(Ft+k)

where Ftt+k is the forward rate today for delivery of currency at time t+k and E(St+k) is today's market's expectation of what the spot rate will be t+k periods from now. [For some forecasts (expectations) of future exchange rates you can check out the home page of Olsen & Associates ].

This expectations hypothesis implies that if the forward rate is less than the current spot rate (Ft < St , as in the example above), we should expect the spot rate to appreciate: E(St+1) < St.

What is the evidence on the uncovered interest parity condition. Is is true that when domestic interest rates are above (below) foreign ones, the exchange rate will depreciate (appreciate) ?

Consider again the UIPC; it implies that the expected depreciation of a currency is equal to te differential between domestic and foreign interest rates:

dSe/S = i - if

Now, we know from the Fisher Condition (see Chapter 2) that high interest rates can be due to two factors: high real rates or high expected inflation. So, substituting the Fisher Condition we get:

dSe/S = (r - rf) + (p - pf)

Two cases:

1. Domestic real interest rate are equal to foreign interest rates. In this case, the domestic nominal interest rate can be above the foreign rate only if the domestic country is expected to have a higher inflation rate than the foreign country. In this case, it makes sense to believe that higher interest rate at home will lead to a currency depreciation.

In fact, by the PPP, higher inflation is associated (sooner or later) with a currency depreciation and the higher interest rate at home reflects only the higher expected inflation of the home country.

This implication is confirmed by the data: countries with high inflation have, on average, higher nominal interest rates than countries with lower inflation and, on average, the currencies of such high inflation countries tend to depreciate at a rate close to the interest rate (or inflation) differential relative to low inflation countries.

2. Domestic inflation is equal (or close to) the foreign inflation rate. In this case higher interest rates at home do not reflect higher domestic inflation but rather higher real interest rates due for example to a tight monetary policy by the central bank. In this case, we would expect that high domestic interest rates will be associated with an appreciating currency (as the high interest rates lead to an inflow of capital to the high yielding country).

In fact, the last twenty years suggests that, for periods of time when US inflation is close to the German one, the US appreciates (relative to the DM) when US interest rates are above the German ones. This is a contradiction of the UIPC but it reflects the effect of high real interest rates on currency values. See a recent discussion by the chief currency economist for Morgan Stanley for an argument based on this yield effect.

So, will a positive difference in dollar and DM rates reflects a prediction that the DM will fall ? The expectations hypothesis says yes. But 20 years of experience with floating exchange rates for major currencies suggests that we should expect, instead, a rise in the DM.

Good rules of thumb are (i) high interest rate currencies (of countries with low inflation) generally increase in value and therefore (ii) expected returns are higher in the high interest rate currency.

Caveats: US$/Yen Exchange rates in the 1994-1997 period.

Further Web Links and Readings

You can find more Web readings on the topics covered in this chapter in the course home page on Macro Analysis and the page on Macro Data sources.

A. Statement of Cash Flows. Mack Truck, 1989.

Sources (+) Minuses (-) Uses of Cash (Thousands)

| Cash Flows from Operating Activities | 9,458 |

| Cash Flows from Financial Activities | |

|

Investing |

(93,354) |

|

Financing |

83,896 |

|

Net |

(9,458) |

B. Balance of International Payments, US, 1993.

Sources (+) Minuses (-) Uses of Funds (Billions)

| Cash flow from current transactions | |

|

Exports |

755.5 |

|

Imports |

(827.3) |

|

Interest, profits, transfers, etc. (net) |

(32.1) |

| Current account balance | (103.9) |

| Cash flow from financial (capital) transactions | |

|

Private US purchases of foreign assets |

(146.2) |

|

Private foreign purchases of US assets |

159.0 |

|

US government purchases of foreign assets |

(1.7) |

|

Foreign government purchases of US assets |

71.7 |

|

Capital account balance |

82.8 |

|

Statistical discrepancy |

21.1 |

Panel A is adapted from Rose Marie Bukis Financial Statement Analysis (Chicago: Probus, 1991), p.114. Panel B is adapted from the US Commerce Department's Survey of Current Business, December 1994, pp.30ff.