|

|||

|

|||

There are many companies that operate in multiple businesses. While the motives for this push into multiple businesses is varied and sometimes merited (synergy, shared costs etc.), it does create scenarios where a company can find itself having to allocate capital across these businesses, with very different risk profiles. If the company fails at this task, its value will suffer, and the company may find itself targeted by activist investors seeking a breakup of the company. Not all activist moves for breakups are well thought through or well intentioned but they all have the effect of bringing to the surface the different characteristics (risk, growth and cash flows) of the many businesses that comprise a single company. That discussion may be uncomfortable for managers but it is a good one to have.

While the push for breaking up companies has been around as long as markets have been around, there seems to be an increase in activity on this dimension. Start with this Wall Street Journal story that points out that not only are more companies being targeted for break ups, but that the targeted companies are getting bigger.

http://online.wsj.com/news/articles/SB10001424052702304899704579391190297827908

As you look at the companies highlighted in this article, they range the spectrum from natural resource companies to consumer product companies.

The Sony Bid

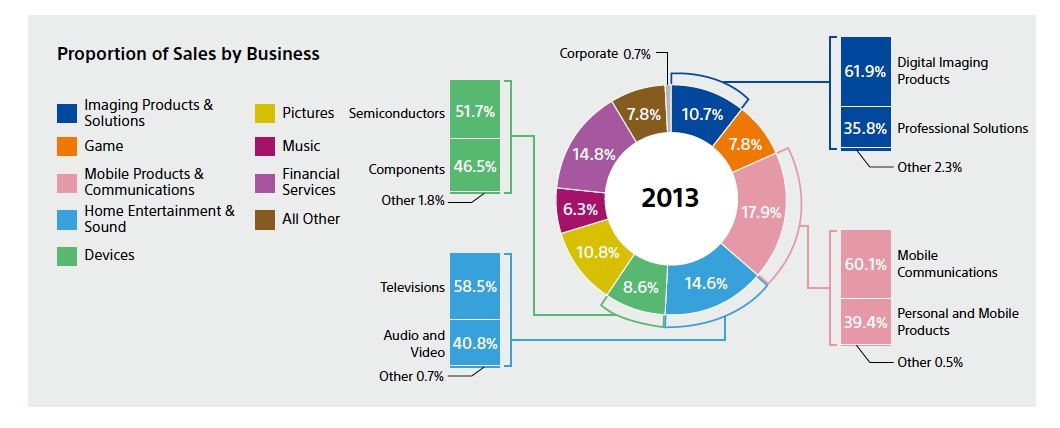

Sony may be an iconic Japanese name brand but it has had a tough decade, losing a hundred billion (not a typo) in market capitalization over the last decade. It has also managed over the last two decades to spread itself across multiple business, broadly categorized into entertainment and electronics, with each of these businesses having sub-businesses. In fact, taking a look at the annual report from 2013 for Sony, here is the picture of the range of their businesses:

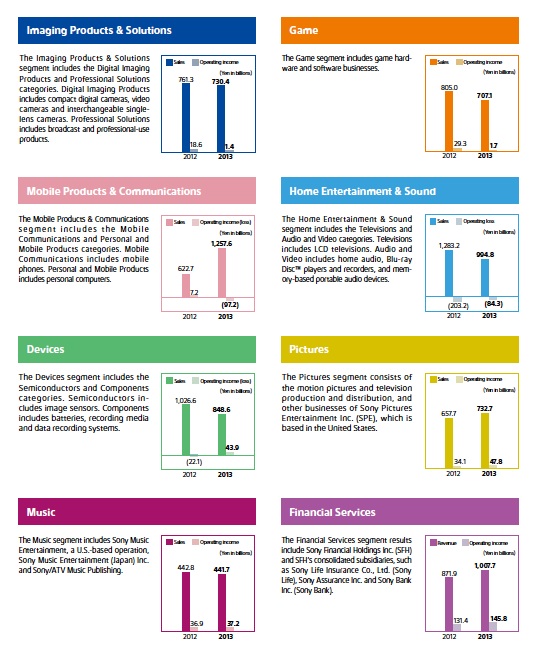

If you are wondering what is in each of these groupings, the following page may or may not help you:

It was a surprise to some people when Dan Loeb targeted Sony for a breakup last summer. You can start with the news stories about the bid:

News story: http://www.bloomberg.com/news/2013-05-15/sony-s-100-billion-lost-supports-loeb-breakup-real-m-a.html

You Tube video: http://www.youtube.com/watch?v=mtwzGevk58A

Sony's response was predictable, insofar that it rejected the break up bid:

http://rt.com/business/sony-loeb-rejected-japan-107/

The story is not over. Loeb continues to be one of Sony's largest stockholders and is still pushing for a break up.

http://www.bloomberg.com/news/2014-02-09/sony-woes-seen-prelude-to-loeb-inspired-breakup-real-m-a.html

Key Questions