|

|||

|

|||

I confess. I send out a lot of emails and I am sure that you don't read some of them. Since they sometimes contain important information as well as clues to my thinking (deranged though it might be), I will try to put all of the emails into this file. They are in chronological order, starting with the earliest one. They are in chronological order, starting with the earliest one. So, scroll down to your desired email and read on, or if the scrolling will take you too long, click on the link below to go the emails, by month.

| Date | Email content |

||||||||||||||||||

| 1/13/25 | Happy new year!. This is the first of many, many emails that you will get for me. You can view that either as a promise or a threat. I am delighted that you have decided to take the corporate finance class this spring with me and especially so if you are not a finance major and have never worked in finance. I am an evangelist when it comes to the centrality of corporate finance and I will try very hard to convert you to my faith. I also know that some of you may be worried about the class and the tool set that you will bring to it. I cannot alleviate all your fears now, but here are a few things that you can do to get an early jump:

1. Pre-work for class

As things stand now, and this could quickly change, we will meet in Paulson Auditorium, a cavernous amphitheater with all of the charm of Madison Square Garden on a bad day (which would be any day that the Knicks actually play there) every Monday and Wednesday, starting on January 27, going through May 5, from 10.30 am to 11.50 am. I will not take attendance, but I would really, really, really like to see you in class. If you do miss a class, the sessions will be recorded and will be available in three places:

You can find out all you need to know about the class (for the moment) by going to the web page for the class:

http://www.stern.nyu.edu/~adamodar/New_Home_Page/corpfin.htmlThis page has everything connected to the class, including webcast links, lecture notes and project links. The syllabus has been updated: https://pages.stern.nyu.edu/~adamodar/pdfiles/cfovhds/cfsyllspr25.pdfIf you click on the calendar link, you will be taken to a Google calendar of everything related to this class. You will note references to a project which will be consuming your lives for the next four months. This project will essentially require you to do a full corporate financial analysis of a company. While there is nothing you need to do at the moment for the project, you can start thinking about a company you would like to analyze and a group that you want to be part of.

3. Class Material

Now for the material for the class. The lecture notes for the class are available as a pdf file that you can download and print. I have both a standard version (one slide per page) and an environmentally friendly version (two slides per page) to download. You can also save paper entirely and download the file to your iPad or Kindle. The first packed can be found at the link below:

It is a big file and will take while to download. Have patience

There is a book for the class, Applied Corporate Finance, but please make sure that you get the fourth edition. It is exorbitantly over priced but you can buy, rent or download it at Amazon.com or the NYU bookstore

While I have no qualms about wasting your money, I know that some of you are budget constrained (a nice way of saying "poor") . If you really, really cannot afford the book, you should be able to live without it.

4. Final Thoughts

I know that In the last decade, we have been forced to reexamine accepted wisdom in pretty much aspect of life, and corporate finance is no exception. As we struggle with the new and the different, we have to incorporate the lessons learned, unlearned and relearned over this period into corporate finance, and I will tru. There are assumptions that we have made for decades that need to be challenged and foundations that have to be reinforced. In other words, the time for cookbook and me-too finance (which is what too many firms, investment banks and consultants have indulged in) is over. At the same time, there is a whole lot nonsense that has been bandied about as the “new way to run business” and I will not mince any words (or spare any feelings) in talking about them. To close, I will leave you with a YouTube video that introduces you (in about 2 minutes) to the class.

I hope you enjoy it. That is about it. I am looking forward to this class. It has always been my favorite class to teach (even more so than valuation, my other teaching venture) and I have a singular objective. I would like to make it the best class you have ever taken, period. I know that this is going to be tough to pull off but I will really try. I hope to see you on January 27th, in class. Until next time!

|

||||||||||||||||||

| 1/20/25 | I hope that you have had a good week since my last email, and if your response is what last email, you may want to check this link:

Next week, at the first class, I will spend time laying out what the class is about, what I hope that we will accomplish during the semester, as well as establish the key themes that underlie corporate finance. You can download the syllabus ahead of time:

As you read the syllabus, you will notice mention of a project and in case you are curious, here is the link to the project resources:

Once we are through the syllabus in the first session, we will turn our attention to the lecture note packets, and every slide you see in class after this will be in that packet. The lecture notes are in two parts, and the first part can be obtained at this link (which I sent you last week as well):

It is also available in powerpoint form (though the file size is bloated), if you go to the lecture note page or webcast page of the class. (Again, if you have trouble getting these links to download, try a different browser)

Now that I have drowned you in stuff, just a little aside. I don’t much care for academic research and almost everything that I write is for practitioners, and my blog (sounds new age, doesn’t it?) has become the first repository for my writing. I spend the first few weeks of each year, talking about the data that I update on my website:

The first two updates re on my blog. Please browse through them, because they are relevant for class:

I will see you in class next week (Monday. January 27, at 10.30 am, NY time on in Paulson Auditorium. I would obviously love to see you in person in class, but if for any reason, you are unable to make it to class, it will be carried as a live zoom session, and the zoom link for all of the sessions is below:

The sessions will also be available in recorded form. Until next time! |

||||||||||||||||||

| 1/26/25 | As we finish up the last weekend before class, I am sending this as a last pre-class email. When I start class tomorrow, it will be my 41st year teaching and I am thankful that I still look forward to the day. There is no other profession where you can start with a clean slate every few months, even though you may screw it up in the subsequent days and weeks. We will meet in Paulson from 10.30 am - 11.50 am for our first class, and it will be glorious (I have got to hype it up as much as I can). I would love to see you all in class, but I do realize that some of you will not be able to make it in class for a variety of reasons, and worry not, since the class will be carried live on Zoom. The zoom link for the class is below:

The recorded versions of the session will also be accessible at the webcast page for the class (see link below).

This page also has the links to the lecture notes and other material for the class.

During the first class, it would have been standard practice for me to hand out the syllabus and project description, but I think that if we truly live in a digital world, it is time to phase out this practice. So, please download the two packets and bring either a digital or physical copy to class tomorrow.

Project Description: https://pages.stern.nyu.edu/~adamodar/pdfiles/cfovhds/cfproj.pdf

At the risk of repeating myself, the lecture note packets for the class are also ready and you can find the links at the top of the webpage for the class sessions:

I am a believer in data, respecting (but not revering) it, and every year, I play Moneyball, with public data. (If you have not watched the movie yet, that is your assignment for tonight). If you are interested in my data updates, you may want to start by reading my first three data posts for 2025:

Until next time!

|

||||||||||||||||||

| 1/27/25 | I promised you with a ton of emails and I always deliver on my promises... Here is the first of many, many missives that you will receive for me….. First, a quick review of what we did in today's class. I laid out the structure for the class and an agenda of what I hope to accomplish during the next 15 weeks. In addition to describing the logistical details, I presented my view that corporate finance is the ultimate big picture class because everything falls under its purview. The “big picture” of corporate finance covers the three basic decisions that every business has to make: how to allocate scarce funds across competing uses (the investment decision), how to raise funds to finance these investments (the financing decision) and how much cash to take out of the business (the dividend decision). The singular objective in corporate finance is to maximize the value of the business to its owners. This big picture was then used to emphasize five themes: that corporate finance is common sense, that it is focused, that the focus shifts over the life cycle and that you cannot break first principles with immunity.

On to housekeeping details.

That is about it, for this email. |

||||||||||||||||||

| 1/28/25 | In the first puzzle for this semester, I am going to focus on the objective in corporate finance, In class, I said that the end game is to maximize the value of the business and that objective has given corporate finance its focus, but has also given rise to criticism that it comes at the expense of other claimholders. That is a legitimate point, and even the Business Roundtable seemed to come around to a stakeholder point of view in this missive:

In a post shortly thereafter, I took issue with the Business Roundtable, and argued that it was the wrong message and that the messenger, Jamie Dimon, was singularly ill equipped to talk about shareholder interests, given how cavalierly he has ignored them over his tenure.

I know that many of you will disagree with me on my conclusions, but I think that this will be a great start for tomorrow’s class. So, please read both and try to answer these questions:

Since this is the type of discussion that is enriched by everyone joining, I have created a forum on the topic under Brightspace, for this class. Log in, check under content, and then under weekly puzzles and you should see the forum. You can post your thoughts, any interesting links or dissenting points of view there. |

||||||||||||||||||

| 1/29/25 | In today's class, we started on what the objective in running a business should be. While corporate finance states it to be maximizing firm value, it is often practiced as maximizing stock price. To make the world safe for stock price maximization, we do have to make key assumptions: that managers act in the best interests of stockholders, that lenders are fully protected, that information flows to rational investors and that there are no social costs. We started on why one of these assumptions, that stockholders have power over managers, fails and we will continue ripping the Utopian world apart next class.

1. Other People's Money: Just a few added notes relating to the class that I want to bring to your attention. The first is the movie Other People's Money, which is one of my favorites for illustrating the straw men that people like to set up and knock down. You can find out more about the movie here:

But I found the best part on YouTube. It is Danny DeVito's "Larry the Liquidator" speech:

Watch it when you get a chance. Not only is it entertaining but it is a learning experience (though I am not sure what you learn). Incidentally, it is much, much better than Michael Douglas's "Greed is good" speech in the first "Wall Street " which was a blatant rip-off of Ivan Boesky's graduation address to the UC Berkeley MBAs in 1986 (which I happened to be at, since I was teaching there that year).

2. DisneyWar: In next week’s session, I will be talking about the dysfunctional state of Disney in the 1990s. If you want to review these on your own, try this book written by James Stewart. It is in paperback, on Amazon:

If you want a more contemporary version of how Disney’s corporate governance is playing out, and want an insider’s perspective, Bob Iger’s autobiography is a solid bet:

3. Company Choice: On the question of picking companies for your group, some (unsolicited) advice:

As a final reminder. Please pick your company soon... As you can see from today's class, we are getting started on assessing your company…

4. If you want to download the financial statements for your company, I would recommend that you start with the annual report for the most recent year. You should be able to pull it off the website for the company, under investor relations. If you want to keep going, and it is a US company, go to o the SEC site (https://www.sec.gov/edgar). If it is a non-US company, you will have to find the equivalent regulatory body in your country. For some of your companies, you will find less data than on others. Don’t fret. It is what it is. Finally, I am attaching the post class test and solution for today’s session.

|

||||||||||||||||||

| 1/30/25 | t is never too early to start nagging you about the project. So, let me get started with a checklist (which is short for this week but will get longer each week. Here is the list of things that would be nice to get behind you:

In doing all of this, you will need data and Stern subscribes to one of the two industry standards: S&P Capital IQ (the other is Factset). It is truly a remarkable dataset with hundreds of items on tens of thousands of public companies listed globally, including corporate governance measures. To get access to Capital IQ, you need to ask for it, and the attached document leads you through the process. As with all things IT related, I am sure that there are glitches and if you find them, let me know.

This is the seventh or eighth email for the class. If you have not been receiving these emails (which means that you are reading this in the chronicles), it is worth noting that I don’t keep an email list for the class. I use the Google groups that Stern creates. In theory, students registered for the class should be on Albert (the NYU official registration/grading site), Brightspace and Google Groups, and the three should be synced, but this is a university. What should be true in theory is not always the case in practice. I can do very little to alter the Google groups. If you are finding yourself locked out of the email list, start with IT, and if they won’t help, I will figure out a way to add you in. If you are a non-Stern student, and have an email address that does not end in@stern.nyu.edu, note that you were assigned a stern email address when you joined this class, and you should be able to find that address. Here is what I got from IT when I asked:

Since you are teaching a Stern course, all your students, exchange and non-Stern, are provided with a Stern account and Gmail.

You can have them all head over to 'start.stern.nyu.edu' to activate their account.

I think I have exhausted my welcome, Until next time! Attachment: Capital IQ Access |

||||||||||||||||||

| 1/31/25 | First things first. As I noted yesterday, the DeepSeek story is a corporate finance, and one with the potential to alter the end game for an entire business (AI), with ripple effects for all of us. With the lead-in that I am an AI novice, and that I have far more insight into potato chips (salt and vinegar beats BBQ, and waffle style is the best) than silicon chips, I decided to put my thoughts down on paper (and it kept going and going). Here is the post that just went up five minutes ago:

There is no rocket science here, nor advanced finance, but I would love to get your thought.

Also, as promised, here is the first of the weekly in-practice webcasts. These are 10-15 minute webcasts designed to work on practical issues in corporate finance. This week’s issue is a timely one, if you are working on picking companies for your project (as you should be..). It is about the process of collecting data for companies, the first step in understanding and analyzing them. The webcast link is below:

It is a little dated (but I have been too lazy to update it), but I don’t think it is too painful to watch, and you may even find it useful. I have also put the link up on the webcast page for the class:

The webcasts for the first two classes should be on there, if you missed (physically, metaphysically or mentally) and the links to the project and syllabus that I handed out in the class. You can stream or YouTube the sessions, or download videos/audios. Also, if you joined the class late, you can get all emails sent up till today here:

Finally, have you had a chance to look at the weekly puzzle? If not, give it a shot by going here:

At the risk of nagging, please do get the lecture note packet 1 downloaded before Monday’s class. It is accessible on the webcasts page linked above. |

||||||||||||||||||

| 2/1/25 | As you start the weekend, I decided to butt in with the first of my newsletters. As you browse through it (and I hope you do), you will realize that this is not really news or even fake news. It is more akin to a GPS for the class telling you where we’ve been and where we plan to go. It is a good way to get a sense of whether you are falling behind on either the class or the project, especially as we get deeper into the class. On a different note, it looks like your groups and jelling and I will be playing matchmaker to get the rest of you in groups. So, the next step is to go into the class master list and enter the name of the company that you will be analyzing as soon as you have picked one:

https://docs.google.com/spreadsheets/d/1xsASDBhkGo_1WhivAMLMkhi_z6cyYFnv1Q9G4y2TN4I/edit?gid=0#gid=0

Enjoy your weekend and I will see you on Monday!

Attachment: Issue 1 (February 1) |

||||||||||||||||||

| 2/2/25 | No email | ||||||||||||||||||

| 2/3/25 | In today’s session, we spent almost a large chunk of out time on the assessment of where the power lies in a company. In the utopian world, the power lies entirely with shareholders, but in the real world, that is not often the case. It can lie with managers, if shareholdings are diffuse and shareholders are passive. It can lie with a subset of inside shareholders, who have large holdings and/or are part of incumbent management. In some cases, that power can come from having voting and non-voting shares. It can lie with governments, lenders or employees. The first step in understanding why a company does what it does is to assess the power structure, and I suggested that you look at the largest shareholders in the company. One source for this is Bloomberg, and while almost all of the information you will find on it can be found elsewhere, it does provide a convenient place to get information. The first step is finding a Bloomberg Terminal, and there are three on the fourth floor of KMEC, in the MBA Study Room. I have never used them, but reliable sources have told me that that the usernames and passwords are in the computer wallpers (they are BBREADING1, 2 or 3 and then a password that is Alpha, Delta or Gamma followed by numbers). Once you are able to get on the terminal, type in the name of your company and a bunch of listings on your company will show up. It may take a little trial and error, but you should eventually find your local listing of your stock. If you can get on a Bloomberg terminal, try this:

1. Press the EQUITY button

2. Choose FIND YOUR SECURITY

3. Type the name of your company

4. You might get multiple listings for your company, especially if it is a large company with multiple listings and securities. Try to find your local listing. For a US company, this will usually be the one with your stock symbol followed by US. For a non-US company, it will have the exchange symbol for your country (GR: Germany, FP: France, LN: UK etc...) It may take some trial and error to find the listing....

5. Type in HDS

6. Print off the first page of the HDS (it should have the top 17 investors in your company).

If you cannot get to a Bloomberg, much of that same information is available on Yahoo! Finance and other online financial data providers. Here is the Yahoo! Finance page for NVDA.

Check out the percent of shares held by insiders (includes founders, managers and individuals owning more than 5%) and by institutions. Then, check out the biggest players. You can see the growth of passive investing in the top two on this (and probably every other large cap company in the universe) - Vanguard and Blackrock, both of which have index funds that track the S&P 500. |

||||||||||||||||||

| 2/4/25 | In this week’s puzzle, I thought I would use the recent kerfuffle at the Adani Group to talk about corporate governance in family group companies., You can find the puzzle described here:

That puzzle points you towards two posts from my blog. In the first post, I wrote a long time ago, where trouble was brewing at the Tata Group, the family group controlling Tata Motors:

I note the pluses and minuses for shareholders from investing in family group companies. I then turn to my last year's post on the Adani Grop, a first-generation family group company founded by Gautam Adani. It is heavily focused on infrastructure business, is connected strongly to political power in India and has seen its market cap zoom over the last two years in particular. In the post, I look at the Adani Group's growth over time, and examine how it has become the focus of a US-based short seller in Hindenburg, which contends that the group has indulged in earnings and price manipulation, and that institutions have looked away.

In the post, I also look at the ownership structure for the Adani Group and note that not only does the group control 73% of the shares outstanding in the company, but that statistic has barely budged over the last decade, even as the company has grown massively. There is a valuation in the post, but I would like your focus to stay on corporate governance at Adani specifically and at family group companies, in general. The puzzle ends with five questions:

In terms of mechanics, how does a family keep its ownership stake intact as a company is growing?

Give it a shot and you don’t need a finance background or have anything to do with India to do it. It is all about power.

|

||||||||||||||||||

| 2/5/25 | The objective function matters, and there are no perfect objectives. That is the message of the last two classes. Once you have absorbed that, I am willing to accept the fact that you still don't quite buy into the "maximize value" objective. That is fine and I would like you to keep thinking about a better alternative with three caveats. First, you cannot cop out and give me multiple objectives - I too would like to maximize stockholder wealth, maximize customer satisfaction, maximize social welfare and employee benefits at the same time but it is just not doable. Second, your objective function has to be measurable. In other words, if you define your objective as maximizing the social good, how would you measure social good? Third, take your objective (and the measurement device you have developed) and ask yourself a cynical question: How might managers game this system for maximum benefit, while hurting you as an owner? In the long term, you may almost guarantee that this will happen.

Building on the theme of social good and stockholder wealth a little more, there are a number of fascinating moral and ethical issues that arise when you are the manager in a publicly traded firm. Is your first duty to society (to which we all belong) or to the stockholders (who are your ultimate employers)? If you have to pick between the two and you choose the former, do you have an obligation to be honest and let the latter know? What if you believed that the market was overvaluing your stock? Should you sit back and let it happen, since it is good for your stockholders, or should you try to talk the stock price down? On the question of socially responsibility, there are groups out there that rank companies based upon social responsibility. I have listed a few below, but they are a few of many:

JUST Capital: https://justcapital.com/rankings/

Calvert Social Index: https://www.calvert.com/calvert-indexes.php

Dow Jones Sustainability Index: https://www.spglobal.com/spdji/en/indices/esg/sp-500-sustainability-screened-index/#overview

And this is just the tip of the iceberg. Environmental organizations, labor unions and other groups all have their own corporate rankings. In other words, whatever your key social issue is, there is a way to stay true (as a consumer and investor). Notice how the rankings vary even across the ethics sphere. No surprise that no one has a monopoly on virtue. In the last few years, though, you have the ESG movement push for composite scores for companies, and that has created an eco system that I am cynical about, in terms of what will be ultimately accomplished. If you are interested in my perspective on ESG, please try these two posts that I have on the topic:

In addition, I did mention that the one thing that impact investing does not seem to measure itself on is actual impact, and here is the link:

Finally, to cement my standing as an amoral, unethical “cares only about money” standing, I wrote about the sacred cow that sustainability has become, and why it too may be heading for the slaughterhouse:

While it may seem like we are paying far too much attention to these minor issues, I think that understanding who has the power to make decisions in a company will have significant consequences for how the company approaches every aspect of corporate finance - which projects it takes, how it funds them and how much it pays in dividends. So, give it your best shot.. On a different note, we will be start on our discussion of risk on Monday. As part of that discussion, we will confront the question of who the marginal investor in your company is. If you have already printed off the list of the top stockholders in your company (HDS page in Bloomberg or the Major Holders page from Yahoo! Finance), bring it with you again. If you have not, please do so before the next class. Also, watch for the in-practice webcast day after tomorrow, because I will go through how to break down the HDS page. I am also attaching the post-class test & solution for this session.

|

||||||||||||||||||

| 2/6/25 | As for the project & class, time sure does fly, when you are having fun... We are exactly 15.38% (4 sessions out of 26) through the class (in terms of class time) and we will kick into high gear in the next two weeks. I am going to assume for the moment that my nagging has worked and that you have picked a company to analyze. Here is what you can be doing (or better still, have done already):

I will be putting up a webcast tomorrow on how to analyze the "top shareholder" list, using a range of companies. Hope you to get a chance to watch it. I also hope that you have had a chance to register for Capital IQ and if you have not, I am reattaching the directions on how to do so. |

||||||||||||||||||

| 2/7/25 | Ahead of Super Bowl weekend , I thought I would get in the in-practice webcast for this week and nag you about your project (yet again). Since these webcasts are directly connected to what you will or should be doing on the project, the best way to use them is to pick a company and use the webcasts to get the relevant parts of the project done. This webcast looks at ways to assess the corporate governance at your company, using HP from 2013 as an example. I use HP's annual report, its filings with the SEC and other public information to make my assessment of the company.

HP Annual Report: http://www.stern.nyu.edu/~adamodar/pdfiles/cfovhds/webcasts/corpgovHP/HPAnnual.pdf

You can find these links in my webcast page, and it looks at what information to use and how to use it to assess the corporate governance structure of a company. (Sorry about the striped sweater… Should have known better)….. |

||||||||||||||||||

| 2/8/25 | 1. Newsletter: First things, first. Your newsletter is attached for the week. As is usually the case, there is not much news there, especially if you have been coming to class.

2. Company choice & groups: I was checking the corporate finance master sheet:

https://docs.google.com/spreadsheets/d/1xsASDBhkGo_1WhivAMLMkhi_z6cyYFnv1Q9G4y2TN4I/edit?usp=sharing

I am glad that it is filling up, and thank you to those of you who have entered the company name. I will be emailing those of you who have no company choice yet, right after this email. So, please don’t panic when you get that email. I am just trying to push you towards a decision.

3. Corporate Finance Puzzles: I have been posting the puzzles that I send out each week on Brightspace in the discussion section. I know that you have lots of things to do, but if you want to discuss and debate, that forum works well. The first discussion was about stakeholders in companies and the second one about corporate governance at family group companies…

4. Blog post on hurdle rates: I just posted my sixth data update for 2025, looking at hurdle rates in businesses.

While I know that you have other things on your plate this weekend, this may be an excellent post for you to read while you watch the Super Bowl halftime show, since it is directly relevant to what we will be b doing next week in lass.

One final note. If you are having trouble opening links on my emails or my webpage, try switching browsers. Google Chrome has issues with links to stern server sites.. (Don’t ask… It will unleash a stream of frustration…)

Attachment: Issue 2 (February 8) |

||||||||||||||||||

| 2/9/25 | I hope that you will be watching the Super Bowl this evening, not prepping for corporate finance. That said, my point about everything being corporate finance applies starting with the insane amount of money that it will cost a network to carry the Super Bowl today (and whether you can make it back on ad revenues or whether you need the show to boost other shows revenues), whether the halftime show will boost the earnings of the entertainer in question and what these ads tell you about the businesses doing the advertising.. Inquiring minds want to know. So, as you much your chips and watch Mahomes throw the ball from angles that look physically impossible, start tallying up the numberers.

Tomorrow, we will complete our discussion of corporate governance and start with a discussion of risk and how it plays out in hurdle rates. In the process, we will talk about the model that started the ball rolling, the capital asset pricing model (CAPM, how it is mystified by some and vilified for others, often in advancement of their agendas, and about alternatives to i5. We will move through this discussion in hyper speed for two reasons. One is that I have zero interest in reinventing modern portfolio theory and showing the mechanics of correlation and covariance. The second is that while I use the CAPM as a tool to estimate hurdle rates, I am not wedded to it and accept all kinds of alternatives (some of which we will talk about in class). If you are still shaky about even the assumptions that underlie the model, my suggestion is that you read chapter 3 from the applied corporate finance book before the class. If you don’t have the book, or not in the mood to read an entire chapter, please read my data posts from this year

These posts will prepare you for what’s coming in the sessions after, we will start on the fun stuff of applying the model, starting with what should be a slam dunk (risk free rates) which is increasingly not and then turning to the equity risk premium, a number that analysts often turn towards services to look up but really has deep implications for both valuation and corporate finance. So, much to do and I hope that you come along for the ride. |

||||||||||||||||||

| 2/10/25 | We started the class by wrapping up the question of at the end game in business, and why I (and you don’t have have to) still trust markets, over managers and expert panels. Markets have no ego, and if allowed to play out, will devise corrections to almost every over reach in business, whether it be managers taking advantage of shareholders, borrowers ripping off lenders, companies lying to markets or creating large social costs. My view is that companies should run to maximize value, but that will involve accepts self-constraints on behavior, and even if the market does not recognize it right away, but that managers need to consider the messages in stock prices.

We then moved on to risk and some of you may be regretting the shift from the soft stuff , but trust me that it is still fun.. If it is not, keep telling yourself that it will become fun. Anyway, here are a few thoughts about today's class.

If you can, try to make your assessment of whether the marginal investors in your companies are likely to be diversified. Look at both the percent of stock held in your company and the top 17 investors to make this judgment. If your assessment leads you to conclude that the marginal investor is an institution or a diversified investor, you are home free in the sense that you can now feel comfortable using traditional risk and return models in finance. If, on the other hand, you decide that the marginal investor is not diversified, we will come back in a few sessions and talk about some adjustments you may want to make to your beta calculations.

|

||||||||||||||||||

| 2/11/25 | In yesterday’s class, we went through the intuitive derivation of the CAPM. I thought that this week’s puzzle should be built around the central themes of portfolio theory, which is that diversification is the best weapon against risk, since it eliminates firm specific risk. That view, though, gets push back from some big name investors, including some value investing legends and Mark Cuban (who is also a legend, at least in his own mind). You can start the puzzle by reading the arguments for and against diversification:

The evidence, from looking at investor behavior, is that most individual investors side with the latter than the former (though that does not mean that it is right):

I am going to surprise you with my view. While I am more inclined to diversify than not, I can also see scenarios where not diversifying makes sense. In fact, I have a blog post on the question of how much diversification is good for you (and the answer will vary across individuals):

This is a topic that is important not just for your finance class, but for your personal portfolios, as you accumulate wealth (I am assuming that this Stern MBA, which you are paying a hefty price for, will pay off). |

||||||||||||||||||

| 2/12/25 | We started today’s class by tying up the last loose ends with risk and return models, talking about how assuming that there are no transactions costs and private information can lead us all to hold the market portfolio, and how risk can be then measured as risk added to that portfolio. We did damn the CAPM with faint praise, arguing that it does not do very well at explaining differences in returns across companies, but that it does at least as well as the alternatives. We then started on the mechanics of the model, taking about risk free rates: how to estimate the risk free rate in a currency where there is no default free entity issuing bonds in that currency and why risk free rates vary across currencies. The key lesson is that much as we would like to believe that riskfree rates are set by banks, they come from fundamentals - growth and inflation. I have a post on risk free rates that you might find of use:

In fact, risk free rates turned negative in a few currencies, upending what we know about risk free rates in. Here is my post on negative risk free rates.

In the second half of the session, we turned to equity risk premiums and how they are related to risk aversion. More on that in the next class. By the way, we have no class next Monday and I hope to see you, rested and ready to go next Wednesday!

There is one final point related to overall class logistics that I want to highlight. As you have noticed, I do come at you incessantly with emails, things to watch (like the in-Practice videos) and things to do, and I do realize that given all of the stuff you have on your plate, it is easy to get behind and feel overwhelmed. I understand that feeling, and I recognize that you may have far less time than I think you do for this class. In the interests of working with constraints, here is my suggestion on what you should focus on, given the time that you can spend on this class (in addition to being in lecture or watching it online).

Busy, Multiple constraints on time including health, family etc.

Time available: <3 hours a week

1. Do post-class tests (10-15 minutes for each class)

2. Review lecture notes for the session (20-30 minutes for each class)

3. Bare minimum on project company (30 minutes/week)

4. In quiz week, work through at least three or four past quizzes (2018-2022) (3 hours every three or four weeks)

Busy, Significant constraints on time

Time available: 3-6 hours a week

1. Do post-class tests (10-15 minutes for each class)

2. Review lecture notes for the session (20-30 minutes for each class)

3. Watch in-practice video each week (30 minutes/week)

4. Get numbers crunched on project company (1 hour/week)

5. In quiz week, work through at least six to eight past quizzes (2015-2022) (5 hours every three or four weeks)

Busy, but class is key priority

Time available: 6-10 hours a week

1. Do post-class tests (10-15 minutes for each class)

2. Review lecture notes for the session (20-30 minutes for each class)

3. Watch in-practice video each week (30 minutes/week)

4. Get numbers crunched on project company & start narrative (1.5 hour/week)

5. Read and give weekly challenge a quick try (30 minutes/week)

6. Review practice problems for each section and try two or three in each section (30 minutes/week)

7. In quiz week, work through at least eight to ten past quizzes (2013-2022) (6 hours every three or four weeks)

Obsessed with this class

Time available: As many hours as needed

1. Do post-class tests (10-15 minutes for each class)

2. Review lecture notes for the session (20-30 minutes for each class)

3. Watch in-practice video each week (30 minutes/week)

4. Get numbers crunched on project company & start narrative + help other group members (2.5 hour/week)

5. Read and give weekly challenge a try and explore topic further (1 hour/week)

6. Review practice problems for each section and try four or five in each section (1 hour/week)

7. In quiz week, work through all past quizzes (1997-2022) (8 hours every three or four weeks)

8. Read stories in financial press, and craft your corporate finance response to each story (continuous)

With each of these, note that I have not set aside the time that it takes to read these long emails, and I am sorry for that. But I cannot think of a better tether to keep you connected to the class. (I could text you the emails, but I don’t think your phone can handle that barrage.)

Until next time!

|

||||||||||||||||||

| 2/13/25 | If my nagging is paying off, you should have picked a company by now and if you have, you can move on to look at the marginal investors in you company, with the objective of assessing whether they are diversified, since it will let you know whether you are on safe ground using the CAPM or any other risk and return model. This will require a degree of judgment, but remember that you are not trying to identify a particular investor (Blackrock, Vanguard etc.) but a type of investor (institutional, insider, individual etc.). In making this assessment, having access to a Bloomberg terminal can speed the process, and if you get a chance, look at the YouTube video that I sent to you about using Bloomberg. If you don’t have access to a terminal, never fear, since much of the data is public. You can get both the breakdown of investors into insider and institutional, as well as the top holders of your stock. Here for instance is the page for PlugPower, a US company listed on the NASDAQ (under Holders): https://finance.yahoo.com/quote/PLUG/holders?p=PLUG

The assessment of who the marginal investor in PlugPower is easy to make. It is a large institutional investor, and very diversified. You can see that 55% of PlugPower’s shares (and 61% of the float, i.e., shares that are being traded at not locked away) are held by institutions, and if you are wondering whether that is high or low, I have data on insider and institutional holdings, by sector, for US, Global, European, Emerging (with China and India as separate date sets), Japan and Australia/NZ/Canada. You can find them here:

Scroll down to insider/institutional holdings and download the excel spreadsheets. If you have fallen behind in this class, there is nothing to fear. You have a whole week to catch up, and if it looks overwhelming, you should start with the entry page for the class:

Everything that we have done so far (from the class sessions, to weekly puzzles to even past emails) should be here.

One final note. These emails go out to a Google group email alias that is maintained by Stern IT. In theory, it should be synced with Albert, which is the registration system. In practice, the two systems sometime don’t talk well to each other. So, if you joined the class late and you are not getting emails yet, it may be because it has synced your name into the list yet. If you dropped the class, and you are wondering why I keep harassing you, it is again the syncing problem, and it is one that I cannot fix. You can try to talking to IT, but you know how that usually goes… So, good luck! |

||||||||||||||||||

| 2/14/25 | Ahead of a long weekend, I decided that it would be a good time to send not one, but two, valuation webcasts this week. The first lt is on assessing who the top stockholders in your company are and thinking through the potential conflicts of interest you will face as a result. The webcast went a little longer than I wanted it to (it is about 24 minutes) but if you do have the list of the top stockholders in your company (the HDS page from Bloomberg, Capital IQ, Morningstar or some other source), I think you will find it useful.

Webcast link: http://youtu.be/x_H_4KTeOkc

Presentation link: http://www.stern.nyu.edu/~adamodar/pdfiles/cfovhds/webcasts/holders.ppt

I hope that you get a chance to not only watch these webcasts but also try them out on your company.

The second one is on the first of the three inputs into your cost of equity, the risk free rate. If you want to get ahead of the curve, you can watch the webcast for this week, which looks at how to estimate risk free rates in different currencies, and how sovereign default spreads can be useful in getting there:

Webcast: https://www.youtube.com/watch?v=imfy-O9QuVc&index=3&t=0s&list=PLUkh9m2BorqmRAGzJb5OIvTAKZZu9HWF-

Additional material:

These datasets are from 2013. The 2025 versions are attached. Have a great long weekend1 Attachments:

|

||||||||||||||||||

| 2/15/25 | Last week, we put the objective function to rest and turned our attention to risk models. Next week, is a shortened week, since we will not have class on Monday. We will continue with our discussion of how best to estimate risk premiums and convert them into hurdle rates. I This week’s newsletter is attached. Attachments: Issue 3 (February 15) |

||||||||||||||||||

| 2/15/25 | As you can see from the heading, this is an email to all my classes, and it is about how to collect data, without getting overwhelmed by it. In particular, I want to focus on, and provide some help on data from three sources: the company itself (annual reports, financial filings), Capital IQ (a database of all publicly traded companies, with immense amounts of accounting and market data on each) and the physical Bloomberg terminals that are in the business school:

1. The Company: About 75% of the information, perhaps more, still come from annual reports and financial filings made by the company and the best source for this information is in the original documents (rather than on online sources, no matter how sophisticated). I usually start by finding the company’s webpage, going to the investor section and finding the most recent annual and quarterly report, as well as the analogous financial filings (10K and 10Q for US companies). Download them in pdf format, because you can then use the search box to search for the data you need in the pdf. (Warning: Do not read the annual report, until you are ready in terms of what data you want from the report)

2. Capital IQ: I have sent you many reminders that you have access to S&P Capital IQ. It is one of the premier global corporate datasets, and given how expensive it is to access, we are lucky to have access at Stern.

If you have not already done so, access Cap IQ, find your company, and it is pretty self-explanatory. I just download into excel the income statement, the balance sheets, the cash flow statement and the segment data, and I replace the default time period (which is the last few years with the maximum period, which can 30 years or more for some companies). You now have all of the historical data that you will need for your company. While you are in Capital IQ, you can also check out the industry grouping that your company is in, screen for other companies like it (by industry group, geography, market cap etc.) and download the data you might need on those companies (I would start with betas, market capitalizations, total debt and cash, but you may need to come back to this list again later in the class). I put together a YouTube video on how to do this, if you are interested:

3. Bloomberg terminal: Find the Bloomberg terminals in the building; for MBAs, there are four on the fourth floor of KMEC, and for undergraduates, there are four in Tisch 316 (accessed through 305). Since these are scarce, and hogging the machines is not a good idea, I thought I would create a guide specifying not only what you need to print off for your company, as well as where to find data on those print outs. I used BP as my company, and the print out should reflect what the pages should look like now for your company:

You will note that there are only six Bloomberg groupings you should print out, ten pages, in all.

HDS: Just the first page

BETA: One page

DES: Five pages

DDIS: One page

CRPR: One page

FA: One page

If you play this right, it should take you 10-15 minutes for your company, and you should do it as soon as you can. I know that this is my second email to you today, but to compensate, I will skip emailing you tomorrow and day after. See.. I am a compassionate person. Attachments: Capital IQ Access, Bloomberg Guide |

||||||||||||||||||

| 2/18/25 | Hi,

As we are navigate our way through a volatile economy and market, it is a good time to think about our views on risk and how it plays out in how we react to the crisis. Both economics and finance are built on risk aversion, i.e., that investors need to be paid extra (over and above an expected value) to take risks. That notion of risk aversion has been challenged and modified over time, but it still is at the heart of how we measure risk and come up with expected returns. Economists agree that not only does risk aversion vary across individuals but it also varies, for the same individual, across time. In this puzzle, which has no right answer, I would like you to wrestle with the question of how risk averse you, explanations that you can offer for that risk aversion and the consequences for your business and investment decision making. You can find the full details of the puzzle here:

One of the side products of the growth of robo advisors is a proliferation of tools that investors can use to assess how risk averse they are. This article in the New York Times nicely sets the table. In the article, though the links to free risk assessment services are no longer free. There are, however, plenty of risk aversion tests online. Here’re a couple that you can try at no cost (though the second one is longer):

University of Missouri: https://pfp.missouri.edu/research/investment-risk-tolerance-assessment/

Take the tests, both to get a measure of how risk aversion gets measured and how risk averse you are as an individual. Then, try to answer the following questions:

In tomorrow’s class, we will complete our discussion of equity risk premiums and perhaps start on the assessment of betas. It would help if you have the beta page for your company (from Bloomberg) and can bring it with you...

|

||||||||||||||||||

| 2/19/25 | Today's class was spent talking mostly about equity risk premiums. The key theme to take away is that equity risk premiums don't come from models or history but from our guts. When we (as investors) feel scared or hopeful about everything that is going on around us, the equity risk premium is the receptacle for those fears and hopes. Thus, a good measure of equity risk premium should be dynamic and forward looking. We looked at three different ways of estimating the equity risk premium. It is with this objective in mind that we computed an implied equity risk premium for the S&P 500, using the level of the index. If you want to try your hand at it, here is my February 2025 update:

Play with the spreadsheet. In fact, try it with today’s index level and T.Bond rate and see what the ERP is right now. I also noted the path of historical implied equity risk premiums, and how they have become more unstable and higher since 2008, mentioning a greater fear of catastrophic risks than ever before. If you are interested in this topic, I wrote a piece about it last week:

I then extended this approach into other markets, and talked about how to (and tried to) estimate equity risk premiums for other markets, using the country ratings (default spreads) as a building block. You can get my 2024 start-of-the-year equity risk premiums at this link:

As a final step, see if you can find the geographic revenue distribution for your company. You can then use my latest ERP update to get the ERP for your company. If you can find production exposure, even better. You will then have to decide whether you want ERPs based upon production, revenues or a composite of the two.

Beta reminder: Pease do try to find a Bloomberg terminal (find the one on the fourth floor of KMEC). Click on Equities, find your stock (pinpoint the local listing; there can be dozens of listings....) and once you are on your stock's page of choices, type in BETA. A beta page should magically appear, with a two-year regression beta for your company. Print if off. If no one is waiting for the terminal, try these variations:

1. Time period: Change the default to make it about 5 years and the interval from weekly (W) to monthly (M). Print that page off

2. Index: The default index that Bloomberg uses is the local index (a topic for discussion next session). You can change the index. Replace your default index (usually the index of rte country in which your company is incorporated and traded with the MSCI Global Equity Ihdex in the index box and rerun the regression.

Bring the beta page (s) with you to the next class. Let's get the project done in real time, in class.

|

||||||||||||||||||

| 2/20/25 | As part of the weekly project nag, I am going to start by assuming that you have picked a company to analyze and that if you have not entered its name in the Google shared spreadsheet, it is an oversight that you will fix soon.

https://docs.google.com/spreadsheets/d/1xsASDBhkGo_1WhivAMLMkhi_z6cyYFnv1Q9G4y2TN4I/edit?usp=sharing

If you have not filled a company name, expect an email from me shortly, but it is more a nudge than a push. So, don’t freak out!

Here are some things to consider doing to catch up:

On a different note, the first quiz is a week from Monday (on March 3), and if you feel the urge, you can start preparing for it, though you may find the third question on each quiz a bit of a mystery at the moment. Here are some resources:

1. If you do want to practice, you can find the past quiz 1s that I have given for this class, with solutions, at the links below:

2. There is a review webcast that I did for the quiz. If you are interested, you can get it by going to: My advice on the quizzes is that you start with the most recent quizzes and work backwards, and with time constraints in mind, here is what I would recommendL On the earlier quizzes, you will notice that I don’t provide an ERP in problems, and that 5.5% shows up in the answer. That is because I expected people to look up the ERP in their lecture notes, and it was roughly 5.5% then, but I have learned my lesson the hard way and provide the ERP in the problem in recent years. |

||||||||||||||||||

| 2/21/25 | It is Friday and time for the in-Practice Webcasts. I have two for this week.

The first is on estimating implied equity risk premiums:

The second webcast is on company equity risk premiums, using operating exposure:

Updated ERP spreadsheet: http://www.stern.nyu.edu/~adamodar/pc/datasets/ctryprem.xlsx |

||||||||||||||||||

| 2/22/25 | No big news this week, since we had only one session, but a newsletter with just a little news nevertheless. Attachments: Issue 4 (February 22) |

||||||||||||||||||

| 2/23/25 | I hope that your weekend is going well. The coming week is going to be a big one on multiple fronts.

|

||||||||||||||||||

| 2/24/25 | In today’s class, we looked past regression betas at how the choices companies make about the businesses they enter can determine their betas.. Summarizing the class, here is what we listed as the three determinants of betas:

If you remember, we looked at the beta for Disney after its acquisition of Cap Cities in the class. The first step was assessing the beta for Disney after the merger. That value is obtained by taking a weighted average of the unlevered betas of the two firms using firm values (not equity) as the weights. The resulting number was 1.026. The second step is looking at how the acquisition is funded. We looked at an all equity and a $10 billion debt issue in class and I left you with the question of what would happen if the acquisition were entirely funded with debt. (If you have not tried it yet, you should perhaps hold off on reading the rest of this email right now)

Debt after the merger = 615+3186 + 18500 = $22,301 million ( Disney has to borrow $18.5 billion to buy Cap Cities Equity and it assumes the debt that Cap Cities used to have before the acquisition) Equity after the merger = $31,100 (Disney's equity does not change) D/E Ratio = 22,301/31,100= 0.7171 Levered beta = 1.026 (1+ (1-.36) (0.7171)) = 1.497 Note that I used a marginal tax rate of 36% for both companies, which was the case in 1996. That’s about it for now, but your quiz is next Monday. More on that in a different email.

|

||||||||||||||||||

| 2/25/25 | This week’s puzzle is on betas and I have used GameStop as my lab experiment. First, check out the description of the puzzle (with the beta pages for both companies):

Once you have browsed through it, here are the questions that I would like you to consider

Just a reminder again that the first quiz is on March 3 (next Monday). The TAs, Justin and Guilherme, are both incredibly knowledgeable and helpful and I will add office hours this weekend for questions that you may have.

On a different note, if you have been checking the calendar, you will probably see a case due on March 19. If you are wondering what that case is, I thoughr I would resolve the mystery and send you the case today. You have three weeks to work on it, and some of the material for the case has not been covered in class yet, but it will help if you can quickly browse through the case.

It is a group case, and dividing some of the labor will help you. But I will let you figure out that process.

|

||||||||||||||||||

| 2/26/25 | In this session, we continued the discussion of betas being weighted averages, and used the concept to estimate the beta for Disney, starting with its businesses and working up to the beta of the company, and we repeated that process with the other companies in our mix - Vale, Tata Motors, Baidu and Deutsche Bank. We ended the class by talking about how to estimate the cost of equity, when an investor/buyer is not diversified, and noted that this can explain why private companies end up as parts of publicly traded companies.

If you feel the urge to estimate the betas of the businesses that your company operates in on your own, please do so, but I do have betas estimated by industry for various groups on data page. The US, emerging market and global averages are linked below, but you can find similar averages for Japanese, European, Indian and Chinese companies:

Emerging Markets: https://pages.stern.nyu.edu/~adamodar/pc/datasets/betaemerg.xls

I also have total betas by industry and for different regional sub-groupings, if you are interested.

|

||||||||||||||||||

| 2/27/25 | Today is usually the project update day. If you really have the time for it, this is a good week to get a bottom up beta for your company and estimates costs of equity for each business line it operates in. I You can get betas by business going to my website:

If you scroll down, you will set betas (levered and unlettered), by business and while the html file includes only US companies, you can download the averages for the rest of the world in the next column. If you prefer to compute your bottom up betas yourself, you can use other databases, but the one that is easiest and most comprehensive is the S&P Capital IQ database. Early this semester, I had sent you instructions on how to get access that database, and if you have not, try to do so now. (See attached instructions.. I know… I know.. I’ve sent it four times already, but just in case...). It provides you incredibly powerful screening tools with 50000+ publicly traded companies, and very simple ways of picking the data you need and downloading that data into a spreadsheet.

The quiz is on Monday, in the first 30 minutes of class, and please take advantage of the TAs for the class, Justin and Guilherme. I am in Portugal today through Saturday, but will be back by mid-afternoon Sunday, and will have office hours on Sunday from 5 pm - 7 pm.

Join URL: https://nyu.zoom.us/j/99520086506

If you are looking for past quizzes and the quiz review, the links are below:

A mea culpa on the quiz solutions. I must have been out of it when I put together the spring 2022 solutions, because there were at least two problems where the answers were off (the second problem where I estimated a cost of equity in Colombian pesos when the problem specified Sul) and the third problem where my solutions suggested a $400 million borrowing, when it was actually $800 million. In my defense, there were two versions of the quiz, and the solution I sent you was for the wrong version. They have been fixed now, and you can download the correct version.

|

||||||||||||||||||

| 2/28/25 | If you want to take time away from preparing for the quiz, in this week’s webcast, I take a look at Disney's 2-year weekly regression (from February 2011- February 2013). I have the Bloomberg page attached. I am also attaching the spreadsheet that I used to analyze this regression, which you are welcome to use on your company. The webcast is available at the link below:

Disney’s Regression Bloomberg beta page: https://www.stern.nyu.edu/~adamodar/pdfiles/cfovhds/webcasts/Regression/Disneyregression.pdf

The best way to make this stick is to try this on your company quickly.

I also have a webcast on the mechanics of estimating bottom up betas. I use United Technologies to illustrate the process and I go through how to pull up companies from Capital IQ. Even if you don't get a chance to watch it after the quiz, it may perhaps be useful later on. Here are the links:

United Technologies 10K: https://www.stern.nyu.edu/~adamodar/pdfiles/cfovhds/webcasts/Bottomupbeta/UT10K.pdf

Spreadsheet to help compute bottom up beta: https://www.stern.nyu.edu/~adamodar/pdfiles/cfovhds/webcasts/Bottomupbeta/bottomupbeta.xls

The last spreadsheet has built into it the industry averages that I have computed for different sectors in the US in 2015. You can get the updated version from 2023 here:

The quiz is on Monday, in the first 30 minutes of class, and please take advantage of the TAs for the class, Justin and Guilherme. At the risk of repeating myself, I will have office hours on Sunday from 5 pm - 7 pm.

Join URL: https://nyu.zoom.us/j/99520086506

|

||||||||||||||||||

| 3/1/25 | First, it is the weekend and the newsletter is attached. Second, and perhaps more important, your quiz is on Monday. I will not repeat all the links again, but I will have office hours tomorrow from 5 pm - 7 0m and the zoom link is below:

Attachments: Issue 5 (March 1) |

||||||||||||||||||

| 3/2/25 | The quiz is definitely tomorrow in the first 30 minutes of class and just to repeat what has been said before, it is

- open book and open notes

- you can use your tablets and laptops for reviewing your slides and other material

- you can use abacuses, slide rules and calculators (physical or digital), but no excel.

. As I get emails about the quiz, I thought it would be a good idea to pull together a list of the top emailed questions that I have received so far.

1. Why do we use past T.Bill rates for Jensen's alpha and the current treasury bond rate for the expected return/cost of equity calculation?

The Jensen's alpha is the excess return you made on a weekly/monthly basis over a past time period (2 years or 5 years, depending on the regression). Since you are looking backwards and computing short-term (monthly or weekly) returns, you need to use a past, short-term rate; hence, the use of past T.Bill rates. The cost of equity is your expected return on an annual basis for the long term future. Hence, we use today's treasury bond or long term government bond rate as the riskfree rate. 2. How do you decide whether to use a historical or an implied equity risk premium? In a market like the US, with a long and uninterrupted history, the choice depends on whether you believe that things will revert back to the way they were (in which case you may decide to go with the historical premium) or that the world is a dynamic, ever-shifting place, in which case you should go with the implied premium. In most other markets, where you don't have a long history, it is not really a choice, since the historical premium is too noisy (big standard error) to even be in contention. Thus, I use a short cut. If it is a AAA rated country like Germany or Australia or Singapore, I use the US equity risk premium, arguing that mature markets need to share a common premium. If it is not a AAA rated country, see the answer to (4). 3. How do you estimate a riskfree rate for a currency in an emerging market? If you are doing your analysis in US dollars or Euros, you would use the riskfree rates in those currencies: the US treasury bond rate for US dollars and the German Euro bond for the Euro. In the local currency, you should start with the government bond rate in the local currency and take out of that number any default spread that the market may be charging (see the Mexico example in the review packet). The default spread can be obtained in one of three ways: (a) The difference between the rate on a dollar (Euro) denominated bond issued by the country and the US treasury bond rate (German Euro bond rate), (b) CDS spread for the country or (c) typical default spread given the local currency rating for the country. As to which one you should use in a problem, the problem will almost always push you in one of the three directions. Don’t fight it. 4. How do you adjust for the additional country risk in companies that have operations in emerging markets? If the country you are analyzing is not AAA, you should adjust for the risk by adding an "extra" premium to your cost of equity. The simplest way to do this is to add the default spread for the country bond to the US risk premium. This will increase your equity risk premium and when multiplied by your beta will increase the cost of equity. A slightly more sophisticated approach is to adjust the default spread for the relative risk of equities versus bonds (look at the Mexico example in the review) and adding this amount to the US premium. This will give you a higher cost of equity. If you are given enough information to do the latter, do it (rather than use just the default spread). When assessing the equity risk premium for a company, look past where the company is incorporated at where it does business. The equity risk premium that you use should be a weighted average of the equity risk premiums of the countries in which the company operates. 5. Why do you use revenues (rather than EBIT or EBITDA) as the basis for your weighting for ERP? Note that what you would really like to know is the value of a company's different businesses/geographies, but since you don't have value, you look for proxies. While you may have a choice of different measures (revenues, EBITDA, EBIT etc), I prefer revenues for three reasons. First, it is always a positive number, which is good since I want weights that are greater than zero. Second, it is less susceptible to accounting allocation judgments than numbers lower down on the accounting statement. Third, I can convert it into a value by using an EV/Sales multiple, which I can get from the sector. 6. Why do you use the average debt to equity ratio in the past to unlever a regression beta? The regression beta is based upon returns over the regression time period. Hence, the debt to equity ratio that is built into the regression beta is the average debt to equity ratio over the period. 7. What is the link between Debt to capital and debt to equity ratios? If you have one, you can always get the other. For instance, the Fall 2006 quiz gives you the average debt to capital ratio over the last 5 years of 20%. The easiest way to convert this into a debt to equity is to set capital to 100. That would give you debt of 20 and equity of 80, based upon the debt to capital ratio of 20%. Divide 20 by 80 and you will get the debt to equity ratio of 25%. 8. How do you annualize non-annual numbers? The most accurate thing to do is to compound. Thus, if 1% is your monthly rate, the annual rate is (1.01)^12-1.... if 15% is your annual rate, the monthly rate is (1.15)^(1/12) -1... When the number is low, as is usually the case with riskfree rates, you can use the approximation of dividing by 12 (to get monthly) or 52 (to get weekly). But try to always compound the Jensen's alpha numbers, since they can be much bigger. 9. What is the cash effect on beta? Why does it sometimes get taken out and sometimes get put back in? I know that dealing with cash is on of the more confusing aspects of beta and cost of equity. Let's start with some basics. If a company has cash on its balance sheet, that cash is an asset with a zero beta (or at least a very low one) and it will affect the beta for the company and the beta that you observe for its equity (say, from a regression). What you do with cash will therefore depend upon what beta you are starting with and what beta you want to end up with. For the pure play or unlevered beta by business: You start with the average (or median) regression beta across the comparable companies in the business. To get to a pure play beta for the business, here are the steps: Step 1: Unlever the regression beta, using the gross debt to equity ratio for the sector Unlevered beta for median company in sector = Regression beta/ (1+ (1- tax rate) (Debt/Equity Ratio for the sector)) Step 2: Clean up for the cash held by the typical company in the sector, using the median cash/ firm value for the sector (see below for firm value) Unlevered beta for the business = Unlevered beta for median company/ (1 - Cash/Firm value for the sector) Note that you use sector averages all the way through this process, for regression betas, debt to equity ratios and cash/firm value Alternatively, you can use the net debt to equity ratio and cut it down to one step Net Debt to Equity = (Debt - Cash)/ Market value of equity Unlevered beta for the business = Levered Beta for median company /(1+ (1-tax rate) (Net Debt to Equity)) To get to the bottom up equity beta for a company: You start with the unlevered betas with the businesses and work up to the equity beta in the following steps: Step 1: Compute a weighted average of the operating business betas, using the values of the operating businesses in the company: Unlevered beta for operating assets of the company = Pure play betas weighted by values of the operating businesses Step 2: Compute a weighted average of all of the assets of the company, with the company's cash included (since cash has a beta of zero) Unlevered beta for entire company = Unlevered beta for operating assets (Value of operating assets/(Cash + Value of operating assets)) Step 3: Compute a levered beta for just the operating assets of the company, using the debt to equity ratio of the company Levered beta for operating assets of the company = Unlevered beta for operating assets (1+ (1- tax rate) Company's D/E ratio) Step 4: Compute a levered beta for all of the assets of the company, with cash included Levered beta for all assets of the company = Unlevered beta for entire company (1+ (1- tax rate) Company's D/E ratio) It is the beta in step 4 that is directly comparable to your regression beta. Note that all the numbers in this part are the company's numbers - for values for the businesses, cash holdings and debt/equity. 10. Why do you weight unlevered betas by enterprise value (as you did in the Disney/Cap Cities acquisition) and in computing Disney's bottom up beta? The unlevered beta is a beta fo the asset side of the balance sheet, right? So, when weighting these unlevered betas, you want to weight them by how much the businesses are worth (and not how much the equity is worth). That is why I used enterprise value weights in the Disney bottom up beta computation. I cheated on the Cap Cities acquisition by ignoring cash for both Disney and Cap Cities, but if cash had been provided, I would have used enterprise value. In case you are a little confused about the different values, here they are:

Sorry about the long email… and hope to see you at the zoom session (and I will record it).

|

||||||||||||||||||

| 3/3/25 | I know that sitting in a class after a quiz is tough to do, and I thank you if you did so. In the quiz -shortened session, we first defined debt broadly as including all contractual obligations, thus encompassing all interest bearing debt and leases. We then argued that the cost of deb tis a long term rate of borrowing money today, and is thus composed of a riskfree rate and a default spread. With rated companies, we can use the rating to get a spread, but for non-rated companies, you have to use the interest coverage ratio to get a synthetic rating, and then use that rating to get a default spread. With companies in risky countries, you should be adding the country default spreads to the riskfree rates to get to the cost of debt. Finally, we have to bring in the tax savings that accrue from being able to net interest expenses out to get to taxable income, by multiplying the cost of debt by (1- marginal tax rate). So, until you get my email about your quizzes, that’s about it. |

||||||||||||||||||

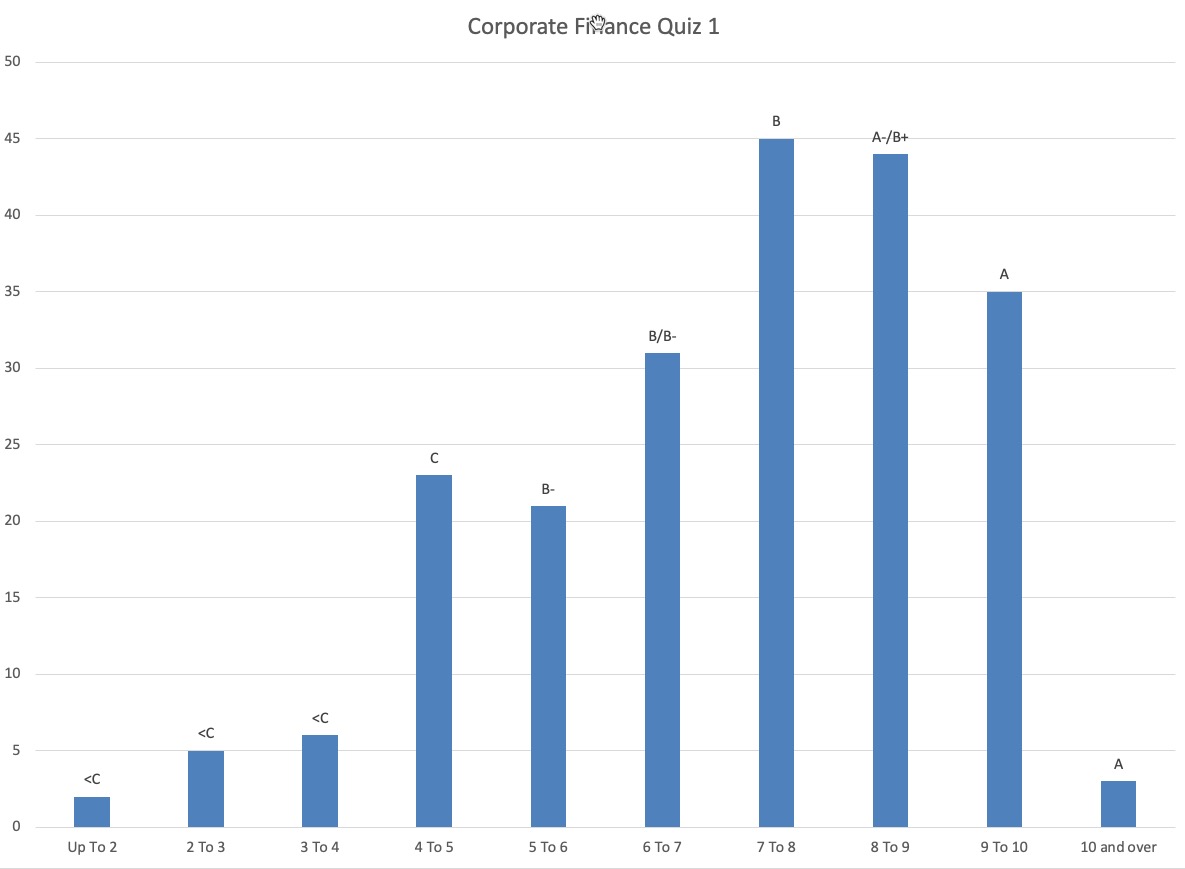

| 3/3/25 | Your quizzes are done and can be picked you. I am sorry for sending you the notification late in the evening, and I don’t expect you to do much about it right now.

Attachments: Quiz 1, solution and grade distribution |

||||||||||||||||||

| 3/4/25 | As you have learnt by now, I am a relentless nag, and I will continue on that mission. Before I get to the nagging, I want to deal with some of the quiz 1 answers where you and I might have disagreed and explain more fully my choices.

With all of that said, there is no point beating yourself up about things done and undone, and as I said, if you truly feel that you have been unfairly graded, bring it up with me (and not with the TAs, since they had nothing to do with it).

On a different note, if you look at your syllabus, you will notice a case worth ten percent, and if you are wondering what the case is about, and when you will be able to read it, it is your lucky day. Rather than give you a puzzle, I am posting the case with one of the exhibits as an excel spreadsheet:

It is a case built around an investment analysis and it is a group project about Celsius, the beverage company that took the market by storm in the last few years, before running into headwinds The project is a group project, and is due by March 19, 2025, before the start of class. It would make sense for the group that you have formed for your final project to be group for the case as well, but if you are a group of eight, and want to do the case as two groups of four, I am okay with that too. I know that you have two weeks, but I would suggest reading it right away and doing it in bite size pieces. I think you should get started on the case as soon as you can, with what you can do. For instance, one of the things you will need to estimate is a discount rate for the project, and much of what we have done in class in the last few sessions should help, and if you read it, the next couple o sessions should help you on the rest of the analysis.

|

||||||||||||||||||

| 3/5/25 | In this session, we first completed our discussion of hurdle rates, by looking at computing market values of debt (drawing on bond pricing), and then talking about when you use the cost of equity and when the cost of capital as a hurdle rate. Our discussion of investment returns began with the “Show me the money” theme from Jerry Maguire, and why we use cash flows, not earnings, in measuring investment returns, After making an argument for the primacy of cash flows, we looked at how a good measure of return is time weighted and incremental and how every investment is a project (small or large). We spent the bulk of the class describing the Rio Disney investment, and then computing the return on capital on that investment, based upon expected revenues and operating income. We will continue with that discussion next class. |

||||||||||||||||||

| 3/6/25 | Today is also usually the day that I write to you about your project, but if you are budgeting your time to immediate priorities, you should be working on the case. I know that you are heading off for spring break, but In case your fascination with corporate finance leads you to work on the case, here are a few suggestions on dealing with the issues.

I have to warn you in advance that there are parts of the case where I have deliberately not given specific assumptions, because I want you to make your own, and check for consistency. |

||||||||||||||||||

| 3/6/25 | File this away under “There is no rest for the wicked”, as I bring you back to the your project. Assuming that you have been working along with me, by now, you should have a risk free rate in the currency of your choice, an unlettered beta reflecting the business or businesses that your company is in and the equity risk premium that you have for your company. To get the unlevered beta to a levered beta, you need market values for equity and debt. With a publicly traded company, the former should be easy (market capitalization of all classes of shares) but the debt can be tricky. You should at least be able to get a book value of debt from the balance sheet (remember to count both short term and long term interest bearing debt), and if your company has leases and is following either GAAP or IFRS, the lease debt should also be there. If you don’t trust accountants, and want to do this right, you can covert book debt to market debt and capitalize leases for your company, but you will need a cost of debt for your company to be able to do this, and you can get that using either an actual rating or a synthetic rating for your company. I have a ratings spreadsheet that will do both (compute a synthetic rating for a company and capitalize leases. This is the link that I sent out yesterday:

Once you have all these numbers, you can compute a cost of capital. I know that you may be several steps behind, but if you do get to this number, please remember to go to the Google shared spreadsheet and enter your numbers for your company:

https://docs.google.com/spreadsheets/d/1xsASDBhkGo_1WhivAMLMkhi_z6cyYFnv1Q9G4y2TN4I/edit?usp=sharing

If you get to this point and want to compare your company’s cost of capital to others in the industry, at the start of 2024, you can find industry averages on my website, under current data.

Scroll down to the cost of capital section. |

||||||||||||||||||