|

|||

|

|||

The emails for this class will be collected on this page, arranged chronologically. Since I send quite a few, you can target it on a specific month by going here:

Have fun with them!

Date |

Email content |

| 1/17/22 | Welcome back! As I checked through the roster, I noticed a lot of familiar names from corporate finance, and you know that the email deluge that awaits you.I am sure that you are finding that break is passing by way too fast, but the semester will soon be upon us and I want to welcome you to the Valuation class. One of the best things about teaching this class is that valuation is always timely (and always fun...) Just as examples: Is it time to sell Tesla? Was WeWork worth any money ever or was Softbank delusional, and if the latter, what does that make Oyo? Is Cathie Woods a genius or just bonkers? How much does a Super Bowl add to an NFL team’s value? You will find the answers to these and other questions on my blog:

1. Preclass work: I know that some of you are worried about the class but relax! If you can add, subtract, divide and multiply, you are pretty much home free… Seriously, all I need of you is a familiarity with basic finance, accounting and statistics. If you feel shaky, you may want to check out the online classes that I have on accounting and financing basics:

2. For this class: If you want to get a jump on the class, you can go to the class web page:

As the schedule stands right now, we will meet on Mondays and Wednesdays from 1.30 pm - 2.50 pm in Paulson Auditorium, starting on January 31, but with COVID still wreaking havoc on our lives, who knows what will play out? I have had quite a few frantic emails from some of you, but you know as much as I do at the moment. If the classes get moved online, never fear. Zoom will come to the rescue. If you have to miss a class or two, because the classes will be recorded and available on three platforms:

When you get a chance, check it out.

3. If you are going to be away or are worried about COVID exposure: Even if we do meet in class, I know that some of you are wary about coming to class, either because you have been exposed to COVID or are worried about exposure. Obviously, I would like you to come to class, if you can, but if you cannot, for any reason, the classes will be both live zoomed and recorded and you can watch the recordings the same day as the class. At the moment, the quizzes and exams are in person, but again, there is much that is out of our hands.

4. Syllabus & Calendar: The syllabus for the class is available on the website for the class and is also linked here:

and there is a google calendar for the class that you can get to by clicking on

https://calendar.google.com/calendar/u/0?cid=Y181MGd2ZjBwOTA2dWxqdm 02cnVkdnFnZDhvZ0Bncm91cC5jYWxlbmRhci5nb29nbGUuY29t

For those of you already setting up your calendars, it lists when the quizzes will be held and when projects come due.

5. Lecture notes: The first set of lecture notes for the class is ready.You can either print off the slides, or save them online. .

Please download and print only this packet on discounted cashflow valuation.

6. Books for the class: The best book for the class is the Investment Valuation book - the third edition. (If you already have the second edition, don't waste your money. It should work...) You can get it at Amazon or wait and get it at the book store... If you are the law-abiding type, you can buy "Damodaran on Valuation" - make sure that you are getting the second edition. Or, as a third choice, you can try The Dark Side of Valuation, again the second edition, if you are interested in hard to value companies.. Or if you are budget and time constrained, try "The Little Book of Valuation". Finally, if you really want to take a leap, try my newest book, Narrative and Numbers at

You will find the webpages for all of the books at http://www.stern.nyu.edu/~adamodar/New_Home_Page/public.htm. If you want a comparison of the books, try this link: https://pages.stern.nyu.edu/adamodar/New_Home_Page/valbookcomp.html

7. Valuation apps: One final note. I worked with Anant Sundaram (at Dartmouth) isn developing a valuation app for the iPad or iPhone that you can download on the iTunes store: http://itunes.apple.com/us/app/uvalue/id440046276?mt=8

It comes with a money back guarantee... Sorry, no Android version yet…

I am looking forward to seeing you in two weeks in class, or if God has other plans, online. Let’s hope that the world holds together until then! Until next time!

|

| 1/24/22 |

It’s been a week since my last email, and while not a whole lot has happened, I thought I should check in ahead of next week’s class. First, if this is the first email you are reading, then you should catch up with the earlier one, which are available at the link below:

If you are wondering about the logistics (exams, projects etc.), we will start the first class with the syllabus, which will also lay out the themes for the class:

As you go through the syllabus, you will notice mention of a project and you can find the details of that project here:

Once we are through the syllabus in session 1, we will turn to an introductory packet (of about 20 pages). The link to that package is below:

Please have this ready for the first session. The rest of the class will be covered in the lecture note packets, and I sent you the link to the first one last week (but here it is again):

Having drowned you with all of that stuff, let me hit with you some pre-class reading (and I don’t think it is too painful). I don’t do much academic research and am supremely uninterested in writing for an echo chamber. Much of what I have written that is original or different has be initially (at least) on my blog. I spend the first few weeks of each year, talking about the data that I update on my website:

The first two updates are on my blog. Please browse through them, because they are relevant for class:

The first class will be six days from today (Monday, January 31, from 1.30 pm - 2.45 pm, NY time) in Paulson Auditorium. Please do come, if you can. If you are unable to, either because of logistical or health reason, the class will be carried on Zoom. The Zoom link for all of the classes (all 28 sessions) is below:

Until next time!

|

| 1/29/22 | It’s been a week since my last email, and while not a whole lot has happened, I thought I should check in ahead of next week’s class. First, if this is the first email you are reading, then you should catch up with the earlier one, which are available at the link below:

If you are wondering about the logistics (exams, projects etc.), we will start the first class with the syllabus, which will also lay out the themes for the class:

As you go through the syllabus, you will notice mention of a project and you can find the details of that project here:

Once we are through the syllabus in session 1, we will turn to an introductory packet (of about 20 pages). The link to that package is below:

Please have this ready for the first session. The rest of the class will be covered in the lecture note packets, and I sent you the link to the first one last week (but here it is again):

Having drowned you with all of that stuff, let me hit with you some pre-class reading (and I don’t think it is too painful). I don’t do much academic research and am supremely uninterested in writing for an echo chamber. Much of what I have written that is original or different has be initially (at least) on my blog. I spend the first few weeks of each year, talking about the data that I update on my website:

The first two updates re on my blog. Please browse through them, because they are relevant for class:

The first class will be six days from today (Monday, January 31, from 1.30 pm - 2.45 pm, NY time) in Paulson Auditorium. Please do come, if you can. If you are unable to, either because of logistical or health reason, the class will be carried on Zoom. The Zoom link for all of the classes (all 28 sessions) is below:

Until next time!

|

| 1/31/22 | We are officially rolling. If you enrolled in the class in the last couple of days, you did miss the first two emails but they are already in the email chronicle, in case you are interested:

Email chronicles: http://www.stern.nyu.edu/~adamodar/New_Home_Page/eqemail.html

This chronicle will be updated at the end of each week to include all emails sent up until then.

If you were able to make it today’s class, thank you, and the slides that we used for the class should be at the links below:

Introduction to Valuation (Slides for Wednesday’s class): https://pages.stern.nyu.edu/adamodar/pdfiles/eqnotes/Valintrospr22.pdf

I mentioned the project for the class, but only in very general terms. You can find the specifics at the link below:

A quick note about today's class. During the session, I told you that that this was a class about valuation in all of its many forms – different approaches (intrinsic, relative & contingent claim), different forums (for acquisitions, value enhancement, investing) and across different types of businesses (private & public, small and large, developed & emerging market). After spending some time laying out the script for the class (quizzes, exams, weekly tortures), I suggested that you start thinking about forming a group and picking companies. To get the process rolling, here is what I have done

1. Group: Please do find a group to nurture your valuation creativity, and a company to value soon. If you are ostracized, or feel alone, I will create an orphan list and make sure that you are adopted.

2. Company Choice: Once you pick a company, collect information on the company. I would start off on the company's own website and download the annual report for the most recent year (probably 2019) and then visit the SEC website (http://www.sec.gov) (for US listings) and download 10Q filings. (You can pick any publicly traded company anywhere in the world to value. The non-US company that you value can have ADRs (but does not have to have ADRs) listed in the US but you still have to value it in the local currency and local market. You can even analyze a private company, if you can take responsibility for collecting the information.)

3. Webcast of today’s class: The web casts for the first class are up and running in all of their variations (Zoom recording, downloadable video, downloadable audio and YouTube). You can access it by going to: 4. Lecture Note Packets: Please download the first lecture note packet, when you get a chance. You can either download it as a powerpoint file (though powerpoint bloats file size or as a pdf file)

Powerpoint slides: http://www.stern.nyu.edu/~adamodar/pptfiles/val3E/valpacket1spr22.pptx

5. Post class test: To review what we did in class today, I prepared a very simple post-class test. I have attached it, with the solution. Give it your best shot. |

| 2/1/22 | The second valuation of the week is upon you, and it is of a company that evokes strong views in both directions, Tesla. I valued Tesla for the first time in 2013, and have valued it every year since, and it still surprises me how much disagreement there is among investors on its future. There are some who believe that Tesla is destined to be the greatest company ever, a beacon of hope that will be worth trillions of dollars. There are others who seem to think of the entire company as a scam, with nothing. Not surprisingly, what you think about Tesla is tied to how you feel about Elon Musk as a person. I have always tried to navigate a middle ground, conceding to the optimists that Tesla is a unique companies that has changed the automobile business and to the pessimists that it is personality-driven and sometime oddly behaved (for a company…I have called it my corporate teenager). To get a sense of my history with Tesla, and where I stand at the moment, take a look at this blog post:

Once you have read the post, open up this spreadsheet, and you will notice that the master input page, which is the only page that you have to touch, does not require any knowledge of valuation details, but just a sense of your Tesla story:

Make your judgments on each of the key dimensions, from the end game for Tesla (in terms of revenues), to the margins you expect it to earn to its risk, and come up with your valuation of the company. Once you are done, please go to this shared Google spreadsheet and enter your numbers:

https://docs.google.com/spreadsheets/d/15gIfz8R7Ve_ke6E1FEulSRzTyBKqkI9XsmunMn6txnw/edit?usp=sharing

Note that when I valued the company in early November, I estimated a value close to $680 billion, and that is very optimistic assumptions, but the market cap was more than $1.2 trillion, making the stock over valued by about 78%. The market cap has dropped by about a third, since this valuation and in your assessment, you may very well find it to be under valued. |

| 2/2/22 | Today's class started with a test on whether you can detect the direction bias will take, based on who or why a valuation is done. The solutions are posted online on the webcast page for the class. We then moved on to talk about the three basic approaches to valuation: discounted cash flow valuation, where you estimate the intrinsic value of an asset, relative valuation, where you value an asset based on the pricing of similar assets and option pricing valuation, where you apply option pricing to value businesses. With each approach, we talked about the types of assets that are best priced with that approach and what you need to bring as an analyst/investor to the table. For instance, in our discussion of DCF valuation and how to make it work for you, I suggested that there were two requirements: a long time horizon and the capacity to act as the catalyst for market correction. We will be starting on the first lecture note packet on Monday. So, please have it downloaded and ready to go. |

| 2/3/22 | It is never too early to start nagging you about the project. So, let me get started with a checklist (which is short for this week but will get longer each week. Here is the list of things that would be nice to get behind you:

In doing all of this, you will need data and Stern subscribes to one of the two industry standards: S&P Capital IQ (the other is Factset). It is truly a remarkable dataset with hundreds of items on tens of thousands of public companies listed globally, including corporate governance measures. To get access to Capital IQ, you need to ask for it, and the attached document leads you through the process. As with all things IT related, I am sure that there are glitches and if you find them, let me know.

On a completely unrelated note, it may be a little early to be talking to me or the TAs, but here are the logistical details on office hours (for all of us) and the TA review sessions that will occur every week:

My office hours: On Zoom, since NYU is not allowing in-person yet, will be at: https://nyu.zoom.us/j/92119670806

For most weeks, my office hours will be from 5 pm - 6 pm on Mondays and 12 pm - 1 pm on Wednesdays. I will add on more hours as we get closer to quizzes and exams and project due dates.

TA office hours

Lianda and Dylan surveyed you to find the best times for office hours and review sessions. They will be having a review session from 10 am - 11 am, on Fridays, and office hours, right after. They will be setting up zoom sessions on Brightspace soon.

|

| 2/4/22 | As promised, here is the first of the weekly in-practice webcasts. These are 10-15 minute webcasts designed to work on practical issues in corporate finance. This week’s issue is a timely one, if you are working on picking companies for your project (as you should be..). It is about the process of collecting data for companies, the first step in understanding and analyzing them. The webcast link is below:

It is a little dated (but I have been too lazy to update it), but I don’t think it is too painful to watch, and you may even find it useful. I have also put the link up on the webcast page for the class:

The webcasts for the first two classes should be on there, if you missed (physically, metaphysically or mentally) and the links to the project and syllabus that I handed out in the class. You can stream or YouTube the sessions, or download videos/audios. Also, if you joined the class late, you can get all emails sent up till today here:

Finally, have you had a chance to look at the weekly puzzle? If not, give it a shot by going here:

At the risk of nagging, please do get the lecture note packet 1 downloaded before Monday’s class. It is now available (or was at least yesterday) in the bookstore. |

| 2/5/22 | hope that you are enjoying your first weekend back at school. I will intrude with a couple of notes.

1. Teaching Fellows/Review sessions: Just a reminder about the TAs for this class. There are two:

They will have office hours and a review session each week. The times and zoom links are on NYU classes.

2. Newsletter: The first newsletter for the class is attached. As I said, there is usually not much news in these newsletters. Think of it more as a timeline for the class, telling you where we went last week and laying out our plans for the week ahead. If you get a chance, take a look at it.

3. Need a group member: I normally don’t play matchmaker, but there is only one person on the orphan list, and if you have room in your group, you may consider adding him.

Ioannis Wallingford, iew8836@stern.nyu.edu

He is a tech MBA and obviously will bring skills to your group that you will find useful (Excel and skydiving, based on his skill notes). Please reach out to him, if you are interested, and see if this could be mutually beneficial. Finally, we will be starting with the first lecture note packet in class on Monday. Please have it with you for class. The pdf version can be found here:

Have a great weekend! Until next time!

Attachment: Issue 1 (February 5) |

| 2/6/22 | First things first. This week, we will be delving into the mechanics of discount rates, starting with the risk free rate and then moving on to the equity risk premium. They are both central to valuation and we live in unusual times, where the former, in particular, is doing strange things. Second, we will be starting off tomorrow's class with the question of firm versus equity valuation. I am attaching the cash flow table that we will be using for the start-of-the-class test as well. If you get a chance, please take a look at it before you come into class. The question is at the bottom of the page. Until next time! Attached: Valuation bias: A test |

| 2/7/22 | Today's class started with a look at a major investment banking valuation of a target company in an acquisition and why having a big name on a valuation does not always mean that a valuation follows first principles, with the first principle being We began our intrinsic value discussion by talking about the weapons of mass distraction. If you want to read the blog post I have on the topic, try this link:

After setting the table for the key inputs that drive value - cash flows, growth, risk, we looked at the different ways of approaching valuation (Dividend Discount model, FCFE model, firm valuation) and the roots that they share, and how they result in different estimation processes. Next session, we will start with a discussion of risk free rate, a foundational number that will drive the rest of our calculations. I have attached a post class test for today, with the solution. Until next time!

|

| 2/8/22 | For this week, I thought I would switch gears and value a very different company from last week’s hot mess which was Tesla. This week, I look at Aramco, a company that became the most valuable public company (in terms of market cap) over night, when it had its IPO in 2019. The place to start this valuation is with the Aramco IPO, a document written by bankers for bankers, and hence thoroughly boring:

You can follow up with two posts that I wrote at the time of the IPO:

The excel spreadsheets containing my valuation of Aramco is here:

Clearly, much water has passed under this bridge in the last two years, and I have the updated numbers for Aramco through 2021 at the link below;

Finally, if you feel up to it, please do go enter your updated valuations for Aramco, with the updated market cap of just over two trillion into the Google shared spreadsheet:

https://docs.google.com/spreadsheets/d/1fpYkDkdsBmAw1edMJNtpaRZ1PrD29bAyvpo4mylp0Kg/edit?usp=sharing

Good luck and have fun!

|

| 2/9/22 | We started the class with a discussion the different groupings of risk, and why some types of risk matter more than others, before moving on torisk free rates, exploring why risk free rates vary across currencies and what to do about really low or negative risk free rates. The blog post below captures my thoughts on negative risk free rates:

If you want to see my updated perspective on risk free rates, try my blog post from this year, built around the inflation question is here:

We just started on the discussion of equity risk premiums but the contours of the discussion should be clear.Historical equity risk premiums are not only backward looking but are noisy (have high standard errors). You can the historical return data for the US on my website by going to

Click on current data, and look to the top of the table of downloadable data items. Finally, The post class test and solution are attached. One last note. It is Wednesday and time for the first weekly challenge, and it relates to the consistency of equity versus firm valuation. I have attached it and will post my solution by Sunday night. Until next time!

Attachments: Post-class test and solution, Weekly challenge #1 |

| 2/10/22 | By now, you should have a company picked, and if so, you can start thinking about at least the first two pieces of your discount rate calculation, a risk free rate and an equity risk premium.

That’s about it for the moment. |

| 2/11/22 | It is Friday, andI have put up the webcast for risk free rates on the webpage for the class.

Risk free Rates

Additional material:

It will of course make more sense, if you have picked a company and have a currency to work with, but that is a nag for a different days II hope that you get a chance to watch the webcast! Until next time!

|

| 2/12/22 | 2. Company choice & groups: I was checking the valuation master sheet:

I notice that a lot of you have not picked a company yet. If you have already and have just not entered the company name (not symbol), please do so.

3. FANGAM Stocks: If you are valuing one of the FANGAM stocks. I just put up a post on my views on these companies. Don’t do anything crazy, like changing companies just because I have a valuation on what you picked. Your story will be different from mine. That’s why we do valuation

Until next time!

|

| 2/13/22 | I hope that you have had a good weekend and that you are watching the Super Bowl, not reviewing your valuation notes. Two quick loose ends to tie up. First, I hope that you had a chance to watch the in-practice webcast on the risk free rate ). Second, I sent you a weekly challenge last Wednesday. I don’t know whether you had a chance to try, but it is still not too late. I have attached the solution to that weekly challenge (and the weekly challenge, in case you have no idea what I am talking about). Tomorrow, we will complete our risk free rate discussion, before turning our attention to equity risk premiums, talking about forward-looking estimates and we will then move on to the cost of debt and capital. So, if you are shaky about any of those concepts, I hope that you are rock solid, by the end of the week. Until next time! Attachment: Weekly challenge #1 & Solution |

| 2/14/22 | In the session today, we started by doing a brief test on country risk premiums. After a brief foray into lambda, a more composite way of measuring country risk, we spent the rest of the session talking about the dynamics of implied equity risk premiums and what makes them go up, down or stay unchanged. We then moved to cross market comparisons, first by comparing the ERP to bond default spreads, then bringing in real estate risk premiums and then extending the concept to comparing ERPs across countries. Finally, I made the argument that you should not stray too far from the current implied premium, when valuing individual companies, because doing so will make your end valuation a function of what you think about the market and the company. If you have strong views on the market being over valued or under valued, it is best to separate it from your company valuation. I am attaching the excel spreadsheet that I used to compute the implied ERP at the start of February 2022. Play with it when you get a chance. Post class test and solution attached. Until next time!

|

| 2/15/22 | Moving right along, it is time for the valuation of the week, and this week’s company bears no resemblance to your first two. It is Heineken, the Dutch brewer, with a worldwide brand name. The reason that I am focusing on the company is not because I like its product, but because this is a valuation that I first did in September 2019, in Euros, when the risk free rate was negative in that currency. Begin by reading this post on negative interest rates from 2016:

You can continue by reading this piece that provides the background for the company and my valuation:

You can download the historical data on the company through 2021 here:

You can download my valuation from February 2021 here;

You are welcome to update the valuation to include the additional quarter of information that has come out, but not much has changed. Try playing with the risk free rate/stable growth rate combination, and I use the word “play” deliberately, since you are messing with first principles when you do so. If nothing else, this will give you bragging rights, since 99% of people who do valuation for a living have not only never valued a company with negative risk free rates, but many in this group will claim it cannot be done. You can say it can and will be done. Until next time!

|

| 2/16/22 | In today’s class, we started by reviewing the pitfalls of regression betas. They are backward-looking, noisy and subject to game playing. We went on to talk about bottom up betas, focusing on defining comparable firms and expanding the sample. I did make a big deal about bottom up betas, but may have still not convinced you or left you hazy about some of the details. If so, I thought it might be simpler to just send you a document that I put together on the top ten questions that you may have or get asked about bottom up betas. I think it covers pretty much all of the mechanics of the estimation process, but I am sure that I have missed a few things.

It is also time for the next weekly challenge, and this one is built around using statistics to make sense of time movements in equity risk premiums. It is on the webpage for the class. Please give it a shot, when you get a chance. One final note. There is no class next Monday and next week’s class (on Wednesday) will be an entirely zoom class. The link is on Brightspace, but I will send it to you again next week. Until next time!

|

| 2/17/22 | First things first. By now, I hope that you are in a group and have picked a company. If so, please complete the process by going to the master spreadsheet for the class and input your company name:

https://docs.google.com/spreadsheets/d/1QJmg1HTrIBPGo4Bo_8-rUY5Mwwk9D1M5fEPgpFNB82Y/edit?usp=sharing

At this stage in the class, you should be able to complete three basic tasks related to discount rates, estimating risk free rates, equity risk premiums and betas. Along the way, you have to get comfortable with how to estimate implied equity risk premiums, and to further you on that path, I will be posting valuation tools webcasts on estimating implied equity risk premiums and company exposure to equity risk. Also, please do try this week’s challenge, since it will give you perspective on equity risk premiums and how they relate to riskfree rates and default spreads. I know that I drown you sometimes in stuff related to the class, from weekly challenges to valuations of the week, and it can be overwhelming. If you are feeling lost in the class, and don’t even know where to begin, my advice is that you go to the entry page for the class:

Everything to do with this class, from the recorded sessions (in case you missed any of them) to the weekly challenges to all emails sent out should be accessible from there. The webcast page for the class has the slides that go with each session, and post class tests and solutions. Until next time! |

| 2/18/22 | This week in class, we moved from risk free rates to looking at equity risk premiums and beta. This week, I have added two tools webcasts.

Implied Equity Risk Premiums

Webcast: https://www.stern.nyu.edu/~adamodar/podcasts/Webcasts/ImpliedERP.mp4

The supporting materials are below: Presentation: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/ERP/ImpliedERP.ppt Implied ERP spreadsheet (from February 2013): https://www.stern.nyu.edu/~adamodar/pc/implprem/ERPFeb13.xls S&P on buybacks (from earlier this year): https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/ERP/SP500buyback.pdf S&P 500 Earnings: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/ERP/SP500eps.xls Company Equity Risk Premium

If you remember, we started this discussion in class by looking at how to measure company risk exposure to country risk, using Embraer, Ambev and Coca Cola, using revenue weights, and then looking at Royal Dutch, where we used oil production weights. In this week’s valuation tool’s webcast, I look at estimating a company’s risk exposure to country risk.

Supporting data: https://www.stern.nyu.edu/~adamodar/pc/datasets/ERP&GDP.xls

Of course, the table you see in this webcast with GDP and ERP is an old one, and you can get the updated version here:

Give it a look, when you get a chance.

On a different note, I have a YouTube video on how to use Bloomberg to get basic data on your company.

For those of you wondering how I got a Bloomberg terminal installed in my home (I am currently in s sunny San Diego), I did not. What I used instead is a really neat interface called Bloomberg Anywhere that you can use to make your terminal mimic a Bloomberg. If you are in New York, and can access a terminal at Stern (I sent you the locations), you should, but I have learned that you too have access to Bloomberg Anywhere, as a Stern student. I have attached the instructions on how to use it in the document below, but keep in mind that there are only a handful of connections that Bloomberg allows at any one time. (Read the document to the end to see why). Given that constraint, you should plan your Bloomberg expedition with purpose, and be ready to get the stuff you need quickly. For the moment, I would like you to get on, if you can, and print off three Bloomberg pages for your company as soon as you can:

If you play this right, it will take only a few minutes, and if you don’t have a printer, just take pictures of each of these pages. Until next time!

|

| 2/19/22 | Last week, we continued on our discussion of discount rates by looking at how best to estimate the equity risk premium. This coming week, we have only one session on Wednesday, and it will be a zoom session. In that session, we will complete the discussion of cost of capital, and start on the meat and potatoes part of valuation, which is cash flows. In the meantime, attached is the newsletter for the week. Also, there are a couple of people in this class who have been unable to find groups for the class. If you are willing to add a person to your group, please let me know. Until next time! Attachment: Issue 3 (February 19)

|

| 2/20/22 | This week, we will complete our discussion of hurdle rates and move on to murkier territory, where we estimate earnings and cash flows. I hope you had a chance to try the weekly challenge. If you did, the solution is at the link below.

Give it a glance, if you have the time! Please remember that we have no class tomorrow. Until next time!

|

| 2/21/22 | No class today, but a preview of what’s coming next week. The first quiz is on March 2nd and I wanted to cover some logistical details.

1. Quiz location and timing: The quiz will be on Wednesday, March 2. It will been in class in the first 30 minutes of class (1.30 - 2 pm, NY time), in Paulson Auditorium, and there will be class after the quiz. It is open-book, open-notes, but you cannot use your laptop. The quiz is 10% of your grade. If you are unable to be in the room physically, because you are trapped in another location or have entered the witness protection program, you can take the class online, but only during the same time window. (I know that this is a pain in the neck, if you are in Asia, but I cannot think of a fair and equitable way to do this, which will not render it unfair to others.). To use this option, you need to sign up in the Google shared spread sheet that I have created for those using this option.

https://docs.google.com/spreadsheets/d/1K1t28sRPdimaw-zuOOxOJzbpAzcDalOxwIPmbC3JWkM/edit?usp=sharing

2. Quiz coverage: The quiz will cover everything through the end of cash flows (though page 162), which we will get to, in the next two sessions; growth is not on this quiz. It will therefore include the big picture sessions on valuation, discount rates and cash flows.

3. Past quizzes: I am posting the links to the quizzes from just the past few years. While there are older quizzes you can cover, these are much more relevant for the quiz at hand.. If you do run into a growth question, skip it.

Practice quizzes: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/shortquiz1.pdf

Practice quiz solutions: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/shortquiz1sol.xls

As you work through these quizzes, please do remember that while the new quiz will resemble past quizzes, it will not be replica.

4. Quiz review webcast: I have a webcast that I have put together where I take you through the material that will be covered on the quiz. It is about 35 minutes long and it may help you get ready for the quiz (or not)…

5. Quiz office hours: I have added an extra two hours of office hours next Tuesday, from 9 am - 11 am, New York time. if you have questions.

Join URL: https://nyu.zoom.us/j/99862440067

See you online for Wednesday’s zoom class. The link to that class is on Brightspace, but I will send it tomorrow as well.

|

| 2/22/22 | Before I dive into the valuation of the week for this week, a reminder again that tomorrow’s class will be on zoom and the zoom link is below:

See you in class at the regular time (1.30 pm - 2.50 pm)

My valuations of the week are usually on individual companies, and this semester, we have already looked at Airbnb, Heineken and GameStop. This week, I am doing something different, but one where every investor has a stake in the outcome. I want to value the S&P 500 index, using the same principles that allow me to value a company. You can start with a blog post at the start of this year, where I valued the S&P 500:

Read to the end of the post for the valuation, but it is a simple one based upon expected earnings and cash flows on the index. My valuation of 3360, at the start of the year, was about 12% below the index level, but that reflects my assumptions. They are in this spreadsheet:

Please download the spreadsheet, and change the assumptions that you feel comfortable changing, valuing the index as of today. Note that, if nothing else, you can update the riskfree rate to what it is today and the index level. Once you are done, you can enter the numbers in a shared Google spreadsheet:

https://docs.google.com/spreadsheets/d/1jlrOWNv3LXQ1f1sYc_zWEwckix55lw5GuMdbP-xaJLI/edit?usp=sharing

Not only is this an extremely useful exercise in regaining investment serenity, but it is the antidote to the nonsense you will hear from CNBC market gurus this week. Give it a shot, and you too can be a market guru! Until next time! |

| 2/23/22 | In today’s class, we started with the cost of debt and computing debt ratios for companies and how to deal with hybrid securities.. If you are interested in getting updated default spreads (on the cheap or free), try the Federal Reserve site in St. Louis:

These are spreads on indices created by rating, updated daily. Neat, right? You can get the spreads from Bloomberg as well, using the FIW function, and tweaking the choices to show all corporate spreads.

We then moved on to getting the base year's earnings right and explored several issues:

1. To get updated numbers, you should be using either trailing 12 month numbers or complete the current year with forecasted numbers. In either case, your objective should be to get the most updated numbers you can for each input rather than be consistent about timing.

2. To clean up earnings, you have to correct accounting two biggest problems: the treatment of operating leases as operating (instead of financial) expenses and the categorization of R&D as operating (instead of capital) expenses. The biggest reason for making these corrections is to get a better sense of how much capital has been invested in the business and how much return this capital is generating. I know that we have not covered R&D expense capitalization in class, but I think you can still try it. Post class test and solution attached, as is the weekly challenge. Until next time! Attachments: Post class test and solution, Weekly challenge #3 |

| 2/24/22 | I was going to remind you of the project and working on it, but if you are turning your attention to the quiz, you may be checking out the links I sent yesterday for the past quizzes and solutions. Since the link I sent yesterday included only a subset of the quizzes and stopped in 2016. If you want more quizzes to practice on, try these for all the quizzes through 2019, and remember to work backwards, since the earlier quizzes may have slightly different coverage:

Past quiz solutions: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/quiz1sol.xlsx

I hope that you find some time to not just review the lecture notes, but work through the practice problems. In fact, it is the working through problems, using the lecture notes as a guide, that will provide the deepest learning. Until next time! |

| 2/25/22 | I know that you have big and fun plans for the weekend and it is my job to ruin them. If you feel the urge to catch up on your project, I am going to give you the capacity to do so by getting trailing 12-month data on your company:

http://www.stern.nyu.edu/~adamodar/podcasts/Webcasts/Trailing12month.mp4 (Uses Apple from late 2012)

The most productive use of the webcast is to download the most recent annual and quarterly reports for your company and work with your company’s numbers. You may get lucky, if your company has a calendar year-end and has just reported its fourth quarter 2021 numbers, in which case your most recent 12 months and the most recent fiscal year will match. If you do have access to S&P Capital IQ (gentle nudge to get that access as soon as you can), you can get trailing 12 month numbers. The other plus of Capital IQ is that you can get historical data for your company in any currency you want. Until next time!

|

| 2/26/22 | I know that you are busy and I have a guess about what you are working on. I have attached the newsletter, on the odd chance that you may want to take a look at it. I As you prepare for the quiz, try not to drive yourself into a frenzy. It is just a quiz, just 10% and if you do badly, you can make it go away. That said, it is better to do well than badly. So, good luck and see you in class on Monday. Until next time! Attachment: Issue 4 (February 26) |

| 2/27/22 | In tomorrow’s session, we will continue on the path of estimating earnings and getting to cash flows. Along the way, we will have to deal with leases, R&D, one-time charges, accounting malfeasance and other potential pitfalls. Nothing that we do is particularly difficult or hard to understand, but the details will pile on top of each other. Just to get you ready, you may find my latest data update post for 2022 relevant:

It looks at the profitability of companies around the world in 2021, and tries to draw lessons. On Wednesday, your will be taking the quiz in the first 30 minutes of class, and a reminder that if you are taking the quiz online (at exactly the same time), you need to put your name down in the Google shared spreadsheet:

https://docs.google.com/spreadsheets/d/1K1t28sRPdimaw-zuOOxOJzbpAzcDalOxwIPmbC3JWkM/edit?usp=sharing

Also, the quiz is open book, open notes and you can use your iPad/Tablet/laptop to access the lecture note slides. If you want all quizzes that I have given from 1997 to 2019, you can get them at the links below:

I think it is over kill, but whatever makes you happy.

Finally, I will have two extra office hours on Tuesday, and I have scheduled it for 9 am - 11 am, New York timef. The link to Zoom is here, and I will see you there:

Time: Mar 1, 2022 09:00 AM Eastern Time (US and Canada)

Join Zoom Meeting

See you tomorrow in class! Until next time! Attachments: Weekly challenge #3 & Solution |

| 2/28/22 | We continued our discussion of cash flows, by first putting to rest some final issues on earnings, including the tax rate to use in computing after-tax cash flows and dealing with money losing companies. In the process, we did look at what to do about accounting fraud, and while the answer is not much, there may be a role for forensic accounting. To be honest, most forensic accounting books are designed for valuation morticians, but here are a couple that you may find useful:

We then moved on to examine broad questions about what to include in capital expenditures and working capital, before putting the cash flow topic to rest by working out debt cash flows and cash flows to equity. Next session, we will continue with a discussion of growth rates but remember that the quiz in the first half an hour of class., but there will be class afterwards. Another reminder is that I will be having office hours tomorrow, on zoom, from 9 am - 11 am, NY time. (Link was in yesterday’s email) Until next time! |

| 3/1/22 | First things first! The quiz is tomorrow from 1.30 -2.00, and there will be class afterwards. There are two groups will not be in Paulson and here are the logistical plans for these groups:

1. Extra time/accommodations: If you signed up with the Moses Center for extra time and/or accommodations, you will be taking your exam at the Moses Center. They have the exam already, and you should be all set.

2. Online exam takers; If you are signed up to take the class online, I have decided that the best way to make this work smoothly is to put the exam on Brightspace, and you will be able to access it by 1.25 pim tomorrow, and you have 30 minutes to take it, and submit it back on Brightspace. You will entering your answers directly into Birghtspace. So, no need for printers or copies. This is the first time that I have given an exam on Brightspace (since we transitioned from NYU Classes) and I hope it works smoothly. Note that access to the Brightspace quiz is available only to those people who signed up on the Google sheet for online exams. (The exam on Brightspace is not a multiple choice exam. You will be working through problems and showing your work in Brightspace).

On a different note, today is the day that you get the valuation of the week. Rather than hit with you another company valuation, I thought I would try something lighter.So, let’s have some fun. I have always been a Star Wars fan, and like other fans, I was a little worried when Disney bought Lucas Films (and with it the rights to the Star Wars franchise) for $4 billion a few years ago. Disney was explicit about its plans at the time, and said that it planned to produce three major Star Wars movies, continuing the story, and three side stories (like Rogue One) filling in history. I went to see Force One in December 2015 and wrote this post on my blog about what I thought the value of Star Wars was at the time;

I assigned a value of almost $10 billion to the franchise, with a big chunk coming from the side products (toys, software, apps) coming from the franchise. You can download the spreadsheet that contains the valuation here:

When I wrote the post, Force Awakens had been out in theaters only a few days and I estimated box office revenue of $2 billion for the movie. Rogue One, of course, had not been released yet and I estimated revenues of $1 billion. Force Awakens is now one for the history books, with global revenues of just over $2 billion and Rogue One crossed the $1 billion threshold.

Updated box office for Force Awakens: http://www.boxofficemojo.com/movies/?id=starwars7.htm

Updated box office for Rogue One: http://www.the-numbers.com/movie/Rogue-One-A-Star-Wars-Story#tab=summary

In addition, the eighth Star Wars movie has come and gone, with the Last Jedi, as has the next add on movie on Hans Solo:

Updated box office for The Last Jedi: https://www.boxofficemojo.com/movies/?id=starwars8.htm

Updated box office for Solo: https://www.boxofficemojo.com/movies/?id=untitledhansolostarwarsanthologyfilm.htm

The final movie in this trilogy, The Rise of Skywalker came out in 2019. You can get the updated box office numbers for all of these movies here:

In addition, it looks like Star Wars is going to be central to Disney Plus making inroads into the streaming business. The Mandalorian was the most-watched series last year, and those Baby Yodas sold out for Christmas (merchandising again) and Wandavision looks like it is going to be a hit as well. That adds a value stream that did not exist a few years ago. Armed with this additional information, here is what I would like you to do. Go into the spreadsheet and reestimate the value of the Star Wars franchise. It may be only tweaks but give it your best shot. Once you have a value, go into this shared Google spreadsheet:

https://docs.google.com/spreadsheets/d/1teC7Hoiyt9zRYeQR4-GgCW4Batalqv8rUUvuxrKGT7I/edit?usp=sharing

Enter your numbers and lets see how the distribution of values evolves over time. And since this is a Star Wars post, might as well end with some good advice from Yoda: Have fun, you must!

|

| 3/2/22 | I hope that you have put the quiz behind you, good or bad. I will let you know when the quizzes are ready to pick up, and send the solutions and the grading template. In the session, which occurred after the quiz i, we started on our assessment of growth rates, starting with historical growth rates, before looking at analysts estimates of growth and why they do not carry more predictive power (given that analysts often are immersed in company-specific knowledge and have access to management). We then looked at tying growth to two fundamental questions: (1) how much companies reinvest and (2) how well. The way we measure these can vary depending on whether you look at earnings per share, net income or operating income. The weekly challenge for this week, if you feel up for it, centers on fundamental growth. Try it, if you get a chance. Until next time! Attachments: No post class test |

| 3/3/22 | Want them or not, your quizzes are done. Here are the details on how you can pick them up and check your score:

If you are unable to pick up your quiz, your score should still be accessible on Brightspace. Needless to say, if you have issues with the grading, I will be glad to talk with you. Since physical office hours still seem to be a no-no, I will set up a zoom link for those with grading questions to come in

Attachments: Quizzes and Solutions |

| 3/4/22 | I am probably pushing my luck, since I have taken up so much of your time this week, with the quiz. If you feel the urge to catch up on your project, I am going to give you the capacity to do so by posting two in-practice webcasts:

1. Converting leases to debt: I have also posted a second webcast on converting leases to debt which takes you through the process of which numbers to use in this conversion and how to deal with loose ends (like the lump sum that is often given for past 5 years).

2. Converting R&D to capital expenditures: We have net covered how to capitalizet R&D expenses in class yet, but you can get a jump on the process with this webcast. I use Microsoft from a year gone by to illustrate this concept:

How to capitalize R&D: https://www.stern.nyu.edu/~adamodar/podcasts/Webcasts/R&D.mp4

Microsoft 10K 2011: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/R&D/Microsoftlastyear10K.docx

Microsoft 10K 2012: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/R&D/Microsoft10K.docx

If you get a chance, please watch one or both of these webcasts. Until next time!

|

| 3/5/22 | This may be your weekend to forget valuation, but I am afraid that I have to intrude. The most recent newsletter is attached. A reminder also that your quizzes are ready to pick up on the ninth floor of the finance department. Until next time! Attachment: Issue 5 (March 5) |

| 3/6/22 | In the coming week, we will complete the last pieces of intrinsic value, talking about growth in all of its forms tomorrow and the terminal value on Wednesday. This is hard to believe but we are close to half way through the semester. So, if you have not picked a company, you should. If you have, you should have the financials. If you have the financials, you should be working on the valuation. I think you get the picture. I have also attached the solution to the weekly challenge. If your reaction is what weekly challenge, I don’t blame you. Until next time! Attachment: Weekly Challenge Solution |

| 3/7/22 | In today’s session, we started by looking at fundamental growth in all its variants. With EPS, net income and operating income, we argued that the long term or sustainable growth rate for a firm is a function of how much it reinvests and how well it reinvests, with the measurement of each varying depending upon the earnings metric. We then looked at the possibility of efficiency growth in the short term, as ROE or ROIC change, and finally at the most general way of estimating cash flows, where we start with revenues, then forecast margins and tie up loose ends with reinvestment, tied to sales. In the final part of the session, we looked ways to keep the terminal value from running away with your valuation by capping growth, limiting the growth period and reinvesting enough to sustain growth. I have two reading suggestions if you are interested. First, I mentioned my incredibly boring paper on accounting returns. You can find it here:

Consider yourself forewarned. The blog posts that I have on terminal value may be more up your alley:

They capture everything we talked about in class today.

|

| 3/8/22 | Airbnb was one of the highest profile IPOs of 2020, and as the IPO approached, and before the bankers priced it, I posted my valuation for Airbnb, with my story:

You will notice that for an IPO valuation, there is an added input for IPO proceeds and IPO share count, but the bottom line is that I valued the equity of Airbnb at about $35-40 billion. As with any IPO, the numbers all come from a prospectus and I have a link to the final prospectus that Airbnb filed on December 2:

Now that Airbnb has been public for a while, I first obtained the updated financials for the company:

I updated my valuation to March 2022 to reflect its public status and its filings since going public.

Note that the value per share that I estimate has increased, as the company came back much more strongly than expected in 2021, and is about $61 billion. In the meantime, the stock has lost a chunk of value over the last year and now trades at about $100 billion. There are five drivers of value for Airbnb:

Change what you want, leave all else alone and come up with your own value. Then, please go to the Google shared spreadsheet and enter your inputs. Let the games begin:

|

| 3/9/22 | In today’s class, we started by looking at building a DCF model, and then talked about the loose ends in valuation, i.e., all the things you do after you have discounted cash flows back at the discount rate and why they matter. We started with cash, the simplest and most direct of all assets to value, and talked about why investors may attach a premium or discount to the cash balance of a company, arguing that discounts reflect a lack of trust in management. I mentioned a paper that looks at how the market discriminates across companies, when it comes to valuing cash balances. We then moved on to cross holdings, and why they are difficult to incorporate into value, and to other assets that you may consider adding on, because we have not considering them yet. On the latter, the key component to remember is not to double count an asset, by first counting its cash flow and then the value of the asset itself. Finally, I attach a weekly challenge for this week, built around terminal value. Please try it when you get a chance. It is simple but it will reinforce some key components of what we did in class. Next week is spring break, and I hope that you have fun, and I promise not to send you emails for seven days, starting this Saturday. Attachments: Post class test and solution, Weekly challenge |

| 3/10/22 | I know that you are looking forward the the break, and I wish you the best. That said, I hope that you are also moving forward on your project. As I mentioned at the start of the class, I will be glad to give you feedback (without a grade) on the intrinsic (DCF) value for your company, if you can get your DCF spreadsheet to me by April 1. While I will not be able to tell you whether your valuation is right or wrong, I can at least tell you whether there are inconsistencies. If you are just starting, I thought I would give you a boost. First, I will not be giving any credit for excel spreadsheet building skills. In fact, I would rather than you focus on valuation and less on spreadsheet building. If you are valuing a non financial service company, the only spreadsheet you will nee is the following;

The spreadsheet comes with add-ons that you may or may not need. Thus, there is a lease conversion worksheet, but if your company follows IFRS or GAAP can capitalizes leases, you can turn it off. There is an option worksheet that converts employee options into a value and recomputes value per share. Use what you want, turn off whatever you do not. To help you in using the spreadsheet, you may want to use this video guide that I recorded this morning for the Motley Fool, on how to use that spreadsheet.

The presentation is long (about 2 hours) but the first hour is a quick review of the class, and if you have lost perspective as we delve into the details of discount rates, cash flows and growth, it is worth watching. The second hour takes you through the spreadsheet, using the Tesla November 2021 valuation as the exhibit, on how to estimate key inputs and how to read the output. If you really, really want to build your own spreadsheet, you can do so, but remember my admonition about less is more and please do not (under any conditions) use a spreadsheet you picked up at an investment bank, since fundamental flaws are baked into it. Until next time! |

| 3/18/22 | f you are back from break, welcome back! If not, enjoy the weekend and hope to see you back on Monday. That said, my week of not sending emails is now officially over, and in case you have the time, I hope that you are starting work or are continuing to work on your company valuation (which is due for informal feedback on Friday, April 1). As you well know, or will find out soon enough, much of your value per share for your company will come from the terminal value, and I have a webcast on checking terminal value that I hope that you get a chance to look at.

I have built these checks into the spreadsheet that I sent you just before break ( https://www.stern.nyu.edu/~adamodar/pc/fcffsimpleginzu.xlsx), though I also let you change the defaults and get yourself into trouble. I also sent you a link to a YouTube video of a session I did for Motley Fool analysts on how to use the spreadsheet, and just in case you have lost that link, here it is:

|

| 3/19/22 | he newsletter for this week is attached. In case you have time on your hands, I also just posted my thoughts on the market/economic implications of the war in the Ukraine.

It may seem callous to talk about markets, when people are dying, but I don’t have a solution to the war (though I wish I did), and I am sure that you are not interested in what I think on humanitarian grounds.

Attachment: Issue 6 (March 19) |

| 3/20/22 | The break is definitely over and I hope to see you back in class this week. We will complete our discussion of loose ends tomorrow, by talking about to deal with complexity, debt and stock compensation tomorrow. We will then turn to how story telling is at the heart of valuation, and how to connect stories to numbers. If you want to get a jump on this discussion, without spending the $20 it would cost you to buy the book, please read this post that I wrote on story telling and valuation in 2014:

The book was born out of this post, and the slides you will see in class came from it as well. It was a good return on time invested, for me, and I hope that you enjoy it too. |

| 3/21/22 | During today's session we finished the last loose ends in valuation and started on connecting stories to numbers. The way in which companies and equity research analysts treat stock based compensation is criminally negligent and I hope that you fin this post on the topic useful:

If you want a longer version of my stories to numbers session, you may prefer this Google talk version that I did a few years ago on the same topic:

It is longer and a little more detail.

The DCF is due by a week from this Friday (April 1) (try to get it in by 5 pm, but if not, 6 pm or 7pm..). If you can get it in earlier, all the better. A few notes on the submission:

1. Individual, not group: This portion of the submission can be done individually and should be done individually rather than as a group, The feedback is specifically for you. As I mentioned in my emails from last week, you are welcome to use the spreadsheet that I have already built (or adapt it to your needs, so that you are not starting from scratch).The most versatile one for non-financial service firms is:

2. Submission content: An Excel spreadsheet will do, with notes embedded on your story and any specific assumptions

3. Submission subject: Use “My Perfect DCF” in your subject. (Please don’t deviate from the script. It is to make sure that it gets into the right smart mailbox, and computers have no sense of humor)

Remember that this DCF is for feedback, not a grade, but work on it as if were your final valuation. That way, the feedback will be more focused and perhaps more useful.

To put a bow on this part of the class, I have a blog post that you may find enjoyable about dysfunctional DCFs.

I hope that none of your DCFs fall on this list.

|

| 3/22/22 | In this week’s valuation of the week, I look back at a valuation I did fouryears ago, when Brexit was still up in the air in the UK and people were unsure about how it would play our, with as many as seven different options on Brexit, ranging from a No-deal Brexit to no Brexit at all. I tookeasyJet, a UK company that is particularly exposed to Brexit, because it gets so much of its revenues from the EU, which has stringent rules on who can or cannot fly between EU countries, and tried to value it under different scenarios. You can read my valuation thesis here:

If nothing else, you will see how scenarios can be used to deal with uncertainty. The valuations themselves are at the links below:

Brexit may now be settled, and you may not care about easyJet, but review the write up and valuation anyway, since this approach may help you in valuing your company, especially if you feel that there are discrete risks (an election coming up, a potential nationalization, regulatory change) that your firm is exposed to, where value can vary depending on the outcome.

|

| 3/23/22 | In today’s class, we continued our discussion of stories, and how critical it is to keep the feedback loop open, so that you can make your stories better. We also talked about how story breaks, shifts and changes. Since I talked about dealing with new earnings reports, I thought you may find these two posts of interest in how narratives shift, and with them, values:

Reacting to Earnings Reports: http://aswathdamodaran.blogspot.com/2014/08/reacting-to-earnings-reports-lets-get.html Narrative Resets: http://aswathdamodaran.blogspot.com/2015/08/narrative-resets-revisiting-tech-trio.html We started with a conventional valuation of Con Ed in class, but we will move to more interesting storylines and valuations next class. If you are still wrestling with the question of management options, I have a weekly challenge that may help you work through your doubts: Of course, the stories on these companies has evolved since, but it should give you a taste of how narratives change.

|

| 3/24/22 | I know that your project DCFs are not due until a week from tomorrow, but if you decide to work on your DCF and even turn it in early, here is some general guidance.

Don’t put too much pressure on yourself. This is only for feedback. Try your best. One final note. I will have office hours specifically for the project tomorrow (Friday, March 25) from 11 am-12 pm. The zoom link for the office hour is below:

|

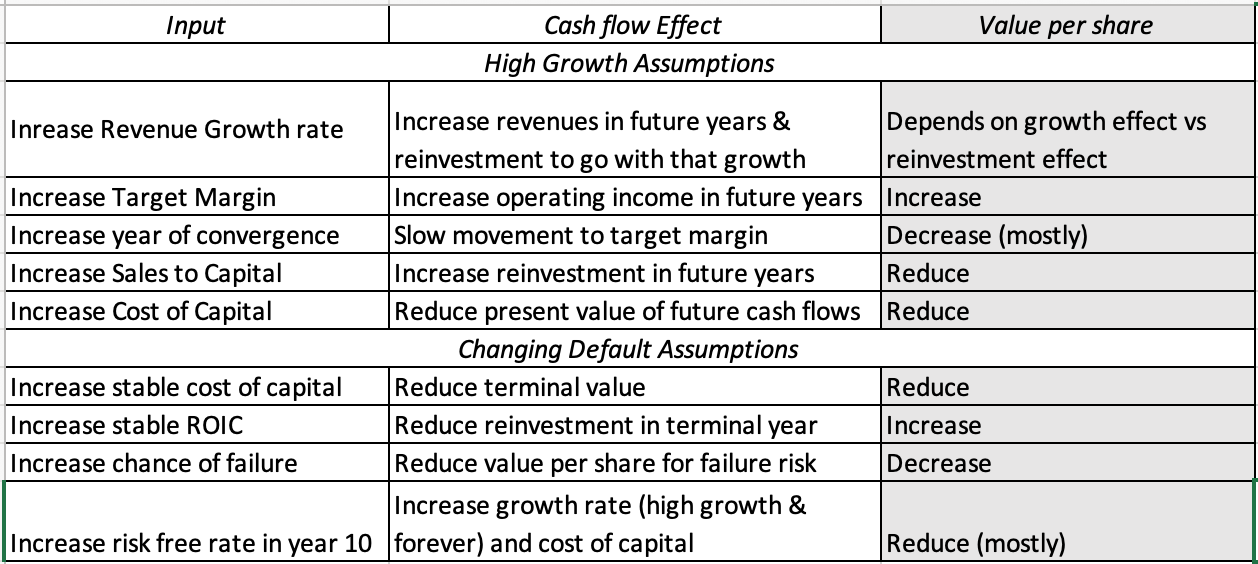

| 3/25/22 | I hope that you are able to spend some time this weekend working on your valuations, and they are due next Friday (April 1, and not the week after). As you work through them, there will be occasions where you will get a value that is very different from the price, and you will be inclined to believe that you (a) must have done something wrong or (b) that my spreadsheet has done something to screw up your valuation. While the latter will make you feel better, the truth is that the spreadsheet is designed to faithfully convert your inputs into a valuation. Thus, if you are getting too low a value, it is coming from your inputs on growth rates, margins and reinvestment (through your sales to capital ratio for the next ten years and the ROIC after year 10). Changing those inputs will change your value, but if your end game becomes getting the value closer to the price, you have to ask yourself what the point of doing valuation is, in the first place. There is a diagnostic worksheet built into the spreadsheet that points to your big assumptions and how they connect to your valuation. Use it, if you are concerned about your value. Here is a simple table that illustrates how your assumption in the spreadsheet change value:

Put simply, this table illustrates what happens to your value per share, when you change these inputs in your valuation. Some of the effects are obvious; higher target operating margins will always increase value and higher costs of capital will reduce value. Some are tricky. If your value looks low, and you increase the revenue growth rate, it will mostly increase value, but it can sometimes lead to lower value, if you have a low sales to capital ratio (and higher revenues cause reinvestment to increase). The default assumptions at the bottom can also affect your value per share, and if misused, can cause your valuations to blow. In particular, be very, very careful with the default assumption where I let you set a growth rate that is different from the risk free rate in perpetuity. If you over ride that default and set the growth rate well above the risk free rate, I will have to disavow any responsibility for what may happen to your value.

On a different note, if you are confused about employee options and how they affect value, you may also want to watch this webcast that I put together on doing this in practice. I used Cisco, a monster option granter, to illustrate the mechanics. You can find the links below:

Webcast: https://youtu.be/-sGw4oLPTsM

Cisco 10K: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/EmployeeOptions/cisco10K.pdf

Spreadsheet for options: https://www.stern.nyu.edu/~adamodar/pdfiles/eqnotes/webcasts/EmployeeOptions/ciscooptions.xls

I hope you get a chance to watch the webcast and that you find it useful. |

| 3/26/22 | I hope that you are approaching cloture on your DCF valuation. In case you are interested, the newsletter for this week is attached. Attached: Issue 7 (March 26) |

| 3/27/22 | As you work your way through your valuations, a quick preview of what is coming this week. We will spend both tomorrow and Wednesday’s class working through valuations. While we will spend only a few minutes on each company’s valuation, I will focus on one or two aspects in each company to highlight. (Otherwise, going through every valuation in full detail will be drudgery.) If you do get done with your valuation before then, you don’t have to wait until Friday. Go ahead and send it to me, when you are ready, using “My Perfect DCF” as your subject. |

| 3/28/22 | In today’s class, we started by looking at 3M, and how a market crisis can affect value, even if nothing about the company has changed. We then adapted the model to value an index (the S&P 500). If you are interested in an updated version, where you can change the numbers try this link:

Finally, we looked at how best to adapt valuation models to value companies on the dark side. Specifically, we examined how best to value young companies with limited information. If you are interested, try this paper on valuing young companies:

I also have a blog post that you may find relevant for today’s discussion on how dilution in future years is already incorporated into value:

I have noticed that some of you are having trouble with the zoom link for office hours. Since it is shared with the other two classes, it might not be showing up on Brightspace, but the link is below (for both today, from 5 pm - 6 pm) and all subsequent office hours):

Next Monday, we will move on to the second quiz for the class. In case you are nervous about it, here are some specifics:

1. Quiz time and logistics: The quiz will be on Monday, April 4, in the first 30 minutes of class (1.30-2 pm) and there will be class after the quiz.

2. Content: It will cover the mechanics of DCF, starting with growth rates and terminal value and extended into the loose ends of valuation and the versions of the DCF we have used on the dark side.

3. Review for the quiz: The links to the review for the quiz and the past quizzes are below:

Presentation: https://pages.stern.nyu.edu/adamodar/pdfiles/eqnotes/valquiz2review.pdf

Webcast: http://www.stern.nyu.edu/~adamodar/podcasts/Webcasts/valquiz2review.mp4 You can also find all past quizzes with the solutions in the following links: All past quiz 2s: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/quiz2.pdf Quiz 2 solutions: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/quiz2sol.xlsx |

| 3/30/22 | In today’s session, we continued on the dark side of valuation with a look at mature companies on the verge of transitions, and how you have to value the status quo company and the restructured one to make a judgment on investing in it. Finally, we looked at declining companies, where your forecasts may have to show declining revenues and margins, and added a twist with distressed companies, where you have to follow up your DCF. |

| 3/31/22 | I hope that you have had a good week. I know that some of you have turned your attention to the quiz, which is on Monday, and that is perfectly understandable. In case, you have lost the links to quiz, I have attached them below:

Presentation: https://pages.stern.nyu.edu/adamodar/pdfiles/eqnotes/valquiz2review.pdf

Webcast: http://www.stern.nyu.edu/~adamodar/podcasts/Webcasts/valquiz2review.mp4 You can also find all past quizzes with the solutions in the following links: All past quiz 2s: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/quiz2.pdf Quiz 2 solutions: http://www.stern.nyu.edu/~adamodar/pdfiles/eqexams/quiz2sol.xlsx I had also promised office hours this weekend. They will be from 11 am - 12 pm on Sunday, and the zoom link is below. If there are lots of people, I will stay on as long as needed to answer your questions:

For those of you who still have the time to work on your DCF, if you can get me your DCF to me tomorrow, great, but I will leave the submit window open for a week, for feedback, but only if you want it. When you do submit it, a reminder to enter “My Perfect DCF” in the subject. |

| 4/2/22 | Three quick notes. First, the newsletter for the week is attached. Next, if you are preparing for the quiz, I will have office hours tomorrow and day after and the links are below:

Office hour on Sunday, April 3, from 11 am - 12 pm: https://nyu.zoom.us/j/91979690185

Office hour on Monday, April 4, from 9 am - 10 am: https://nyu.zoom.us/j/92119670806

Finally, we will be done with packet 1 this coming week and moving on to packet 2. Please download both packets 2 & 3 when you get a chance. The links are on the webcast page, but I have the attached the pdf links below:

Atachments: Issue 8 (April 2) |

| 4/2/22 | By now, almost all of you should have got your DCFs back, with my minimalist feedback. If you have not received feedback, could you please resend your DCF with “My Perfect DCF” in the subject. If you were expecting feedback on details (like beta or revenue growth rates), you were probably disappointed, but I thought that it might make sense to take you through my template for reviewing my spreadsheet, so that you can do it yourself on a future valuation.

1. Start by looking at your historical financials: The first place to start is by checking the inputs that you have for the most recent year and the year before. I took two company valuations from last year’s class (so that I would not be exposing the valuations of someone in this class), Live Nation and Nio, very different companies and will use them to illustrate the process.

Obviously, Live Nation and Nio diverged in 2020, with the former having a horrifically bad year and the latter a really good one (at least in terms of growth). Note that Nio is incorporated in the US, but it is a Chinese company.

Advice on units: Everything in your valuation has to be in the same units (hundreds, thousands, millions etc.). While you can use any units, stay away from having too many digits in your inputs (pick millions over thousands, for instance).

2. Check out the riskfree rate and cost of capital: The riskfree rate will reflect your currency choice for your valuation and your cost of capital will (or should be) in the same currency. I do have a worksheet that computes your cost of capital, but if you plan to use, rather than directly input a cost of capital, please make sure that you have picked the businesses and geographies for your company in that sheet.

Live Nation

Nio

Live Nation is being valued in US dollars, while Nio is being valued in Yuan. (See riskfree rates). The costs of capital are consistent, lower for Live Nation than for Nio. To check to see if your cost of capital is within bounds of reasonableness, remember that the median cost of capital in US dollar terms for a global company is 6-6.5%, and if you have a different currency, you can add inflation to it. If your cost of capital is more than 4% off the median in either direction, check your numbers to see if there is a mistake.

3. Check through the key inputs on growth, margins and reinvestment: The key inputs that drive your valuation are in the input sheet, and while they might be linked to a cell in default, you preserve and should use the power to change them to what you think best fits your story (see step 5):

Live Nation

Nio

You may need to revisit your numbers after you go through step 4, but you are not bound by historical data, industry averages or any other variable. These are your inputs.

4. Do a quick scan of the valuation output: Go to the valuation output page, and check out the following:

a. Revenues in your terminal year: One of the problems with growth rates in percent is that it is very difficult to figure out how the compounding plays out over time. To illustrate, take a look at the revenue forecasts for Live Nation over time:

The growth rates look high, but the revenue you have in year 10 is $8.5 billion, well below the revenues of $11.5 billion they had in 2019. That is a pessimistic story, albeit a plausible one, for the future, and if that is what you intended, you should leave it as is. If not, you should go back and change your revenue growth rate from years 2-5.

For Nio, revenues are up, up and away, which makes sense given that it represents the convergence of two potentially big markets (China and electric cars)

Here the revenues increase to 340 billion Yuan in year 10. (In dollar terms, this would be about $50 billion). Again if that strikes you as too low (high) a number, go back and revisit your revenue growth rate. To get a sense of whether it is too high or too low, you should look at large companies in the sector and see what they generate as revenues.

b. Evolution of margins/operating income over time: In the table above, you also see margins changing for your two companies towards your target margin. How quickly it happens depends on the year of convergence that you pick. A lower number (as is the case with Live Nation) will cause a speedier convergence.

c. Imputed return on capital: If you go to the bottom of the valuation spreadsheet, you will notice an item that you probably overlooked when you did your valuation, but it will give you a snapshot of how your assumptions about growth, margins and reinvestment have played out in the company. For Live Nation, here is what you see:

The fact that your return on capital has trouble getting off the floor and even approach your cost of capital is troublesome, and it does look like you are reinvesting way too much, but more on that in step 5.

With Nio, the return on capital rises rapidly over time, but given its status as a first mover in China and presumed competitive advantages in that market, you may be okay with the 24.85%, but if you feel it is too high, you may need to work on your reinvestment, by lowering your sales to capital ratio.

5. Go to your stories to numbers worksheet: The most critical sheet on diagnosing your own DCF is your stories to numbers sheet. If you never even got to this sheet, clearly, you would not have been able to use it, since it will carry the default stories for GameStop or Boeing in there. For Live Nation, here is what you will see:

As you can see, the valuation yields a negative value per share and the culprit is also clear. It is your negative FCFF for the next 8 years. While each individual item has a storyline that makes sense, there is a fundamental contradiction in these forecasts. Since you are assuming that the company will not even make it back to 2019 levels, why do you need to be reinvesting such huge amounts in the future. Put simply, the sales to capital ratio is way too high, given your revenue story, and the easiest way to fix it is to go raise the sales to capital ratio to a really high number (I would use 100, in this case, since your revenues never make it back to pre-COVID levels). In more moderate cases, where you make it back to pre-COVID levels over the next three or four years, you can use a high sales to capital ratio for those three years and then lower it to historic norms or industry averages.

Finally, I know that a few of you built your own spreadsheets and I applaud you for doing so. If you found yourself pushed into using my spreadsheet, it is not because I am better at building spreadsheets than you are. I am not an Excel ninja, but I do know that spreadsheet building is a lot more work than you initially think it will be. In my experience, any spreadsheet you build takes about ten runs before you fix any remaining errors, and I wanted your focus to be on valuation, not Excel. So, feel free to abandon my spreadsheet and build your own, when you have the time. If you do so, my only advice to you is to forget everything you learned about building spreadsheets at an investment bank, where you have hundreds of line items, three statement forecasts and exit multiples. That is the roadway to hell.

|

| 4/3/22 | Needless to say, but I will say it anyway, the second quiz is tomorrow in class, in the first 30 minutes of class. If you signed up to take it virtually, you will be getting instructions in the next few minutes on access, but the window for the online version is now closed, since it creates chaos to be adding people at the last moment. Tomorrow, we will complete the residue of intrinsic valuation, by talking about valuing emerging market, commodity and financial service companies. On Wednesday, we will start on pricing, and that will require the second packet of lecture notes which are accessible on the webcast page for the class. Please download them when you get a chance. See you tomorrow, and until next time! |

| 4/4/22 | In today’s session, after the second quiz, we wrapped up our discussion of intrinsic valuation. For decades, we have valued banks using the dividend discount model, simply because getting cash flows is so difficult, but that approach is built on trusting management at banks to behave sensibly (paying out what they can afford to in dividends) and regulators to do the same. For me, that trust was breached in 2008, and I present a way of estimating FCFE for a bank, using investment in regulatory capital as my stand in for reinvestment. Next session, we will wrap up the valuation section and start on pricing. If you are interested in reading more about valuing financial service companies, try this link:

The Deutsche Bank post is here: